Laggard-to-Braggart for Italy’s Bonds Enables Talk of 0% Yield

Fightback for Italy’s Bonds Enables Talk of 0% Benchmark Yield

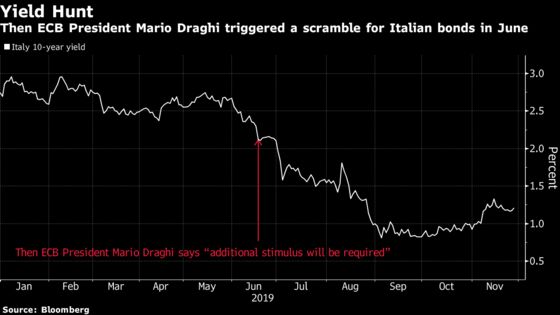

(Bloomberg) -- The fortunes of Italy’s debt have been transformed this year, with the benchmark 10-year yield on course for its biggest annual drop since 2014, even leading to talk among analysts that it could touch 0% in 2020.

Such speculation would have been highly unlikely 12 months ago, when the bonds lagged their European peers as a populist government threatened to blow the budget deficit wide open. Now, a re-formed coalition government is in place, having avoided snap elections in September and the European Central Bank’s resumption of stimulus has resurrected a major buyer for its debt.

According to Markus Schomer, the New York-based chief economist at PineBridge Investments, the prospect of “0% Italy” is not a reflection of how bad things are in the euro area, but could be seen as “the ECB’s next stimulus tool” as it seeks to lift growth and inflation with quantitative easing.

“The point of more QE is to level the interest-rate effect on member states’ budgets,” said Schomer. “Germany paying less interest on its debt may be a correct representation of the credit risk, but Italy needs more help to stave off recession and has less room to use fiscal policy. That’s why it would make sense to provide all euro-zone members with the same low German rates.”

While the talk of 0% yields is a long way from consensus, optimism is commonplace among strategists into 2020. The country’s benchmark yield, comfortably above 1%, stands out given the equivalent German and French debt is negative, locking in a loss for investors holding it to maturity.

Lyn Graham-Taylor, senior rates strategist at Rabobank, also points to the outlook for deeper negative yields at the core of the euro area when he says “there is more juice in Italy,” which looks “attractive to investors looking for positive yield.”

The sweet spot for Italian bonds is also defined by the more restrained fiscal policies of its re-drawn coalition. Prime Minister Giuseppe Conte’s ability to hold the government together will be crucial, but investors are remaining positive on his chances for now.

Conte expects his budget to pass by the end of the year, avoiding a domestic crisis and a fiscal stand-off with the European Union. But as ever with politics, there are signs of stress between the government’s partners, which have intensified their squabbling in past weeks. National polls point to a clear win for the rival populist League party, led by Matteo Salvini, should a general election prove necessary if the national government splits.

Until those risks materialize, the ECB’s economic stimulus which restarted in November, with its purchases of 20 billion euros ($22 billion) a month of debt, is likely to help underwrite demand for Italy’s bonds, also known as BTPs.

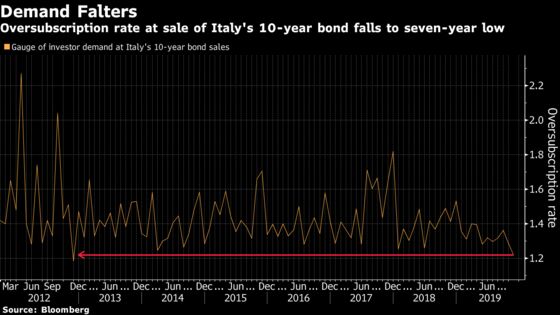

There are some signs sentiment is vulnerable to change. Demand for Italian 10-year bonds at an auction Thursday fell to the weakest in seven years. The historically low outright yields were a factor, along with profit-taking by investors heading into the end of the year, according to Antoine Bouvet, a senior rates strategist at ING Groep NV in London.

Investors tracking debt market benchmarks are still likely to be buying. Tony Small, the London-based head of European rates strategy at Morgan Stanley, points out that BTPs represent almost 25% of the Bloomberg Barclays Euro Area Aggregate Treasury Index collectively. He predicts that the 10-year yield premium over German debt will probably narrow about 50 basis points to 100 by the end of next year.

--With assistance from William Shaw, Joanna Ossinger and John Ainger.

To contact the reporter on this story: James Hirai in London at jhirai3@bloomberg.net

To contact the editors responsible for this story: Dana El Baltaji at delbaltaji@bloomberg.net, Michael Hunter, Neil Chatterjee

©2019 Bloomberg L.P.