One Question for the ECB: How Will It Tackle the Strong Euro?

One Question for the ECB: How Will It Tackle the Strong Euro?

(Bloomberg) -- Investors want to know how the European Central Bank is going to tackle the euro’s strength.

It’s been a guessing game since ECB Chief Economist Philip Lane said “the euro-dollar rate does matter,” hours after the common currency breached $1.20 for the first time in more than two years.

Money markets priced in a 10 basis-point cut in the main policy rate by next September, the euro tumbled and bonds advanced, all on the assumption that the central bank will eventually do more than just talk down the euro. A stronger currency makes it harder for the ECB to reach its inflation target.

“It seems highly likely that next week’s ECB meeting will have a dovish slant, partly in response to the strength of the euro,” wrote Jamie Searle, a rate strategist at Citigroup Inc. “A change in policy stance seems unlikely, however.”

The market moves were driven by expectations that the ECB may give guidance on whether it’s considering more stimulus, potentially weakening the currency. Curbing the euro would increase the competitiveness of European exports and raise inflation, which turned negative for the first time in four years, by making imports more expensive.

If the ECB President Christine Lagarde stresses the negative implications of currency strength, the market will price further rate cuts, according to UBS Group AG strategists including Rohan Khanna. Most economists forecast an increase in stimulus by December.

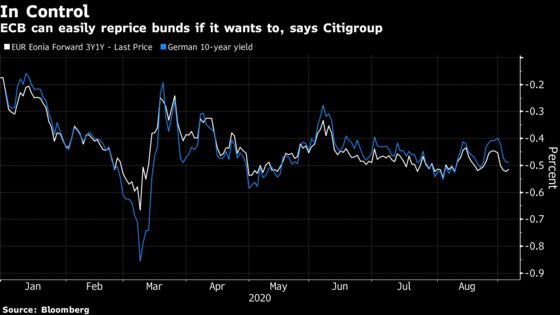

“The ECB may have problems with the euro -- and certainly with inflation -- but it already has a tight grip on euro rates,” said Searle, who sees the ECB increasing its bond-buying program by 500 billion euros in December. “The ECB can easily reprice bunds if it wants to” by cutting the main policy rate, he added.

That’s because Germany’s 10-year bond yield is closely aligned with a measure of where the policy rate is expected to be in future.

Debt Sales

The amount of bonds auctioned in the euro area may fall next week, with offerings from Germany, Italy, Netherlands, Austria, Portugal and Ireland totaling almost 20 billion euros ($24 billion), according to Citigroup. Danske Bank A/S flags that Italy and Spain may sell bonds through banks next week.

- Germany pays 12 billion euros of redemptions next week; there are no coupons payable

- The U.K. will offer a combined 5.25 billion pounds ($6.9 billion) of three- and 30-year debt. It will also sell a new 15-year note through banks; coupons and redemptions of almost 20 billion pounds will be paid

- The BOE will buy back 4.4 billion pounds of debt across three operations

- Data for the coming week in the euro area, Germany and U.K. is mostly relegated to second-tier, backward-looking figures; Germany will publish industrial production figures for July

- U.K. investors should be focused on Friday when July monthly GDP alongside industrial and manufacturing production figures as well as trade balance data will be published

- Lagarde speaks at the press conference following the monetary decision on Thursday and again later the same day at a Bundesbank event; Jens Weidmann, Francois Villeroy speak at the same event and chief economist Philip Lane participates in an online panel discussion on Friday

- There are no scheduled BOE policy maker speeches next week

- S&P Global Ratings reviews Portugal, Austria on Friday

©2020 Bloomberg L.P.