Europe’s Record Bond Program Bumps Up Against Green Concerns

Europe’s Record Bond Program Bumps Up Against Green Concerns

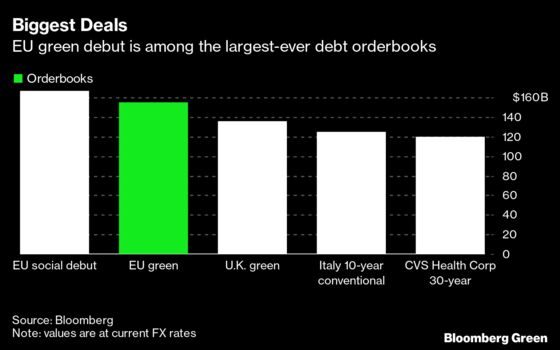

(Bloomberg) -- The European Union’s inaugural green bond sale wowed investors this week with its record size and massive order book. But it also raised some awkward questions about how the money will be used.

The EU’s green bond program isn’t yet covered by its own rule book for such debt. Instead, the bloc is applying a framework that governs a separate facility dedicated to Europe’s recovery from the pandemic. While that program also screens for environmental criteria, it’s not as strict as the EU’s green taxonomy, according to Sebastian Mack, a policy fellow at the Jacques Delors Centre, a Berlin-based think tank.

Europe launched its record 250 billion euro ($290 billion) green bond program this month. Proceeds from the sales are set to cover roughly a third of the bloc’s recovery package. But because the EU parliament and member states have yet to sign off on rules for green debt, investors aren’t covered by its protections. The European Commission says the bonds will adhere to its framework where feasible, but will be aligned with principles set by the International Capital Market Association.

Some investors who bought the bonds are now wondering whether their money risks going toward projects whose greenness is debatable.

“We do see a risk that activities are financed that have a relatively small environmental contribution,” said Jeroen Van Herwaarden, a fund manager at Triodos Investment Management BV, which participated in this week’s inaugural sale. “We would like to see reporting that provides an indication of the percentage of proceeds that has been allocated to EU taxonomy-aligned activities.”

The European Commission said its current framework draws “heavy inspiration” from the green bond standard proposal, using the taxonomy as a starting point for the assessment and screening of the categories. It “offers a gilt-edged guarantee to investors that their funds will be used for green investments, and commits to a full program of use of proceeds and impact reporting,” the commission said. The framework has “rigorous ex ante and ex post screening of projects to verify that the projects financed are truly climate relevant.”

| Read More... |

|---|

Hot Green Bond Market Seen Facing ‘Damper’ From Rules Next Year Record Demand for EU Green Debut Shows Supply Can Hardly Keep Up ECB Said to Study New Bond-Buying Plan for When Crisis Tool Ends |

After selling the bonds, the EU decides how to distribute the proceeds to member states. Countries need to submit payment requests as they reach environmental targets. Once they can show they’ve made progress, green-bond proceeds will be paid into national budgets, according to Sphia Salim, head of European interest rates strategy at Bank of America Global Research. Budget Commissioner Johannes Hahn said on Tuesday that another green bond sale this year would be unlikely, unless more payment requests are made.

What BNEF Says...

“Even if in its framework the EU mentions that introduced parts of its taxonomy into the rules that govern its green bond, the eligible projects follow another methodology which is only partially aligned with it. It feels like the EU created this gold standard classification but is struggling itself to implement it practically. However the fact that the Commission will report on the share of its green bond expenditures that are considered to be aligned with the EU Taxonomy should prevent greenwashing.”

--BloombergNEF associate Maia Godemer

The EU says it intends to use the money from the bonds to cover nine categories spanning everything from energy efficiency to climate-change adaptation as well as research and innovation activities supporting the green transition. Some targets “are formulated very broadly, leaving room for interpretation,” Van Herwaarden said. Not all countries’ recovery and resilience plans have been published yet, he noted, meaning there’s a chance projects won’t align with his fund’s requirements.

“We are very concerned that some projects may be deemed ‘green’ by governments while they are not according to the EU taxonomy,” said Sebastien Godinot, an economist at the WWF’s European policy office in Brussels. “There is a risk of greenwashing.”

Even so, the 15-year green bond sold this week meets Triodos’ definition of an impact instrument. The fund stayed away from the U.K.’s debut green gilt last month after deciding it wasn’t green enough. The EU’s focus on climate change mitigation and adaptation is encouraging, as is the transparency provided on the activities considered eligible in member states’ recovery plans, Van Herwaarden said.

The green bonds won’t be used to finance gas or nuclear energy projects, an EU official said by email. The commission is facing intense lobbying from those industries to be included in the taxonomy, while environmental groups insist they should be excluded.

Mack of the Delors Centre says the EU’s member states need to prove to investors that the bloc can maintain a high standard.

“It is now in the hands of the member states to keep the door to greenwashing closed,” said Mack. “If projects labeled as green do not deliver on climate protection, they must be sorted out and financed by conventional bonds.”

©2021 Bloomberg L.P.