Some Emerging Markets Can Withstand Trump Shock on Trade

Some Emerging Markets Can Withstand Trump Shock on Trade

(Bloomberg) -- For all the angst over the prospect of a U.S.-China trade war, there’s little chance it will trigger an across-the-board meltdown in emerging markets like last year.

If this week’s high-stakes talks in Washington fail to signal a deal’s in the pipeline, the clamor for the safety of U.S. Treasuries and the dollar may be accompanied by renewed turmoil in the weakest pockets of the developing world, such as Turkey, Argentina and South Africa. But there are plenty of nooks and crannies within emerging markets that would still attract yield-chasing investors.

The difference this time is the Federal Reserve’s now well-documented dovish tilt. At least two policy makers currently favor rate cuts, even though Chairman Jerome Powell said after last week’s two-day meeting he saw little reason to move in either direction. That’s a far cry from a year ago, when the Fed was firmly in tightening mode. All of which means the hunt for higher yield may just get another lease of life.

Here’s a non-exhaustive list of assets investors may seek out even if trade tensions worsen:

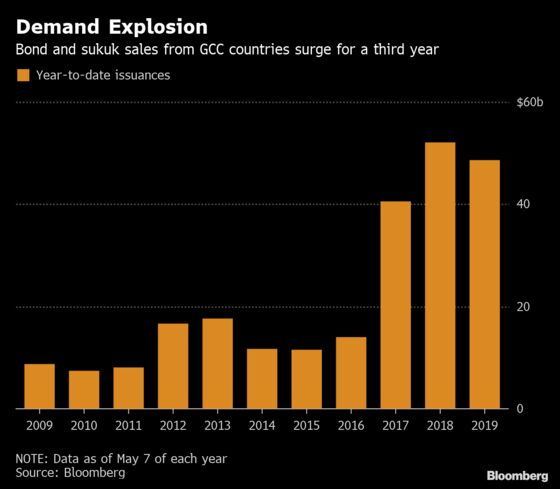

GCC Bonds

Emerging-market dollar debt has led this year’s rebound, a trend that may strengthen if Donald Trump follows up on his threat to raise tariffs on Chinese goods.

That’s good news for the Middle East.

Global investors are warming to the region, encouraged by Saudi Arabia’s impending entry into MSCI Inc.’s emerging-market indexes, this year’s oil rally and the proposed initial public offering by Saudi Aramco, the kingdom’s state-owned energy giant. Gulf bond issuers have raised more than $49 billion this year, with demand routinely exceeding the debt on offer by several times.

Bond sales by Gulf Cooperation Council borrowers may increase 15 percent on year to $90 billion in 2019, according to Franklin Templeton Investments. GCC nations are undergoing a structural shift away from their reliance on bank loans toward financing via bonds, and with foreign investors relatively underexposed to the region, a surge in inflows is in the offing, Templeton said.

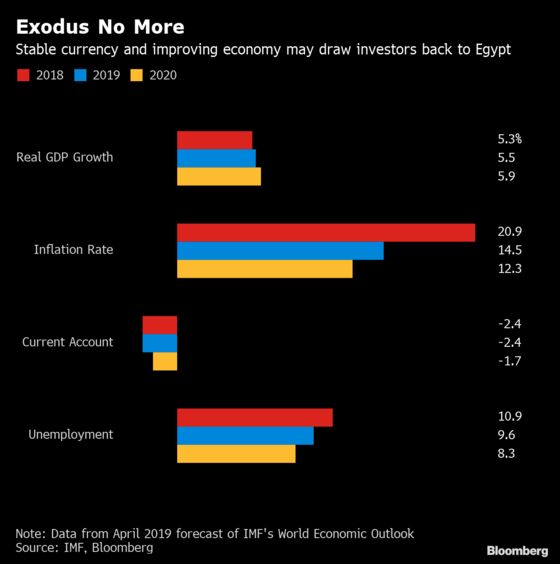

Stable Currencies

Floating currencies backed by central-bank capacity to support them have an irresistible charm to global investors, especially carry traders. The Egyptian pound may be one of those because it enjoys the best of both worlds.

While the North African nation is seeking to consolidate the economic overhaul implemented under a $12 billion International Monetary Fund program expiring in November, there are signs of an economic turnaround. Growth is forecast to accelerate in 2019 and 2020, while inflation, the current-account deficit and unemployment are all projected to ease, according to the IMF.

That’s encouraged the government to target lower yields on domestic debt in the new fiscal year, confident that its securities will remain coveted by investors.

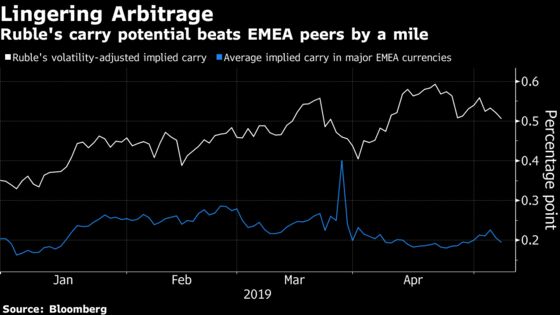

Oil Exporters

Think of a country that has current-account and budget surpluses, a currency with high carry-trade potential and a main export whose price has climbed about 29 percent this year. And now think of one that’s not in President Donald Trump’s cross-hairs right now.

Russia checks all those boxes.

That’s why the ruble is proving to be such a good trade for investors in 2019. And even after a world-topping 8.8 percent carry return, the currency’s attraction hasn’t waned. Its implied carry -- a measure of interest-rate arbitrage adjusted for expected volatility -- is almost triple of the average in emerging Europe, Middle East and Africa.

With inflation slowing for the first time in nine months and one of the highest real yields in the developing world, Russia looks set for possible rate cuts this year. That may spur investors to lock in bond yields at current levels.

To contact the reporter on this story: Srinivasan Sivabalan in London at ssivabalan@bloomberg.net

To contact the editors responsible for this story: Dana El Baltaji at delbaltaji@bloomberg.net, Justin Carrigan

©2019 Bloomberg L.P.