Don't Ignore These Industrial Warning Signs

Don't Ignore These Industrial Warning Signs

(Bloomberg Opinion) -- Industrial stocks have rebounded from their Christmas Eve low, outpacing the broader market recovery. But early earnings results suggest investors were right to be Grinches.

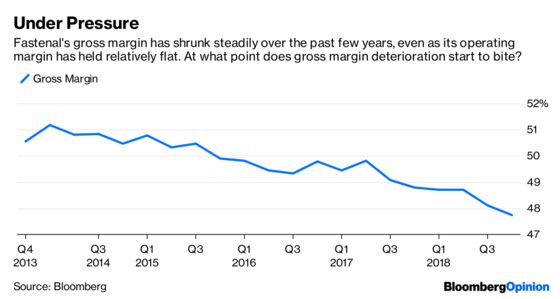

Fastenal Co., a distributor of factory-floor basics and office products, reported yet another slump in its gross margin, with the profitability benchmark shrinking 110 basis points to a below-estimates level of 47.7 percent. The company blamed rising costs, particularly in freight, and an unfavorable mix of orders for the decline. Of particular concern was Fastenal’s disclosure that its price increases failed to offset input-cost inflation in the fourth quarter – and that’s without a significant impact from tariffs. The company expects tariffs to affect sales and profit in 2019.

Industrial distributors have a strong track record of pushing through price increases, so Fastenal’s struggle to get traction with that at this stage is worrisome. The company’s status as a supplier for heavy-equipment and other industrial-goods manufacturers has made it a bellwether for what’s coming when its customers start reporting results. The gross-margin miss that Fastenal revealed in its third-quarter results and management’s acknowledgement of the difficulty in predicting the impact of President Donald Trump’s trade war with China preceded signs of peaking margins and sales at the likes of 3M Co. and Caterpillar Inc.

This latest shortfall makes the 12 percent gain in the Industrial Select Sector SPDR fund off the two-year low it hit in December look a bit premature. Growth is still holding up for manufacturers; Fastenal reported a 13.2 percent gain in daily sales in the fourth quarter. But that momentum looks unsustainable and is showing signs of fading. A measure of new orders tracked by the Institute for Supply Management plunged 11 points in December, one of the biggest declines in the past 30 years. The Federal Reserve’s Beige Book economic survey released Wednesday cited a decline in business activity at wholesale distributors.

The prospect of deceleration matters for Fastenal because it’s historically been dependent on revenue growth to boost earnings. In the absence of margin improvement to counteract any deceleration, it’s tough to justify a premium valuation, notes Melius Research analyst Jake Levinson. It’s unclear where that profitability lift comes from as Fastenal attempts to carve out a competitive edge amid the upheaval wrought by Amazon.com Inc.’s push into industrial distribution. Fastenal’s network of vending machines for dispensing industrial parts and on-site inventory-management services would be difficult for the e-commerce giant to replicate and likely helps insulate its market share, but selling products this way comes at a cost to profitability.

Fastenal shares rose 4 percent as of 9:53 a.m. in what may be a sign of relief that adjusted earnings per share for the fourth quarter matched analysts' estimates despite the gross margin miss. The company also boosted its quarterly dividend to 43 cents per share.

Investors shouldn’t ignore the the challenges Fastenal faces. Some are unique – but its mix of higher costs and the risk of a sales slowdown isn’t. Expect to see more of this throughout the quarter.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.