Express Is Exhibit A of Retail's Execution Problem

Express Is Exhibit A of Retail's Execution Problem

(Bloomberg Opinion) -- We’ve just gone through another spasm of news that smacks of trouble in the retail industry: Payless Shoe Source and Gymboree are going out of business; Diesel USA has filed for bankruptcy. And on Wednesday morning, Express Inc. became the latest retailer to report gloomy holiday results and a truly dismal outlook, despite a strong consumer backdrop.

But don’t mistake these developments for signs that physical stores are doomed. In fact, brick-and-mortar retailing, as a format, is holding up fine. It’s just that certain companies are doing a lousy job at it.

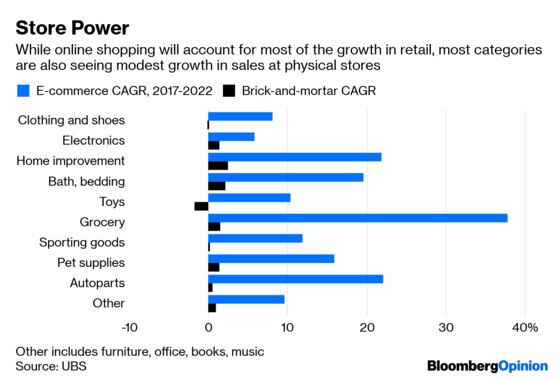

Take a look at these estimates for retail sales growth from UBS analysts. As you might expect, online is where most of the gains will be over the next few years. But the model also includes projections for modest annual brick-and-mortar increases in most retailing categories:

Yes, physical stores play a different role in the digital era. But they still have relevance, remain destinations for many, and offer growth potential. Legacy retailers have only themselves to blame if they can’t keep this part of their business healthy.

Take Express. The apparel chain’s comparable sales sank 6 percent in the fourth quarter, contributing to a 1 percent decline on this measure for the full year. E-commerce sales growth for 2018 was a robust 20 percent, however, so we know the grim comparable sales result was caused by its slumping physical stores. But this isn’t evidence of a broader trend: UBS says brick-and-mortar sales for the clothing and shoes category overall should largely be holding their own. That leaves Express with few excuses for such a dramatic flight away from its mall outposts.

The retailer has said that it’s recently seen bleak traffic patterns at its stores, with a particular deceleration in its women’s business in the early part of the holiday season. A “highly promotional” environment was part of the challenge. Sorry, but I haven’t seen evidence that the seasonal deals deluge was markedly more aggressive than usual in 2018 among Express’s competitive set. And in an economy that’s still pretty strong, if all people need to be lured away from your mid-priced apparel business is a 20 percent-off coupon, you’re doing something wrong.

Express doesn’t have anything close to a clear path to improvement. The company issued first-quarter guidance for an abysmal 9 percent to 11 percent drop in comparable sales, and didn’t even issue full-year guidance, a move it attributed in part to “current variability in comparable sales trends.” The other factor is that is searching for a CEO after David Kornberg’s departure in January.

The new leader at Express needs to sharpen its merchandise selection, particularly in its women’s business. And it should be moving faster on initiatives such as rolling out personal styling services, which would give people more reason to visit the stores. The company has been converting dozens of locations from full-price to outlet stores, on the grounds that those particular locations are becoming more productive. But the comparable sales rut for the company overall makes me wonder: Is the brand being tarnished by doing a heavier share of business in this value-oriented category?

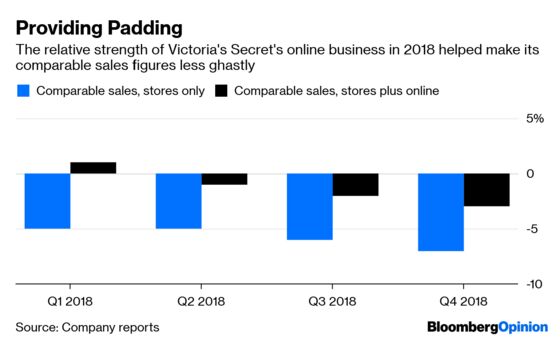

Other retailers are stuck in a similar dynamic. Victoria’s Secret regularly sees its dismal physical store sales somewhat tempered by solid online growth. In each quarter so far in 2018, Bed Bath & Beyond has said that its “strong” online sales were offset by “mid-single-digit” declines in store sales. But the bath and bedding category is expected to see 2.2 percent annual sales growth in the brick-and-mortar channel through 2022.

This makes it obvious that these chains aren’t some preordained victim of changing shopping habits – they have an execution problem.

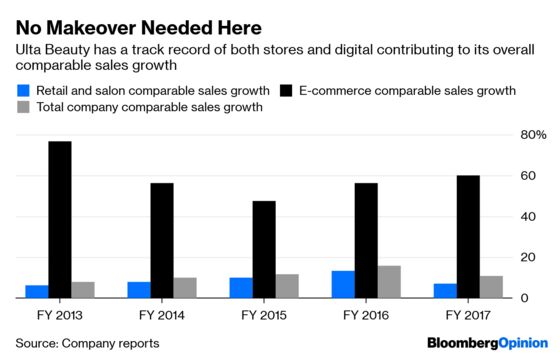

We see plenty of cases of the old guard learning to draw strength from both digital and physical retailing. Walmart Inc. and Target Corp. are the most prominent examples of chains that have seen both their stores and digital businesses contribute to comparable sales growth. It’s not just big boxes: Ulta Beauty Inc. also consistently delivers growth in both channels.

To be sure, I don’t think the opportunity to achieve sales growth in physical stores should be taken as an excuse for retailers to cling to locations that are underperforming. It seems inevitable that chains might find certain locations are becoming less profitable as some customers embrace online shopping, and they should be proactive about dumping them.

But the potential for growth in the brick-and-mortar business should remind retailers not to neglect stores as they chase e-commerce dollars. This is why Target, for example, is smart to invest in hundreds of store remodels, and why DSW Inc. is right to try outfitting its shoe stores with manicure stations. And retailers should continue investments in technology that help allocate in-store labor effectively and ensure sure they don’t run out of stock.

Retailers’ fate doesn’t hinge on fast-growing e-commerce alone. Stores still matter, and we should judge these companies on their ability to remain competitive in both channels.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Sarah Halzack is a Bloomberg Opinion columnist covering the consumer and retail industries. She was previously a national retail reporter for the Washington Post.

©2019 Bloomberg L.P.