The U.S. Yield Curve Isn’t as Boring as It Seems

The U.S. Yield Curve Isn’t as Boring as It Seems

(Bloomberg Opinion) -- For market observers, it’s usually not interesting to read (or write) about something that’s little changed. In the case of the U.S. yield curve, however, it’s precisely the recent bout of unusual calm that should be a signal to investors about the future direction of monetary policy and the level of interest rates.

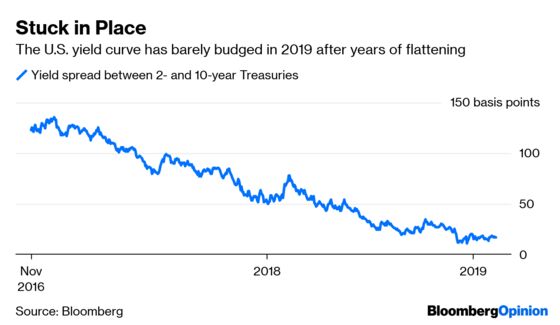

The $15.6 trillion Treasury market has been stuck in place in 2019, with growth slowing worldwide and the Federal Reserve pausing on further interest-rate increases for the time being. Nowhere is this rut more evident than the spread between two- and 10-year note yields: It has moved less than one basis point in 17 of the past 22 trading sessions (roughly one calendar month), a streak of tranquility that’s unrivaled in recent memory. One of the closest contenders is the month from mid-August to mid-September 2006.

That’s significant because June 2006 was the last interest-rate hike of the previous tightening cycle, while Aug. 8 of that year marked the first time in more than two years that policy makers kept their lending benchmark steady after a Federal Open Market Committee meeting. It’s easy to see the parallels to the current “pause.” Whether or not the Fed is done raising rates this go-around, the markets are acting as if that’s the case.

There’s one big difference between now and 2006, though. Back then, the yield curve from two to 10 years was inverted. That segment has remained stubbornly positive this time, even as other parts flipped below zero in December. It raises the pivotal question of whether the yield curve will fully invert before the next economic downturn or whether the Fed stopped just in time to prevent that classic recession indicator.

Investors and strategists are talking about the prospect of a recession in the coming year or two and separately debating the next move in the yield curve. But because of the Fed’s pivot, the two outlooks no longer seem to be quite as linked. Instead, there seems to be a growing consensus that Chairman Jerome Powell has pushed off a U.S. recession. For example, Scott Minerd at Guggenheim Partners last week pegged it at late 2020, compared with a previous forecast for late 2019. Kyle Bass, founder of Hayman Capital Management, said this week that the U.S. would most likely enter a mild recession by the middle of next year.

As far as the yield curve, though, Wall Street isn’t quite on the same page. Here are a few recommendations from bank strategists, courtesy of Bloomberg News’s Elizabeth Stanton:

- Barclays: Bet on a flatter curve from five to 30 years.

- UBS: Bet on a steeper curve from six months to two years.

- Morgan Stanley: Bet on a flatter curve from two to five years.

- Bank of America: Abandon curve-flattening bets, look for tactical opportunities to bet on steepening.

- Deutsche Bank: Bet on a flatter curve from 10 to 30 years.

- Societe Generale: Little scope for the curve from two to 10 years to flatten or invert.

Confused? It’s no wonder that the yield curve has barely budged in the past few weeks. For much of the past two years, the easy trade has been to not fight the Fed and the flattening. Some brave souls probably tried to bet on an extended steepening, only to see it falter time and again.

For now, fed funds futures are pricing in no change to the Fed’s benchmark rate this year. That makes it hard to pinpoint any sort of driver one way or the other for the yield curve. As long as U.S. data is good enough for the central bank to leave rates where they are, it’s hard to see the two-year yield falling much below 2.5 percent (the upper bound of the fed funds rate). Meanwhile, with economists and Fed officials seeing slower growth this year than previously expected, 10-year Treasury yields may have peaked already. As Krishna Memani, head of fixed income at OppenheimerFunds Inc., said to me in an interview: “People were talking about 3.5 percent or 4 percent, all that nonsense, and it’s proven to be just that.”

To Memani, “The front end of the curve is really the interesting part. The long end of the market in Treasuries is going to remain boring for the foreseeable future.”

While the day-to-day movements may be small, the implications are big. It was only about a year ago that Bill Gross declared, “Bond bear market confirmed.” It was even more recently that Franklin Templeton’s Michael Hasenstab saw 10-year yields reaching 4 percent, while JPMorgan Chase & Co.’s Jamie Dimon warned that 5 percent was more likely than people thought. If it’s back to lower-for-longer, does that mean a renewed push into the highest-yielding corporate debt? Rightly or wrongly, that seems to be the playbook so far.

Surely, something will come along to shake the yield curve out of its slumber. Maybe this week’s data will show January’s inflation was higher than forecast, sparking a sell-off in long bonds. Maybe there will be a breakthrough in trade talks between the U.S. and China, causing investors to shed Treasuries and buy riskier assets. Maybe the federal government will shut down yet again, which could drive some haven flows. Or perhaps like in 2006 and 2007, this environment will last for about a year. Indeed, the futures market starts to price in a rate cut in mid-2020.

Gone are the days of the yield curve relentlessly flattening toward inversion. For now, the most exciting thing is the unknown path of the world’s biggest bond market. It can only stay in place for so long.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.