For U.K. Debt Chief, Only Certainty Is Unprecedented Bond Supply

For U.K. Debt Chief, Only Certainty Is Unprecedented Bond Supply

(Bloomberg) -- Britain is almost certainly heading for its biggest borrowing binge on record, and it’s still anyone’s guess how high bond issuance might go.

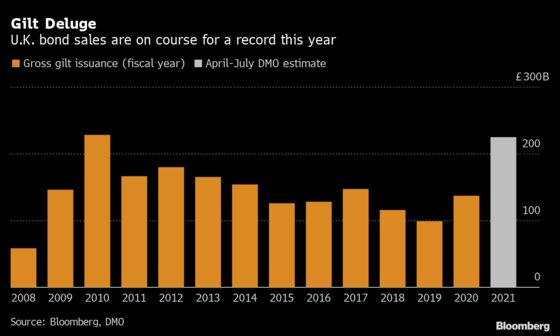

Robert Stheeman, chief executive of the U.K.’s Debt Management Office, is “very confident” he can sell an unprecedented flurry of government bonds in coming months. Gilt issuance is set to surge to 180 billion pounds ($222 billion) between May and July -- more than four times the level implied by an estimate just last month.

Yet in refusing to put a number on total sales for the next year on Thursday, the U.K. took an unusual step that surprised investors. A Bloomberg survey of primary dealers before the announcement estimated that Britain will sell 270 billion pounds of gilts over the course of the fiscal year, though estimates varied by almost 150 billion pounds.

“The whole situation is hugely uncertain -- it’s not our usual method of operating but these are unusual times,” Stheeman said in an interview Thursday. “What we’re trying to do is tell the market this is our best attempt at providing certainty about what we know, rather than speculate about something which might turn out to be wrong. We do not want to mislead anyone.”

U.K. Chancellor of the Exchequer Rishi Sunak faces a problem shared by finance chiefs the world over: funding an unprecedented relief package, which includes emergency payments to struggling businesses and furloughed workers, at the same time as the economy is shut down and tax receipts slashed.

That’s where the DMO comes in. Filling the financial gap means the U.K. must turn to international bond markets on a scale not seen even during the global financial crisis. It’s Stheeman’s job to get the British taxpayer the best value on the hundreds of billions it will borrow.

Taken together with the 45 billion pounds of gilt sales in April, the total borrowing in the first four months of the fiscal year almost matches the 228 billion pound annual record in 2009-10. Stheeman says he’d be “very surprised” if bond issuance this year did not eclipse that.

Gilts initially fell after the supply announcement, before weak economic data sent investors back into bonds across Europe. Yields fell two basis points Friday to 0.27%, just half of their level in February, following a global rally in haven debt.

Monetary-Fiscal Equilibrium

Any strain on gilt markets could make it more costly for Britain to fund its relief program. Such is the immediate pressure on financing that the Bank of England extended its so-called Ways and Means facility -- effectively a government overdraft at the central bank -- by an unspecified amount earlier this month.

Stheeman welcomed the move, saying it will ensure the smooth operations of the U.K.’s cash management operations and avoid the country resorting to money markets. “It is not there in any way as a financing tool,” he said. “It is a temporary facility, and it really must be emphasized that it has always been used as such.”

The DMO is confident both domestic and international funds will soak up the supply deluge, saying the U.K.’s sovereign marketplace has proved more liquid and better functioning than its peers. The BOE’s 200 billion pound bond-buying program also provides a backstop for investors.

“The market has seemed to have found something of an equilibrium between us, as a massive source of supply, and the Bank of England, as a very large source of demand in the secondary market,” he said. “The fact yields have moved very little on the back of the announcement confirms that for me. Right now the market does not feel dislocated.”

©2020 Bloomberg L.P.