Europe’s Stricter Green Bond Rules See First Use by Market

Europe’s Stricter Green Bond Standard Sees First Use by Market

(Bloomberg) -- The European Union’s “gold standard” rules for green bonds are starting to be used by the market, even before the bloc approved them.

Swedish property company Dios Fastigheter AB will present its new green financing framework to investors on Wednesday, which it says is aligned to the EU’s proposed green bond standard. Svenska Handelsbanken AB, which advised Dios, believes it is the first to adapt to the bloc’s regulations.

The bloc’s voluntary standard, published in July, requires issuers to abide by an array of rules if they wish to call their debt “European green bonds”. The EU’s parliament and member states have yet to sign off on it, with Budget Commissioner Johannes Hahn saying it won’t be ready for another year or two.

Dios’ green bond framework includes a “Factsheet” required by the EU standard, setting out its funding goals and environmental objectives. That still needs to be reviewed by an external party registered with the European Securities and Markets Authority, which Dios may seek later, though the mechanism for accreditation is not yet in place.

“They’re able to issue normal green debt today, but with a very strong option on those bonds to become European green bonds at some point in the future,” said Tobias Lindbergh, Handelsbanken’s sustainable finance head for debt capital markets. “There are major changes to the structure to make that possible and well over 100 changes throughout the entire framework.”

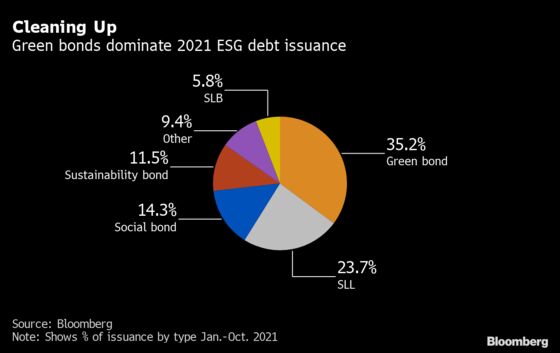

Global green bond sales have nearly doubled this year to $478 billion, with debuts in Europe from the likes of Italy, the U.K. and the EU itself, though borrowers have been using a cornucopia of national and voluntary market standards.

The most widely used, from the International Capital Market Association, only has a voluntary recommendation for reviews. The EU’s rules require mandatory impact reporting and an external review by an accredited verifier. The proceeds must also go to environmentally-friendly projects that are in line with its “taxonomy” for what counts as sustainable investment.

The European Central Bank published its opinion on the green debt rules this month, where it said the standard should become mandatory for newly issued green bonds within three to five years. The current proposal is voluntary, with issuers allowed to continue using existing industry guidelines for green debt.

The bond standard is part of a broader array of EU initiatives to help prevent greenwashing, with companies also needing to disclose how their activities align with the EU’s taxonomy in coming years.

Lindbergh said the clients he’s talking to about adopting the EU bond standard see it as an opportunity to start working on taxonomy-alignment in preparation for the company-level reporting. Some market participants also expect a pricing advantage for European green bonds.

“One year from now, I think if you ask an investor if they prefer a European green bond, a normal green bond or a plain vanilla bond, there will be a hierarchy where European green bonds come out on top,” he said. “Once mandatory disclosure on taxonomy-alignment begins, the market should begin to ramp up more quickly.”

©2021 Bloomberg L.P.