The Fed’s 'First, Do No Harm' Policy Is Harmful

The Fed’s 'First, Do No Harm' Policy Is Harmful

(Bloomberg Opinion) -- The sharp “risk-on” rally in financial markets this year strongly suggests that the U.S. economy has been inoculated against recession risk by the Federal Reserve’s dovish pivot. This reasoning, however, ignores to two notable concerns. First, the cyclical slowdown in growth that precipitated the plunge in stocks in the fourth quarter isn't about to end. Second, everyone seems to have forgotten that monetary policy impacts economic growth and inflation with "long and variable lags."

History has shown that the odds of a soft landing go up only if the Fed is preemptive in cutting interest rates, as opposed to simply hitting the rate-hike pause button. All the central bank has really done by saying it’s willing to be patient when it comes to future rate increases is recognize the reality of slower growth and inflation after stock prices and government bond yields plunged.

In fact, the Fed's dovish about-face was predictable. After all, it was a reaction to the 14 percent plunge in the S&P 500 Index during the fourth quarter, triggered by the market’s belated realization that economic growth was slowing amid concern that the Fed was exacerbating the problem with its intent to keep raising rates.

Furthermore, making room for the Fed’s U-turn was Chairman Jerome Powell’s admission that inflation was indeed "subdued." This came months after ECRI’s inflation downturn call last summer, suggesting that President Donald Trump was right in saying that the central bank was being too hawkish. It’s this inflation cycle downturn that’s dragged consumer price index growth to a 28-month low, while the market’s inflation expectations have also dropped. Notably, the Fed’s pivot was also preceded by a belated pullback in Treasury yields that began in October.

Removing the risk of a recession and sparking a renewed acceleration in economic growth – never mind reigniting inflation pressures – will require much more than the doctrine of primum non nocere, meaning first, do no harm. The Fed would actually need to start a rate cut cycle. Yet, even if that happened in short order, Milton Friedman’s observation that “monetary actions affect economic conditions only after a lag that is both long and variable” virtually guarantee that the economy wouldn’t feel much of an impact this year. Recall that, despite the Fed rate cut cycles starting in January 2001 and September 2007, recessions began two and three months later.

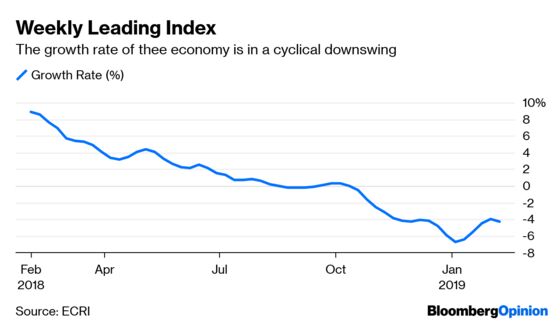

The problem is that, regardless of what Powell has said, the cyclical drivers of economic growth continue to wind down, meaning that the slowdown is set to continue. That’s the objective message from the same array of leading indexes that we used to predict the current U.S. economic slowdown in the context of a global slowdown last year. A case in point is the publicly available U.S. Weekly Leading Index, whose growth rate remains in a cyclical downswing.

If the U.S. slowdown continues until the opening of a recessionary window of vulnerability, within which almost any negative shock would trigger recession, it will be too late for the Fed to head off a hard landing, as it was before the 2001 and 2007-09 recessions.

Today, despite the risk-on rally, a couple of conflicting concerns linger – fears of recession down the road and residual worries about resurgent inflation. To be sure, a recession isn’t imminent, but it’s not off the table. At the same time, a renewed upswing in inflation is nowhere in sight.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Lakshman Achuthan is a co-founder of the Economic Cycle Research Institute in New York.

Anirvan Banerji is a co-founder of the Economic Cycle Research Institute in New York.

©2019 Bloomberg L.P.