Did the Markets Break Jerome Powell? We’re About to Find Out

Did the Markets Break Jerome Powell? We’re About to Find Out

(Bloomberg Opinion) -- This week’s Federal Reserve decision will be the most consequential one yet under the leadership of Chair Jerome Powell.

Sure, Fed officials will almost certainly leave interest rates unchanged, and they won’t do anything with the central bank’s balance sheet beyond what they have previously indicated. But the move in financial markets has been so swift, with traders so convinced that policy makers will lower interest rates imminently, that every change in their statement’s wording, every syllable uttered by Powell during his press conference, and any tweak in the “dot plot” will be scrutinized as much as ever. After all, vast sums of money (not to mention strategists’ reputations) are riding on a decidedly dovish shift.

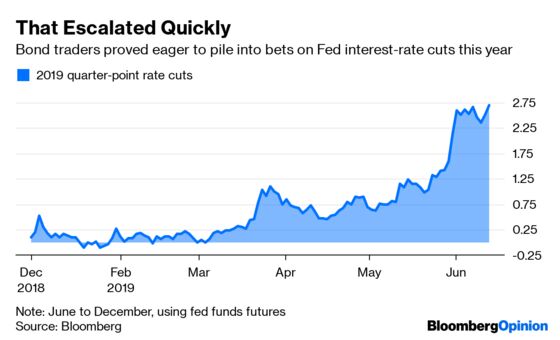

It truly seems as if bond traders have gone too far and are setting themselves up for disappointment. They have priced in a 92% chance of a quarter-point rate reduction in July and 2.75 cuts by the end of the year. Barclays Plc strategists would say that’s too conservative — they’re calling for a 50-basis-point cut next month and an additional 25 basis points in September in one of the more aggressive Wall Street forecasts. Basically, as Michael Purves at Weeden & Co. put it, markets are “almost taunting the Fed.”

Make no mistake, Fed officials have a number of reasons for caution. While President Donald Trump tabled threatened tariffs on Mexico, a potentially drawn-out trade war with China looms large. U.S. inflation continues to fall short of the central bank’s stated 2% target, while the University of Michigan's gauge of expected price changes fell to an unprecedented low late last week. And the bedrock of this rate-hiking cycle — a seemingly unstoppable labor market — is showing early signs of slowing, with American companies adding just 75,000 workers in May, missing estimates for a 175,000 gain.

All of this lines up with Powell’s pivot since the end of last year, from signaling further interest-rate increases and keeping the balance sheet runoff on “automatic pilot” to being patient and winding down the bank’s “quantitative tightening.” He and other policy makers have clearly indicated this is as far as they’ll go in tightening monetary policy this time around.

That’s not the same thing as saying they’re ready to begin easing.

The problem is, bond traders (and, admittedly, financial journalists) don’t care about that nuance. Conviction that the Fed is done hiking, by definition, means that the next move in interest rates will be lower, making it a matter of “when,” not “if.” After Powell said earlier this month that “as always, we will act as appropriate to sustain the expansion,” it was perceived as opening the door to cutting interest rates, even though he didn’t really say that. RBC Capital Markets had a brilliant report that noted the “weak” May jobs number was actually perfectly consistent with the Fed’s outlook. No matter; traders scurried to wager on easing sooner rather than later in the wake of the payrolls data.

So here we are, with markets brazenly taunting the Fed. Will Powell dare to defy them?

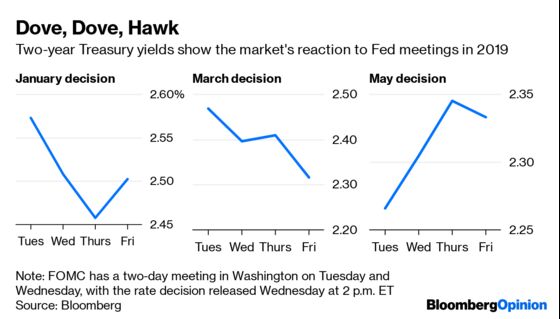

Unfortunately, recent history doesn’t provide a clear answer. In January, I wrote that the Fed was officially at the market’s mercy, given a decision that was seen as giving in to the late-2018 equities tantrum. Two-year Treasury yields fell about 12 basis points in the following 27 hours. In March, it was more of the same, with central bankers managing to beat traders’ lofty dovish expectations by shifting the dot plot to show zero interest-rate increases in 2019, compared with two in December. Again, two-year yields tumbled, ending the week 15 basis points lower than they were before the decision.

Things went differently last month. After what looked like another bond rally in the making, Powell managed to entirely reverse it, and then some, by highlighting “transitory factors” keeping inflation subdued. “Our baseline view remains that with a strong job market and continued growth, inflation will return to 2% over time,” he said. Two-year yields climbed eight basis points in the next 27 hours, to 2.35%, a level that almost exactly aligns with the current effective fed funds rate. In other words, bond investors were more or less on board with the idea of a “patient” Fed holding rates where they are.

Obviously, the outlook has changed since then, but not nearly to the extent that market pricing would indicate. As one example, Citigroup Inc.’s U.S. economic surprise index is at the same level it was on May 1, the day of the Fed’s most recent decision. The persistently negative reading is hardly a cause for celebration — it signals data have been worse than expected — but it could just as likely indicate that forecasters have to come to terms with the expansion turning 10 years old and serve as an early warning that the economy is rolling over. As RBC’s Tom Porcelli and Jacob Oubina noted, it’s all about the narrative.

Given all that, which Powell will investors get? The one who gives them what they want and more, or the one who is willing to push back?

I believe that deep down, Powell would strongly prefer to keep interest rates where they are and only begin easing when he and other officials observe clear and persistent signs of weakness. The U.S. economy is not at that point yet. It doesn’t help that Trump continues to pound the table for lower rates, in what has become a now-commonplace break from recent presidential history, while simultaneously trumpeting the “tremendous potential our Country has for GROWTH.”

If I had to guess, the dot plot will turn flat, with the current 2.375% median fed funds rate extending through at least 2021. That’s the definition of patience. Then, Powell will reiterate in his press conference that the Fed stands ready to act as appropriate. In doing so, he preserves the option to lower interest rates as soon as July or September, without making any sort of explicit commitment. If that’s seen as insufficiently dovish, as some rates strategists suggest, then tough.

Powell, at the helm of the world’s most influential central bank, can afford to be more deliberate than traders looking to get ahead of the next big move. At the same time, the cacophony of calls for rate cuts is tough to shut out. Should he capitulate entirely, he will be permanently viewed as a Fed chair who was broken by bond traders.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.