Fed Is Reaching Limit on What It Can Do to Lower Mortgage Rates

Fed Is Reaching Limit on What It Can Do to Lower Mortgage Rates

(Bloomberg) -- American home buyers have cheered the drop in mortgage rates to record lows, and now it’s natural to ask if they will head even lower.

The U.S. 10-year Treasury yield has closed within a narrow 0.33% band since the end of the first quarter, and finished as low as 0.57% on April 21. It ended Tuesday at 0.71%. The Freddie Mac 30-year mortgage rate, meanwhile, dropped to a record low 3.13% on June 18.

While the Federal Reserve is unlikely to slow its latest bout of quantitative easing, the 10-year Treasury yield isn’t forecast to drop any further. Wall Street forecasts see it ending this year at 0.94%, which does not bode well for lower mortgage rates.

Any push lower in mortgage rates will likely need to come from somewhere other than the central bank, which has purchased an astounding $765 billion of mortgage bonds since March 16.

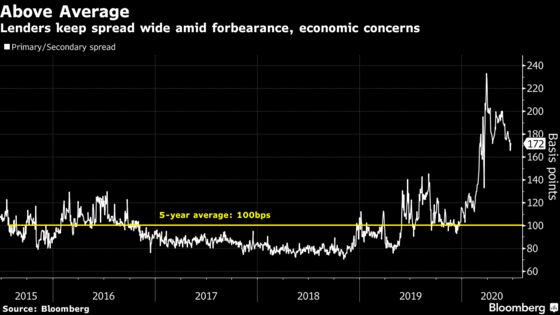

Homeowners should look to mortgage lenders and what is known as the primary/secondary spread, which measures the difference from where the lender can sell a home loan into the market and where they will offer one to you.

That spread has been trending far above its historic average, and has kept mortgage lending rates higher than they otherwise would be. As of Tuesday’s close, that spread was 1.72%, compared to the 1% average seen over the last half decade.

Fed Has Delivered Negative Rates to Mortgage Bond Investors: FHN

The primary/secondary spread is in part a measure of how much risk lenders believe there is within mortgages -- and between the economic damage from the coronavirus and forbearance, it is certainly elevated.

As of June 14, 8.45% of mortgage loans are in forbearance, according to the Mortgage Bankers Association, while the Federal Reserve Bank of Atlanta’s GDPNow index points to a 45.5% collapse in GDP for the second quarter.

Still, should lenders tighten the primary/secondary spread back to its trailing five-year average, Americans could enjoy mortgage rates almost 0.75% less than the current, historic low.

The Federal Reserve’s ability to create credit at will performs wonders, but it may have done all it can do for homeowners. The lending community now holds the reins.

- Christopher Maloney is a market strategist and former portfolio manager who writes for Bloomberg. The observations he makes are his own and are not intended as investment advice

©2020 Bloomberg L.P.