Fed Talk of Taper Rekindles Specter of Wrenching 2013 Tantrum

Fed Talk of Taper Rekindles Specter of Wrenching 2013 Tantrum

(Bloomberg) -- Federal Reserve officials are beginning to split over when they may need to start pulling back on their massive monetary stimulus, drawing nervous glances from investors who remember how markets were roiled during the 2013 taper tantrum.

In the past week, four of the Fed’s 18 policy makers have publicly raised the prospect they may discuss reducing bond buying -- currently running at $120 billion a month -- by year’s end. In contrast, several others have called the debate premature and Fed Vice Chairman Richard Clarida, the most senior central banker to weigh in, has said he doesn’t expect any changes before 2022.

Investors, taking no chances, have pushed up yields on longer-duration Treasuries, steepening the spread between rates on two- and 10-year debt to around the widest in more than three years. They may get more guidance in coming days. Clarida and Governor Lael Brainard both speak on Wednesday, followed a day later by Chair Jerome Powell in his first comments of the year.

“The Fed needs to clarify its position or it risks a taper tantrum, unnecessarily,” said Diane Swonk, chief economist at Grant Thornton in Chicago.

In 2013, in the so-called taper tantrum, yields surged following the unexpected disclosure by then-Fed Chairman Ben Bernanke that officials were thinking about dialing back their asset purchases, provoking severe financial market volatility and a bitter memory among investors.

“Bond investors were all trapped,” said John Herrmann, director of U.S. rates strategy at MUFG Securities Americas, invoking the iconic 1971 rock song from the Who to make his point. “As Roger Daltrey once argued, Treasury bond investors are prepared to argue, we ‘Won’t get fooled again’.”

In December, a unanimous Federal Open Market Committee said it would continue $120 billion a month in asset purchases -- comprised of about $80 billion in Treasuries and $40 billion in mortgage-backed securities -- until there was “substantial further progress” in meeting its goals on employment and inflation. Powell called the guidance “powerful,” but declined to spell out what metrics the committee was looking for to make a change.

That vague wording is open to different interpretations by individual Fed policy makers, and a source of potential confusion among investors. The 10-year Treasury yield is near the highest level since March, while the two-year yield has edged up only slightly -- reflecting the clear signal from the central bank that overnight interest rates will stay near zero through at least 2023.

What Bloomberg Economists Say

“If the Fed tapers in 2021, then I certainly do worry about a taper tantrum. But Powell-Clarida and the doves-moderates camp will not sweat a short-lived inflation flare up. On the contrary, I anticipate the Fed will continue full-bore on QE until 2022.”

-- Carl Riccadonna, chief U.S. economist

Regional Fed presidents including Patrick Harker, Robert Kaplan, Raphael Bostic and Charles Evans have all indicated an openness to discussing a 2021 taper if the economy proves to be strong enough. The rollout of Covid-19 vaccines to the U.S. population, more fiscal aid and continued monetary support are contributing to forecasts of a robust recovery in the second half of the year.

At the same time, even those open to discussing a 2021 tapering are not pushing for action anytime soon. “It’s too early for me to have a strong judgment on that,” Chicago Fed chief Evans said, adding that by June things may be clearer. Vaccine distribution has gotten off to a slow start and further delays would be a setback to the hoped-for strong recovery, the Atlanta Fed’s Bostic noted Tuesday.

Clarida said his forecast didn’t include tapering in 2021, and other Fed officials viewed the outlook as still cloudy.

“It is good to plan ahead and to try to anticipate, but I don’t want to put specific dates on things,” St. Louis Fed President James Bullard said Wednesday during a virtual Reuters event. “We should just leave it at that -- ‘substantial further progress’ -- and see how that develops.”

Powell speaks Thursday at a virtual event hosted by Princeton University and is likely to keep his tone cautious, said Steven Englander, head of North American macro strategy at Standard Chartered Bank Plc.

“I think the debate is premature,” he said.

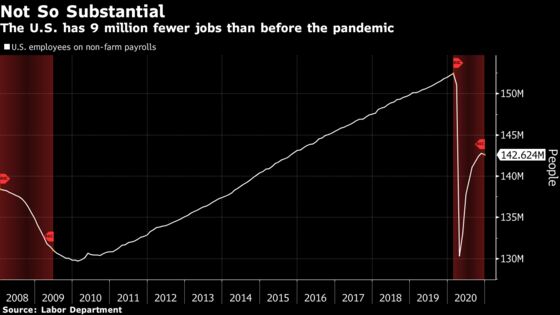

The FOMC in December forecast an unemployment rate of 5% in the fourth quarter of this year, with inflation of 1.8%, both still some way from the committee’s targets. Unemployment -- now 6.7% -- was 3.5% in February prior to the pandemic and 9 million jobs have been lost. Inflation has been mostly short of the Fed’s 2% goal since 2012.

“The conditions for tapering which the Fed itself put in place are that there has to be considerable progress toward the Fed’s goals of full employment and 2% inflation, and I just don’t see that happening this year,” said Chris Low, chief economist at FHN Financial. “It’s just too soon.”

Fed officials have stressed that tapering of bond buying would be telegraphed well in advance to avoid a surge in Treasury bond yields. They haven’t sounded alarmed by the move up in bond yields to date.

“I think we have learned lessons certainly from six or seven years ago,” Richmond Fed chief Thomas Barkin said on Monday, noting that Powell was at the central bank during that episode. “I expect us to do our best to communicate well there.”

©2021 Bloomberg L.P.