Faster QE Is On the Menu at Bank of Canada: Decision Day Guide

Faster QE Is On the Menu at Bank of Canada: Decision Day Guide

(Bloomberg) -- Bank of Canada Governor Tiff Macklem gets a chance on Wednesday to say how much of the government’s record spending he intends to finance.

Macklem, in his first policy decision since taking over as governor June 3, will need to recommit to large-scale asset purchases in order to keep up with an unexpectedly large jump in government spending. The bank releases its rate setting and Monetary Policy Report at 10 a.m. in Ottawa, with a press conference to follow at 11:15 a.m.

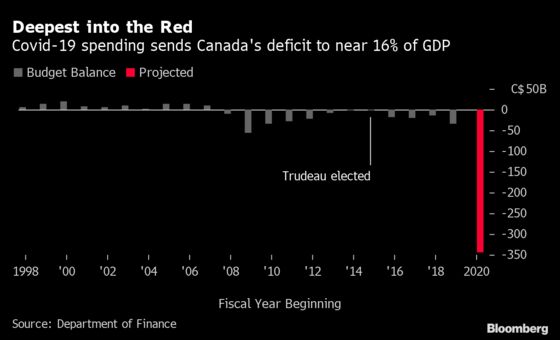

Prime Minister Justin Trudeau unveiled plans last week to run up historic deficits to pay for Covid-19 related measures, and officials now expect bond issuance to exceed C$400 billion ($293 billion) this year, more than triple last year’s levels.

Since early April, the central bank has added almost C$7 billion in federal bonds a week to its balance sheet to sop up the supply, becoming the government’s main financier through the creation of new money. The process, known as quantitative easing, allows policy makers to keep borrowing costs low, an essential ingredient for any recovery.

“We know what issuance is going to look like now and the Bank of Canada may react to that and adjust” their bond buying program, Royce Mendes, an economist at Canadian Imperial Bank of Commerce, said by phone.

The crisis has taken the Bank of Canada into uncharted waters, forcing it to cut the benchmark rate to near zero, injecting hundreds of billions in cash into financial markets and undertaking the first-ever foray into large-scale asset purchases. The current policy is to buy at least C$5 billion in government bonds until the recovery is “well underway,” effectively a signal it plans to keep borrowing costs as low as possible for as long as possible.

Macklem is expected to reinforce that strategy Wednesday, possibly by tweaking policy as early as this rate decision. Options include raising the minimum amount of bonds it plans to buy, or providing more explicit guidance about how long it plans to keep rates low.

“It may be prepared to work the guided range of purchases well above the minimum of the at least C$5 billion per week amount it is implementing,” Derek Holt, head of capital markets economics at Bank of Nova Scotia, said in a report to investors. “It may be helpful to further define program duration beyond the vague until-the-recovery-is-well-underway guidance in such fashion as to inform the stock and period of such purchases.”

Another possible change could be a shift toward yield curve control, where the central bank targets a specific medium-term interest rate.

| What Bloomberg’s Economists Say |

|---|

“Bloomberg Economics expects the BoC will lift the pace of weekly government bond purchases as early as this meeting -- they are already proceeding at a faster clip than the initially announced C$5 billion per week.” --Andrew Husby, Bloomberg Economics Terminal subscribers can read the full report here |

Markets are expecting the bank to keep its benchmark interest rate unchanged at 0.25% for at least two more years, at a level the bank considers its effective lower bound. Both Macklem and his predecessor, Stephen Poloz, have indicated that making rates negative would be one of the least desirable options.

Five of 10 economists in a Bloomberg survey expect Macklem to eventually introduce forward guidance, while a smaller proportion see the bank ramping up bond purchases or adopting yield curve control over the next few months. Economists anticipate the central bank’s balance sheet -- currently at about C$530 billion, or 23% of gross domestic product -- will max out at about 30%.

New Forecasts

Macklem is expected to deliver a more extensive set of quarterly forecasts this time compared with April, and has promised a “central scenario,” though it’s unclear how detailed the numbers will be.

The economy seems to have avoided the worst-case scenario -- a roughly 30% contraction -- outlined in the bank’s previous monetary policy report in April. But the latest projections will probably show an economy operating with plenty of excess capacity over the next two years, providing more than enough justification for loose monetary conditions.

Macklem has already signaled as much, using his first public appearances as governor to underscore his view the economy will take a long time to fully recover from the Covid-19 lockdowns.

©2020 Bloomberg L.P.