Exotic Notes Get a Risky New Twist in a Yield-Starved Market

Exotic Notes Get a Risky New Twist in a Yield-Starved Market

(Bloomberg) -- Structured-product issuers are breaking new ground in the most yield-starved market in Europe.

An arm of commodities specialist Marex Spectron sold a Swiss-franc structured note last month issued with subordinated Tier 2 capital rather than senior debt, touted as the first deal of its kind. The five-and-a-half-year securities offer both a hefty coupon and a return linked to the country’s benchmark stock index.

The mechanics behind the transaction will be familiar to structured products investors, but it’s thought to be the first time a subordinated debt issuer uses the securities to meet capital requirements.

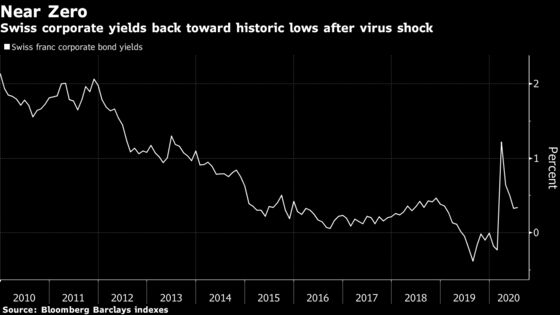

The deal comes as European governments unleash unprecedented monetary stimulus designed to tackle the fallout of the coronavirus pandemic, suffocating yields. While the use of riskier debt adds an extra layer of complexity to the derivatives-powered product, it also juices the coupon.

“The classic structured note market is very developed and efficient but the investor base is starved of yield,” said Nilesh Jethwa, chief executive of London-based Marex Solutions, which helped arranged the transaction. “Structured products backed by subordinated debt is an elegant solution.”

Marex Financial Products had to get approval from the U.K.’s Financial Conduct Authority to issue the notes, a process that took around two months, according to Jethwa. He said the firm typically targets qualified institutional investors such as pension funds.

The principal-protected product pays a 2.55% coupon and delivers any gains in the benchmark Swiss equity index at maturity. Jethwa declined to disclose its size.

In a typical structured trade, banks issue zero-coupon bonds and use the difference between the par value and issue price to purchase derivatives. But the ever-shrinking discount rate limits the returns they can offer.

The lack of income is particularly acute in Switzerland, where 10-year government bond yields are trading at -0.43% and a quarter of corporate bonds in the Swiss currency guarantee losses if held to maturity, based on Bloomberg Barclays indexes.

Tier 2 bonds offer higher return than senior notes, as they take losses first if the issuer goes under. This means the discount is bigger, allowing structurers to build more lucrative payouts.

“Some banks could issue such notes but for small structures and with a limited investor pool,” said Sebastien Barthelemi, head of credit research at Kepler Cheuvreux SA.

The difficulty in raising substantial amounts of capital via complex structures may limit widespread adoption. The average size of a Tier 2 bond issued by a European bank this year stands at almost $550 million. But for Marex, the products could present an alternative for lenders.

“Banks have successfully leveraged structured notes to raise liquidity,” said Jethwa. “However we also think this is an efficient way of raising capital.”

©2020 Bloomberg L.P.