Fed’s Regulatory Relief May End Distortion in $124 Trillion Market

Fed’s Regulatory Relief May End Distortion in $124 Trillion Market

(Bloomberg) -- In one fell swoop of regulatory relief, the Federal Reserve has put a massive distortion in the debt market on course to normalize after years of being turned upside down.

At stake is a stubbornly illogical relationship between two of the world’s most important funding markets -- the $17 trillion of U.S. Treasuries and the $124 trillion world of interest rate swaps -- that’s persisted for more than a decade. Such swaps exchange fixed-rate payments for floating-rate ones, and are used by investors ranging from pension funds to insurers, as well as companies managing their future liabilities.

But the relationship between swaps and Treasuries was turned upside down in the aftermath of the financial crisis, with so-called ‘swap spreads’ -- what should be a premium of swap rates over Treasury yields, to reflect the credit risk involved in dealing with a private counterparty -- turning negative.

Taken at face value, negative swap spreads suggest that investors view private counterparties as less likely to default than the U.S. Treasury. In reality, market participants blamed capital constraints and supply and demand dynamics in Treasuries and corporate credit for the distortion.

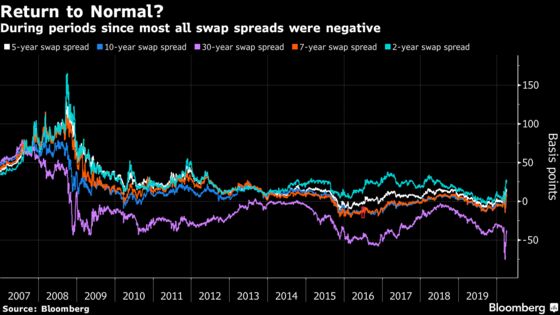

New Normalcy?

With the Fed moving on Wednesday to allow banks to increase leverage in an effort to restore debt-market liquidity and get credit to consumers, the oddity of negative swap spreads is now expected to fade. It may also make disorderly leaps and plunges in Treasury yields less likely.

The Fed exempted Treasuries and deposits from banks’ supplementary leverage ratio (SLR), and that’s set to stoke debt trading and make Treasuries more appealing versus derivatives -- a dynamic that would widen swap spreads and potentially turn them positive across maturities.

“Positive swap spreads would mean the world is right side up again, with economics of investors driving the pricing of derivatives rather than regulatory and other practical constrains on dealers,” said Joshua Younger, head of U.S. interest rate derivatives strategy at JPMorgan Chase & Co. The regulatory “relief is targeted at reducing intermediation frictions more so than incentivizing banks to hold more Treasuries in their investment portfolio.”

Rates on 30-year swaps have been lower than similar maturity Treasury yields for most of the time since October 2008. That anomaly -- which created the negative swap spread -- was once considered to be an impossibility in funding markets since swaps’ floating payments are based on the London interbank offered rate, which has embedded credit risk. The spread was at -40 basis points on Friday, compared to about -42 basis points Thursday and -52 basis points a week earlier.

The Fed said on Wednesday that for one year, the biggest U.S. banks will no longer have to add their Treasuries and reserves into the basket of assets for which they’re required to maintain extra capital. It said the change was “to expand their balance sheets as appropriate to continue to serve as financial intermediaries” because “liquidity conditions in Treasury markets have deteriorated rapidly.”

With the central bank’s balance sheet on course to top $10 trillion due to an array of debt-purchase programs to combat the economic effects of the virus, the regulatory roll-back also helps unlock more bank lending -- even given the resulting rise in reserves that will follow. Net net, it gives banks more space to use their balance sheets in ways that support the Treasury market.

“The SLR had forced banks to really optimize the balance sheet, and in doing that they cut back on repo activity because it is a low-return business,” said Priya Misra, global head of interest rates strategy at TD Securities. “With the Fed’s action, there will be more repo activity and more demand for Treasuries -- both of which will widen swap spreads.”

| Read more |

|---|

|

As always, supply and demand dynamics will impact swap spreads. Right now the U.S. Treasury is boosting issuance of government debt at a torrid pace to fund a $2 trillion fiscal stimulus program.

Treasury Supply Surge Begins With Next Week’s Coupon Auctions

While an influx of Treasury supply would tend to narrow swap spreads as it pushes Treasury yields higher, strategists see the impact of the regulatory roll-back winning out, putting spreads on a path of expansion. The Fed is helping that dynamic by buying up lots of the Treasury’s debt -- thereby limiting the net supply to the private sector.

It all adds up to a new world order, where the eerie past -- when swap spreads for nearly all maturities were negative -- is firmly in the rear view mirror. Strategists at banks including TD Securities and Societe Generale predict the Fed will ultimately keep the SLR tweak well beyond a year.

A key gauge of Treasury liquidity known as market depth, or the ability to trade without substantially moving prices, plunged last month to levels last seen in the 2008 crisis, according to data compiled by JPMorgan.

Both dealers and commercial banks are bloated with debt, given the double whammy of them needing to meet regulatory mandates and outsize Treasury issuance.

“Spread widening is going take place across the curve, with it especially strong in the long-end where dealers’ balance sheet constraints were most pronounced,” said Subadra Rajappa, head of U.S. rates strategy at Societe Generale. “The SLR change will bolster liquidity as well. The big move recently in 30-year bonds was really due to these constraints and because dealers’ holdings of Treasuries have surged.”

©2020 Bloomberg L.P.