Europe’s Funds Are Hunkering Down in Bonds for Coming Recession

Europe's Funds Are Hunkering Down in Bonds for Coming Recession

(Bloomberg) --

Woeful. BAD. Shocking. That’s how investors and strategists described Europe’s latest economic data, leaving them fearing the worst and betting this year’s record bond rally has further to run.

The prospect of an oncoming recession has some of the region’s biggest fund managers seeking safety by ratcheting up positions in Europe’s debt, including negative-yielding German securities. Yields look to be heading back down toward historic lows, despite the best efforts of the European Central Bank to stave off a contraction.

“Dipping in and out of recession could become the norm in Europe,” said Luke Hickmore, a money manager at Aberdeen Standard Investments, who has boosted the duration of his portfolios. “I think Germany is in a recession now but for the whole of Europe I would put the probability at close to 60% over 2020.”

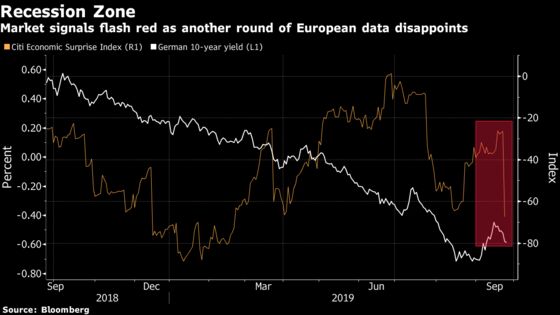

This year’s surge in European bonds stalled before the latest round of economic data this week. Now the rally is back on, as manufacturing in the region’s largest economy faces its worst slump since the financial crisis. That renews fears Europe is going the way of Japan -- a world of permanently low growth, inflation and bond yields.

The drop in the euro-area’s Purchasing Managers’ Index for services to an eight-month low of 52 in September was “a shocking set of numbers” for Robeco Institutional Asset Management’s Martin van Vliet. Any further fall to below 50, the dividing line between expansion and contraction, will be key to whether German yields slide even lower, according to Mediolanum SpA money manager Charles Diebel.

“The data is BAD,” Diebel said in a written response to questions, putting the chance of a recession in the euro area at 50% over the next 18 months. “We’re still looking for bull mode to be sustained in general.”

Further signs of weakening sentiment came Tuesday, with business expectations this month in Germany falling to the lowest in a decade. The mood among factory executives was the main reason, with the Ifo institute, which compiles the sentiment report, saying the only direction was “downward.”

Indeed, the Citi Economic Surprise Index, a gauge of whether economic data beats or falls short of analyst expectations, plunged to its lowest level since February this week, adding fuel to the market rally. ADM Investor Services global strategist Marc Ostwald described the latest manufacturing figures as “woeful.” Next in focus will be regional economic confidence data on Friday.

German 10-year yields dropped to -0.62% Wednesday, having touched an all-time low of -0.74% earlier this month. Those in Italian, Spanish and French debt have also fallen this week. Euro-denominated investment grade bonds have returned investors 8.5% this year.

New Lows

Amundi Asset Management, Europe’s biggest fund manager, thinks now is not the time to dip toes back into global bonds, as markets are pricing in too much monetary easing, according to Pascal Blanque, its group chief investment officer. It has cut exposure to long-dated U.S. Treasuries.

Still, while the jury is out on further Federal Reserve rate cuts, support for bond gains in Europe is set to come from the ECB’s fresh package of quantitative easing, starting in November at a pace of 20 billion euros ($22 billion) per month. ABN Amro Bank NV expects an increase in the pace of net asset purchases as well as another cut in its deposit rate.

The institution’s new tiering measure to ease the profit-squeeze on banks may allow it to cut rates deeper into negative territory in the future, despite some confusion in the short-term.

ECB President Mario Draghi has called on governments to help out to boost growth, though there are no imminent signs Germany will heed the call as it sticks to strict fiscal limits. Even the prospect of bigger budget spending is unlikely to turn the tide in rates, according to ING Groep NV, which recommended investors buy German debt.

“Economic weakness and a new round of stimulus suggest that long rates and government bond yields will see a new leg down and will eventually surpass previous record lows,” said ABN strategists Aline Schuiling and Nick Kounis.

To contact the reporter on this story: John Ainger in Brussels at jainger@bloomberg.net

To contact the editors responsible for this story: Paul Dobson at pdobson2@bloomberg.net, Neil Chatterjee, William Shaw

©2019 Bloomberg L.P.