Everyone Is Running Up Debt Except America’s States and Cities

Everyone Is Running Up Debt Except America’s States and Cities

(Bloomberg) -- America’s states and cities may be the only ones that aren’t running up their credit cards.

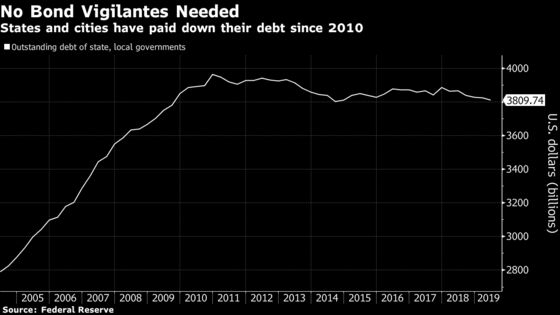

The outstanding debt of U.S. state and local governments shrank for the fourth straight quarter in the three months ended in June, dropping by $14.6 billion to about $3.8 trillion, according to Federal Reserve Board figures released Friday. That stands in contrast the federal government, households and businesses, all of which stepped up their borrowing.

The figures underscore the fiscal restraint that has reigned in the nation’s statehouses since the Great Recession, which forced governments to cut jobs and slash spending to make up for the massive budget shortfalls they were left with when the economy collapsed. Even with the interest rates on municipal bonds at the lowest since at least the early 1960s, states and cities have been hesitant to borrow and are saving for the next downturn instead. As a result, the municipal-securities market is smaller than it was in 2010.

That has been a good thing for bondholders, with the subdued pace of new debt sales providing a tailwind for the market. While the pace of borrowing typically picks up in the last few months of the year, Bank of America Corp. analysts said Friday that it shouldn’t cause any trouble: investors will receive about $42 billion in interest and principal payments through the end of October, roughly enough to buy all the new bonds that will be sold.

To contact the reporter on this story: William Selway in Washington at wselway@bloomberg.net

To contact the editors responsible for this story: Elizabeth Campbell at ecampbell14@bloomberg.net, William Selway, Michael B. Marois

©2019 Bloomberg L.P.