Peak Earnings Fears Loom Over Industrials

Peak Earnings Fears Loom Over Industrials

(Bloomberg Opinion) -- Earnings season is going to be an obstacle course for industrial companies.

Swollen profit estimates and high valuations have left companies with little wiggle room as they combat trade tensions and higher bills for everything from materials to labor and freight. Economic data point to generally strong industrial spending for the time being, but investors are looking for any sign that we might be nearing a peak in earnings. Fastenal Co. — a distributor of factory-floor basics whose results are often a harbinger for its industrial customers, which report in the coming weeks — unofficially kicked things off on Wednesday. The subsequent stock drop is an ominous sign.

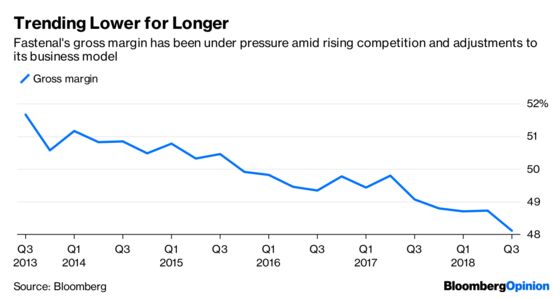

Fastenal reported a 13 percent increase in third-quarter net revenue but retained only about 48 cents of each dollar of sales in gross profit. That was a decline from the year-earlier period, and Fastenal missed analysts’ estimates for a gross margin of 48.6 percent. Some company-specific factors are certainly at play. Fastenal’s gross margin has been a focus ever since Amazon.com Inc. stormed into industrial distribution, bringing with it the price transparency and convenient shopping experience of its consumer website.

To stay competitive, Fastenal ramped up its pursuit of large national accounts, which tend to be more stable sources of revenue but are less profitable because those customers receive discounts for buying in bulk. It has also invested in vending machines for industrial goods and on-site services that more deeply ingrain it in its customers’ supply chain and make its offerings more difficult to replicate. These moves should help limit the Amazon threat, but they come at a cost to profitability: i.e. the product and customer mix that Fastenal cited as a reason for its gross margin decline.

It’s debatable how worrying that margin slippage is long term if Fastenal ends up building a more defensible revenue stream and market share. Some analysts have wondered, however, at what point margin pressure at the distributors starts impacting the ability of industrial companies such as 3M Co. to push through price increases, a concern that becomes more relevant as cost inflation continues to creep up.

Fastenal did realize higher pricing in the third quarter, but it also saw a myriad of puts and takes including higher freight costs and a 10.3 percent increase in employee-related expenses because of wage inflation, increase in headcount and higher bonuses. Interest expense also increased. Those cost pressures are likely to be a refrain among industrial companies and lead to some messy reports this earnings season.

While these kinds of rising expenses are common later in the earnings cycle, complicating the matter is President Donald Trump’s escalation of trade tensions with China. Most industrial companies’ guidance for the full year reflects Trump’s steel and aluminum tariffs and the first $50 billion of tariffs on Chinese imports, whose impact was largely minimal. But few CEOs were incorporating the recently announced tariffs on another $200 billion of Chinese goods, or Trump’s threat to enact levies on yet another $267 billion of imports. Those actions are likely to have a more meaningful effect on cost inflation and could force companies to accelerate price increases, perhaps to the point of knee-capping growth.

Of note, Fastenal said that sales increased to 79 of its top 100 customers in the third quarter, compared with 80 in the second. That is a fairly minor sequential stepdown and not particularly alarming on its own, but coupled with the higher costs and gross margin disappointment, there are enough caution signs for industrial bears to latch on to.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2018 Bloomberg L.P.