Even $8.7 Trillion Bond Rollover Can’t Solve Safe-Asset Drought

Even $8.7 Trillion Bond Rollover Can’t Solve Safe-Asset Drought

(Bloomberg) -- The world’s biggest economies may roll over $8.7 trillion of debt maturing this year, but it won’t go far in sating almost bottomless demand for government bonds.

The value of bills, notes and bonds coming due for the Group of Seven nations plus key emerging markets is up 25% from five years ago and slightly higher than the $8.6 trillion last year, according to data compiled by Bloomberg.

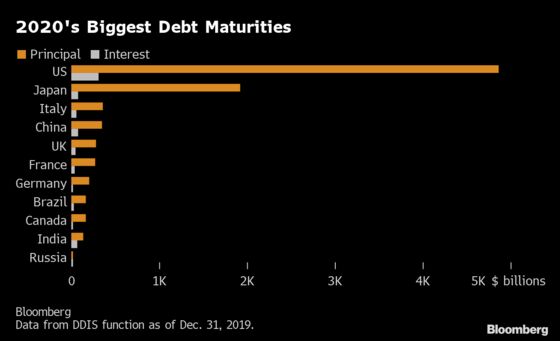

Refinancing needs look set to be dominated by the U.S., which has $4.87 trillion of debt coming due, followed by Japan with $1.92 trillion. China’s tab will drop to $351 billion from $632 billion.

On the other side, coupon payments and huge inflows into bond funds have made investors cash-rich, creating a positive technical backdrop for a debt party many on Wall Street see enduring.

In fact, despite the trillions in gross financing needs, investors face a bond drought, according to TD Securities and Oxford Economics.

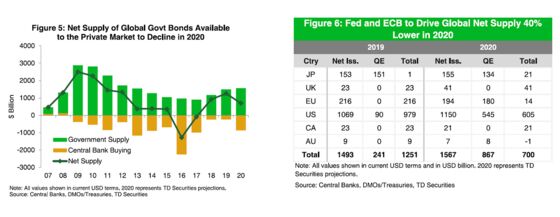

Purchases by the Federal Reserve and European Central Bank will drive global net supply of government bonds down 40%, according to TD strategists led by Priya Misra, leaving the net amount available to private market investors at the lowest levels since 2017.

It’s a shortfall Oxford Economics puts at about $400 billion annually over the next five years as demand outstrips supply. The firm expects central banks to buy at least $255 billion of safe assets a year, and in a severe downturn that figure could rise to $1 trillion.

The global bond markets surged to more than $115 trillion in mid-2019 from $87 trillion a decade ago, with government debt making up 47% of the total amount, according to data from the International Institute of Finance. Yet yields on sovereign debt have declined by 1.5 percentage points on average during that period, data compiled by Bloomberg show.

The U.S. shouldn’t struggle to find buyers to replace the maturing debt. In a world where more than $11 trillion of bonds globally have sub-zero yields, demand for Treasuries will persist.

Some 60 trillion yen ($552 billion) of Japanese government debt with a coupon of over 1% that matures within three years is likely to be reinvested in the U.S. where the whole yield curve is positive, Sumitomo Mitsui Trust Asset Management estimates.

Amundi, for one, is loading up on Treasuries.

“The global economy is stabilizing, but downside risk remains,” said Vincent Mortier, the deputy chief investment officer at the Paris-based firm. He reckons the yield on 10-year Treasuries will move in a 1.5%-1.7% range this year. “Quality bonds with positive yields will be in demand.”

--With assistance from Todd White.

To contact the reporter on this story: Anchalee Worrachate in London at aworrachate@bloomberg.net

To contact the editors responsible for this story: Sam Potter at spotter33@bloomberg.net, Cecile Gutscher, Sid Verma

©2020 Bloomberg L.P.