Fed’s Tools for Liquidity Crunch Brace for Next Wave in Crisis

Fed’s Tools for Liquidity Crunch Brace for Next Wave in Crisis

(Bloomberg) -- The Federal Reserve and the U.S. government have at least one thing in common in their fight against the coronavirus: they are both struggling to keep up.

The U.S. central bank unleashed some of its biggest weapons over the past two weeks -- to keep banks flush with cash and markets functioning -- but it’s done little to stop investor panic or the widening signs of a coming global recession.

That has investors asking how much ammunition the Fed has left to counter what comes next. There is likely more to come. On Tuesday, a Federal Reserve bank president said she would support a facility that would provide short-term credit to potentially a vast array of corporations that are getting squeezed out of money markets.

“The market has already jumped over the liquidity problem and is laser focused now on the solvency issue,” said John Fagan, principle at Markets Policy Partners, and the former head of the U.S. Treasury Department’s Markets Room.

The Fed has slashed interest rates to nearly zero, plowed money into the money market to boost liquidity, enhanced dollar swap lines with other central banks and announced buying of at least $700 billion of Treasuries and mortgage backed securities to ensure market functioning and keep credit flowing.

Investors are still rattled as they try to gauge how severe the economic impact will be and how long it will last. Stocks fell 12% on Monday for the steepest losses since 1987.

And the House and Senate have yet to pass a bill to help that is big enough to convince investors the government has the economy’s back.

Second-Round Effects

The longer the fiscal response takes the higher the risk of so-called second-round effects where liquidity risks suddenly turn into solvency risk as indebted households lose work and indebted businesses lose customers with not enough government help in sight.

“The thing that could turn this from a temporary shock into a normal recession would be if in the very short term enough business and consumers go bankrupt that trashes their credit lines and sinks banks’ capital,” said Joseph Gagnon, a senior fellow at the Peterson Institute for International Economics in Washington.

The $3.9 trillion municipal bond market, where cities, states and counties raise money for everything from schools to health care systems, is poised for its biggest monthly drop since September 2008, according to Bloomberg Barclays indexes.

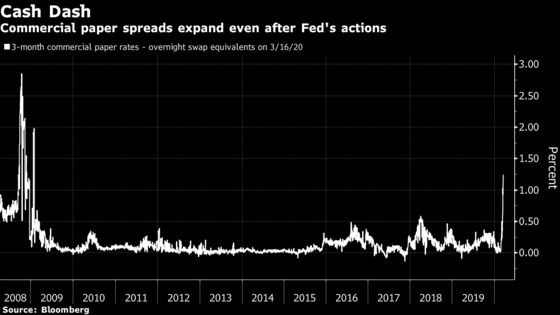

For companies trying to get money via commercial paper, it had gotten to be the most costly this month since 2009 relative to overnight index swaps. Even after the Fed’s actions Sunday, commercial-paper rates tied to even the most credit-worthy companies in the U.S. remained elevated Monday.

On Tuesday Federal Reserve Bank of Cleveland President Loretta Mester said she would back more measures to keep markets functioning including a crisis-era facility to the support commercial paper market. A decision by the Fed could come later Tuesday, Reuters reported, citing sources.

And even after the Fed bolstered its currency swap lines to foreign central banks to ease a global searched for dollar cash, the price to tap that money in currency derivative markets surged on Tuesday.

The Fed is prohibited in what it can do to help individual companies and especially those in bankruptcy, but it has a few more tools left at its disposal to attack a longer, more protracted downturn. They include:

Lending Facilities

The Fed also has the ability to launch facilities to be the lender of last resort -- if market makers and investors retreat from all risk taking.

Under Section 13.3 of the Federal Reserve Act, the Fed would be required to get permission from the Treasury Secretary to create a facility to assist a “broad based” group of companies or entities that are “unable to secure adequate credit accommodations from other banking institutions.”

During the financial crisis, the Fed used lending facilities to support markets for commercial paper, asset backed securities and to provide longer-term funding for banks.

“You need three stars aligned,” to start a facility, said Mark Spindel, author of a book about Congress’s relationship with the Fed. “The Fed, the Treasury and Congress. The Fed has that balance sheet but by law now they can’t use it without political support.”

TAF

One of the many things the Fed may still do to help easing funding conditions is to reduce the stigma still associated with using the discount window by restarting programs such as the Term Auction Facility, according to John Briggs, head of strategy for the Americas at Natwest Markets.

TAF was created during the financial crisis and just last week former New York Fed President Bill Dudley mentioned it as a possibile tool.

More Quantitative Easing

The FOMC said in its statement Sunday that “over the coming months” it will buy at least $500 million of U.S. Treasury securities and $200 billion in mortgage-backed securities. That language left the door open to even more purchases, and potentially for a monthly amount as they did in previous rounds of QE.

“There’s a lot of volatility and that will continue but by adding $700 billion in purchases to the Treasury and mortgage market the Fed’s goal is to bring back confidence and reiterate that this is not a financial crisis now, it’s more a healthcare crisis that has impacts to the economy and corporations,” said Sean Simko, global head of fixed-income portfolio management at SEI Investments Co.

Forward Guidance

The Federal Open Market Committee said Sunday that it expects to maintain the 0%-0.25% range on the federal funds rate “until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals.”

That language suggests the zero rates are contingent on the virus running its course and the economy bouncing back.

If the economic impact is deeper, the Fed could signal to markets that it’s instead tying zero rates to an outcome such as the unemployment rate.

“They need eventually to clarify their commitment about how long they will keep the fed funds rate near zero,” said David Wilcox, a non-resident senior fellow at Peterson. “My guess is they’ll be at the zero lower bound for a long time here.”

Read more: How Cross-Currency Basis Swaps Show Funding Stress: QuickTake

--With assistance from Amanda Albright.

To contact the reporters on this story: Craig Torres in Washington at ctorres3@bloomberg.net;Liz Capo McCormick in New York at emccormick7@bloomberg.net

To contact the editors responsible for this story: Margaret Collins at mcollins45@bloomberg.net, Jenny Paris

©2020 Bloomberg L.P.