Congratulations, Market. The Fed Is Officially at Your Mercy.

Congratulations, Market. The Fed Is Officially at Your Mercy.

(Bloomberg Opinion) -- Financial markets demanded that Federal Reserve Chairman Jerome Powell ease up on tightening monetary policy. For most of his tenure, he didn’t let equity price swings knock the central bank off course. Until now.

Perhaps the most honest instant reaction on Wall Street came from Jim Cramer.

Yes, that’s precisely what the other Fed officials did. Policy makers said they would be “patient” on any further rate moves and, even more important for markets, signaled that they were flexible on the path for reducing its balance sheet. The Federal Open Market Committee’s statement twice refers to “financial developments.” Here are the two key passages (Powell read the first one verbatim in his press conference):

“In light of global economic and financial developments and muted inflation pressures, the Committee will be patient as it determines what future adjustments to the target range for the federal funds rate may be appropriate to support these outcomes.”

“This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.”

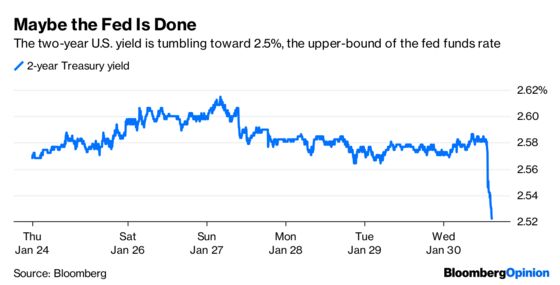

Bloomberg News’s Craig Torres called it “a substantial pivot.” Markets interpreted it as a full-blown capitulation. The two-year Treasury yield, the most sensitive coupon-bearing maturity to Fed policy, tumbled 4 basis points to 2.53 percent. The yield curve “bull steepened,” a classic move for when the Fed is laying off short-term rate increases. U.S. stock markets soared.

I wrote on Jan. 4 that Powell seems to have decided that the stock market’s December tantrum was too noisy to ignore, based on how he has shifted his tone. He and other officials cemented that view in the latest statement. On top of that, he disclosed in his press conference that the FOMC is evaluating the appropriate timing for the end of the central bank’s balance-sheet runoff and that officials would be finalizing plans at coming meetings. That’s a far cry from what he once described as “automatic pilot.” I don’t think he wanted to give such an explicit exit plan but was backed into a corner by financial-market volatility. He even said he doesn’t want the balance sheet to cause turbulence.

There’s also the fact that Powell is suddenly worried about the global economy. Last year, it seemed as if the chairman had convinced the markets that it wasn’t the world’s central bank — it would focus on the domestic economy and react accordingly. Now, he mentioned potential slowdowns in China and Europe. Germany, after all, just cut its forecast for 2019 gross domestic product to 1 percent from 1.8 percent.

It’s entirely possible at this point that the Fed is done raising interest rates for this cycle. Bloomberg News’s Rich Miller asked an excellent question at the press conference: Can “future adjustments” mean a hike or a cut? Powell largely dodged, saying it will depend on the data. But reducing rates wasn’t ruled out. After that, Treasuries extended gains.

BMO Capital Markets strategist Jon Hill called it an “aggressively dovish pause.” That sounds about right. For anyone who wanted the Fed to slow down, Powell did even better: He brought the Fed to a grinding halt.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.