Fed Guidance Seen Coming by September and Linked to Inflation

Fed Guidance Seen Coming by September and Linked to Inflation

(Bloomberg) -- Federal Reserve policy makers will most likely link their guidance on the future path of interest rates to inflation, and will reveal that guidance by September, according to economists surveyed by Bloomberg.

The Federal Open Market Committee holds its next meeting July 28-29. Survey respondents expect minimal change in the policy statement released at 2 p.m. Washington time at the conclusion of that gathering.

One reason for the committee to do nothing dramatic at this meeting: the next fiscal stimulus package that is being hashed out in Congress. “The details of the upcoming fiscal package will be an important consideration as the Fed deliberates the degree of longer-term monetary accommodation,” Brett Ryan, senior U.S. Economist at Deutsche Bank Securities, wrote in his survey response.

Forward Guidance

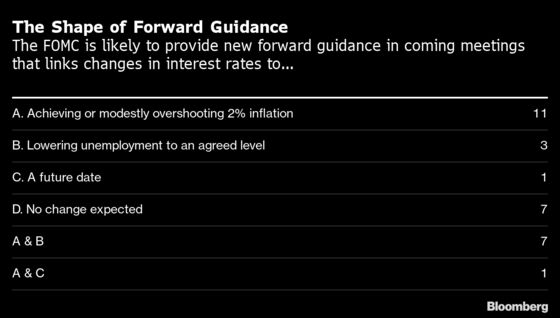

Officials have pledged to keep rates near zero until they’re confident the economy “has weathered recent events and is on track to achieve its maximum-employment and price-stability goals.”

Nearly two-thirds of the 30 respondents to the July 17-22 poll expected the FOMC will link eventual liftoff in the federal funds target range to achieving, or modestly exceeding, the central bank’s 2% inflation target. Of that group of survey participants, seven said guidance will also include a reference to unemployment. Only three respondents said guidance would refer only to unemployment.

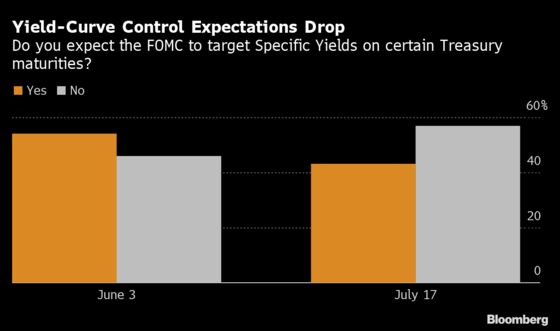

Relative to the a similar survey in early June, the poll also showed a drop in expectations for the adoption of yield-curve control -- a policy that involves setting target yields for certain maturities of Treasury securities. The proportion of economists anticipating such a policy fell to 43% from 54% in June. Those who still anticipate its use pushed back the timetable, many to next year.

“With markets functioning well and longer-dated yields remaining at such low levels, the Fed has little need to alter its language or stance at this stage,” wrote James Knightley, chief international economist at ING Financial Markets. “Should, in the months ahead, yields come under upward pressure due to the scale of bond issuance, then yield-curve control would become much more likely, but for now that is not our base case.”

The survey results on forward guidance and yield-curve control reflect the preference of policy makers revealed by the minutes of the June 9-10 FOMC meeting, released by the Fed on Jul 1.

They showed a “number” of officials favored tying future policy moves to inflation. That could involve waiting for “a modest temporary overshooting of the committee’s longer-run inflation goal” of 2%. The minutes also made clear FOMC members had many questions about capping yields and showed no readiness to embrace the strategy.

Most survey respondents said they do not expect policy makers at the upcoming meeting to shift the stated purpose for the Fed’s buying of Treasuries and mortgage-backed securities toward explicitly stimulating economic activity. The purchases are currently aimed at ensuring “smooth market functioning.” They also showed very little expectation the committee will wrap up its monetary policy framework review at this meeting.

Worries over deflation have also subsided somewhat among economists. Asked to assign a probability of core PCE inflation dropping below zero for three straight months within the next two years, the median response was 15%, down from 25% in June.

©2020 Bloomberg L.P.