European CLO Debt Looks Too Good to Ignore in 2020

European CLO Debt Looks Too Good to Ignore in 2020

(Bloomberg) -- Europe’s CLOs are set to move into 2020 offering some of the most attractive spreads available in the corporate debt world.

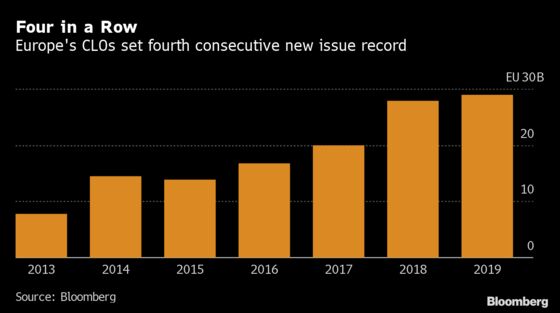

This year saw new managers flock into the asset class, contributing to just under 30 billion euros ($33 billion) of issuance and setting a fourth consecutive supply record.

“It’s been a strong year for the market with eight new CLO managers joining, triple-As tightening on strong demand and ESG gaining ground,” said Florent Chagnard, who is responsible for syndication and origination in the European CLO New Issue team at Credit Suisse Group AG.

Chagnard added that “all this creates opportunities that investors won’t be able to ignore and we are seeing more global investors coming online drawn to the strong relative value opportunity CLOs offer.”

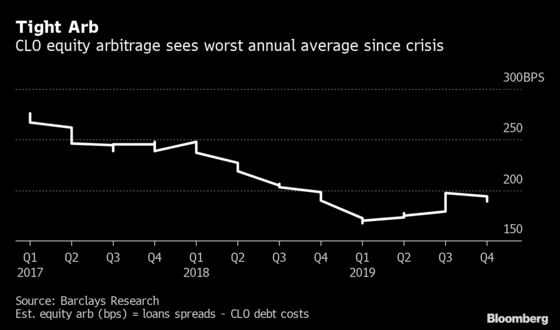

The robust supply seen in 2019 came despite ongoing comparisons with subprime and one of the toughest period of arbitrage dynamics in recent years. An off-kilter gap between the funds coming in from the loan collateral and the outgoing paid on the CLO bonds has this year compromised day one returns to equity investors, making the junior part of the CLO stack hard to sell.

This dynamic could weigh on issuance in the year ahead, with the most bearish analysts predicting supply to fall by 25%.

Spread Betting

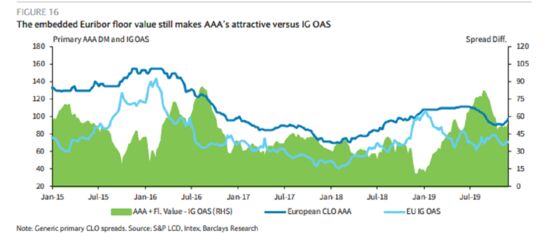

Helped by the value of the embedded Euribor floor and the European Central Bank’s monetary policy, top rated CLO spreads have this year provided an opportunity too good for institutional investors to ignore. That could drive compression next year.

“A lot of real money investors should be assessing CLOs, even if some end investors are nervous around the asset class,” said Jonathan Butler, head of European leveraged finance at PGIM Fixed Income.

“A German pension fund needing a 3% to 4% long term investment return, can not achieve that if invested in German Bunds that offer a negative yield,” Butler said, adding that such a fund “should be assessing the risk return value of CLO triple-As, which look ever so cheap compared with European corporate investment grade debt.”

Japanese demand remains the wild card, however. More investment from this region could help drive triple-A spreads lower. But even as anchor investor Norinchukin Bank stepped back in May, the gap was filled by European banks and U.S. investors buying with leverage, which sparked a 20 basis point rally in triple-A spreads.

Further down the CLO stack spreads widened during the second half of 2019 on growing credit stress in CLO portfolios, with the thin buyer base and contagion from the U.S. market pushing European spreads to three-year wides.

This heightened risk awareness caused investors to differentiate between managers based on strategy and performance, resulting in more pronounced price tiering among issuers.

Further idiosyncratic risk and downgrades are anticipated next year, but while rating companies such as Moody’s Investors Service expect a slight increase in defaults, credit enhancement will enable CLOs to continue to perform.

Europe CLOs to Perform Well in 2020 Despite Defaults: Moody’s

European CLO portfolios are also in better health compared to the U.S., and the return of buyers has helped junior mezz spreads retrace their widening into year end.

“The underlying fundamentals of CLOs continue to outperform the rest of credit markets mainly due to their robust structures and embedded subordination,” said Credit Suisse’s Chagnard.

The proliferation of ESG standards in the European CLO market could also cause eventual tiering in AAA pricing, notes Barclays CLO strategist Geoff Horton in a “Global Securitized Product Outlook” note.

Nine European managers have already incorporated ESG screening into their CLO strategies--NIBC Bank NV took this further by also scoring the underlying loans--and others should follow as investors seek out sustainable investments.

Whacky Arbitrage

Perfectly balanced arbitrage dynamics rarely exist, but as collateral spreads tightened and liabilities widened it has never been so difficult, according to one manager. That’s especially true for those selling 95% of the equity tranche leading to more fee sharing and creative structuring.

Captive equity vehicles handed a clear advantage to issuers including Ares Management, Apollo/Redding Ridge, Blackstone/GSO and CVC Credit Partners, which were the only managers to print three CLOs this year.

“Risk retention funds have become more and more important for the market and those managers with access to these or other equity solutions will find it easier to print deals,” said Nikunj Gupta, a director of new issue CLOs at Deutsche Bank AG. “There’s a difference between the fee rebate to third party investors and to risk retention funds.”

Rather than cut fees for another year some managers may pause before opening a new warehouse potentially slowing CLO creation in 2020. The availability of suitable loan assets is the other determinate, as lower loan spreads and poorer credit quality slow the time taken to ramp warehouses.

Still, this year has shown that it’s hard to stop the CLO printing machine, and with early indications for an uptick in M&A backed loan volumes next year, managers could get the supply they need to forge ahead. More new managers will boost the now 54 strong issuer base, and there are estimates of more than 50 warehouses open, some delayed from the final quarter of 2019.

Read More: Europe’s CLO Issuer Base More Than Triples In Past Six Years

“Things are likely to slow down, but CLO supply will continue to be driven by asset availability and if primary loan origination increases, then maybe the CLO market will rebalance and issuance will pick up,” said Deutsche Bank’s Gupta.

To contact the reporter on this story: Sarah Husband in London at shusband@bloomberg.net

To contact the editors responsible for this story: Vivianne Rodrigues at vrodrigues3@bloomberg.net, Hannah Benjamin

©2019 Bloomberg L.P.