Evaporated, Collapsed: Strategists Dissect Stock Liquidity Woes

Evaporated, Collapsed: Strategists Dissect Stock Liquidity Woes

(Bloomberg) -- Bear markets can be stressful no matter what. But the speed of the slump, the whiplash of market swings and the strains of working from home have raised alarm about the faltering liquidity in even the biggest financial markets.

The Federal Reserve’s stimulus efforts on Sunday did little to calm the equities market and investors have continued to call for more help.

Here’s some strategist views on the ease of trading and the opportunities and risks therein:

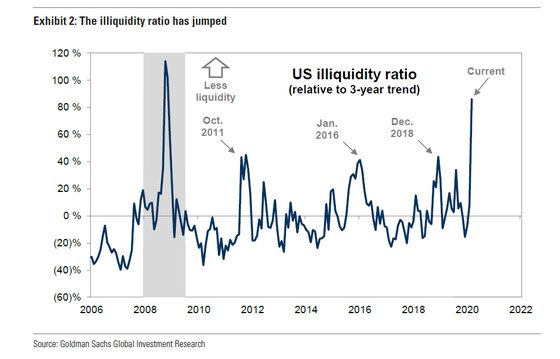

Risk and Opportunity

Ryan Hammond and David Kostin, Goldman Sachs Group Inc.:

“Our illiquidity ratio, which measures the price impact of trading volumes, shows that liquidity has evaporated within U.S. equities.”

“There’s a feedback loop among liquidity, volatility, and returns, as high volatility reinforces low liquidity and vice versa. Consistent with the current bear market, liquidity shocks are associated with a wider distribution of Russell 3000 returns, as weak liquidity can be present in both sell-offs and rallies.

“Some of the strongest S&P 500 returns have come during illiquid bear markets. We believe that thin liquidity, along with uncertainty and positioning, increase the risk that the S&P 500 overshoots its fundamentals in the near-term.”

“For longer-term investors, accepting liquidity risk presents an opportunity. A strategy of buying illiquid stocks and selling liquid stocks has generated a 4% annualized return since 1976, with a 63% annual hit rate of outperformance.”

Worse Than 2008

Bram Kaplan, Marko Kolanovic and Shawn Quigg at JPMorgan Chase & Co.:

“S&P 500 futures market depth plunged about 90% since the start of the COVID-19 panic to record lows.”

“The collapse in liquidity is much more pronounced than in 2008, due to the change in market microstructure we’ve discussed in past notes. For example, the worst month in 2008 (October) experienced a much smaller 60% drop in futures market depth from the prior average, and futures market depth was 7x higher in October 2008 than March 2020 month-to-date on average.”

Read more: Futures Liquidity Worse Than 2008 Crisis, JPM’s Kolanovic Says

ETF Resilience

Sebastien Lemaire and Laure Genet, Societe Generale SA ETF strategists:

“Based on the analysis of ETF traded volumes and redemptions between 24 February and 11 March, we show that ETF liquidity has suffered as for any other financial instrument, but that it has also demonstrated resilience. Only a fraction of the record volumes observed in the secondary market gave rise to redemptions, proof that ETF liquidity did not evaporate.”

Too Remote?

Tom Lee, co-founder of Fundstrat Global Advisors LLC:

“The VIX just posted an all-time closing high, at 83. This is higher than during the Great Financial Crisis (which had an intraday high). Was part of this due to the growth of remote working for financial employees? Many have posed this question and there are anecdotes that today was particularly disorderly. And under such circumstances, one would not be surprised to see the most ‘liquid’ assets being sold -- hence, the particularly brutal selling for equities.”

To contact the reporter on this story: Joanna Ossinger in Singapore at jossinger@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Ravil Shirodkar, Paul Dobson

©2020 Bloomberg L.P.