Mortgage Investors Buoyed as Refinancings Signal Prepayment Peak

For Mortgage Investors, Prepayment Speeds Trump Repo Volatility

(Bloomberg) -- Despite the recent volatility in repo rates, the agency mortgage sector has been a relative bedrock of stability.

The threat of faster prepayment speeds, of prime importance to mortgage valuations, seems to be abating, helping performance. Also contributing to insulating the sector from repo volatility is the widespread use of the dollar roll market to fund to-be-announced transactions, and a preference among mortgage investors to finance their settled positions with term rather than overnight repo.

While this Friday’s prepayment speed report for September is expected to show a 10% increase over the previous month, the 30% drop in the refinance index over the past four weeks suggests prepayments may soon peak. In addition, the recent increase in primary mortgage rates has removed about $550 billion worth of home loans from being able to refinance.

“The big factor in mortgage-backed security prices and spreads is prepayments more than funding costs,” said Scott Buchta, head of fixed income strategy at Brean Capital. “The reason that repo has had a lesser impact on mortgages than on Treasuries is because they still tend to yield more than repo.”

Dollar roll: A type of repurchase transaction in the mortgage pass-through securities market in which the buyside counterparty of a “to-be-announced” (TBA) trade agrees to sell off the same TBA trade in the current month and to buy back the same trade in a future month

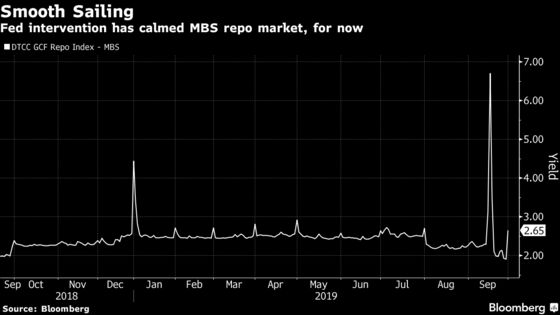

The mortgage sector continued to outperform Treasuries even as volatility in the repo market surged on Sept. 16, prompting the Federal Reserve to intervene. During the week ended Sept. 20, when mortgage repo rates closed at a multi-year high of 6.7%, sector outperformance actually hit a month-to-date peak of 30 basis points. Yesterday saw it close at 24 basis points for the month as a whole, the same level seen on Sept. 13.

There are still pockets of fast-paying cohorts within the mortgage universe. A recent report from Wells Fargo & Co. points out that UMBS 30-year pass-throughs delivered to settle TBA trades exhibited 1-month CPR of 40, 40 and 57.5 for the 3.5%, 4% and 4.5% coupons. Back in January they were 4, 7 and 10, respectively. Faster speeds hurt performance for mortgage investors who purchased their bonds at a premium, and all three of those TBA coupons are trading well above par.

A conditional prepayment rate (CPR) is a loan prepayment rate equivalent to the proportion of a loan pool’s principal that is assumed to be paid off ahead of time in each period

Because of this, the 3.5%, 4% and 4.5% TBA -- where the most recent vintages with characteristics such as prime credit scores and large loan sizes that are red flags for faster prepayment speeds lie -- have seen their rolls drop into negative territory from being essentially flat at the end of June, according to Bloomberg’s TBA Roll Analysis reports.

“The fact rolls are trading negative is because the implied CPR is so fast. The issue with repo is piling on to the roll issue,” said Walt Schmidt, head of mortgage strategies at FTN Financial in Chicago.

Of course, a renewal of repo volatility and higher rates would not be of benefit to mortgages, or securities markets in general, as investor balance sheets would become more expensive to fund. It will only be known if this issue has been put to bed when the Fed steps away and allows repo to find its own level. If rates spike again, the next question is will the central bank set up a more permanent intervention mechanism.

Read more: ‘Repocalypse’ to Raise MBS Funding Costs, Pressure mREITs: JPM

“The last thing the Fed wants is a liquidity crisis due in part to their decision on balance sheet size,” said Anthony Di Ciollo, co-head of fixed income at INTL FCStone Financial Inc. “The question is, will they deliver what the market wants.”

NOTE: Christopher Maloney is a market strategist and former portfolio manager who writes for Bloomberg. The observations he makes are his own and are not intended as investment advice

To contact the reporter on this story: Christopher Maloney in New York at cmaloney16@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, William Selway

©2019 Bloomberg L.P.