Euro, Bund Paths Depend on Draghi Ending the Great Rate Divide

Euro, Bund Paths Depend on Draghi Ending the Great Rate Divide

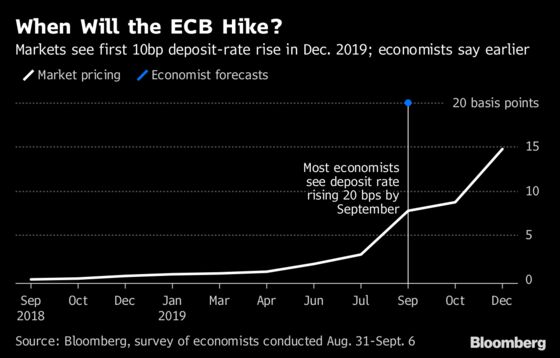

(Bloomberg) -- One particularly divisive debate in global markets -- how soon the European Central Bank will lift interest rates -- may be coming to a head.

Mario Draghi’s message Thursday could tilt the scales in favor of either investors, who are pricing a rate hike only toward end-2019, or analysts predicting an earlier move. And that should set the near-term course for the region’s bond markets led by German bunds, as well as the euro.

The monetary authority’s latest economic forecasts and Draghi’s confidence in pressing ahead with the plan to wind down asset purchases will help inform investors’ assessments on whether rate hikes could come any sooner. Predictions for growth starting from 2018 will be revised lower, officials familiar with the latest projections said, while those for inflation are largely unchanged.

The ECB committee that oversees the compilation of the forecasts also sees the risks to economic growth as tilted to the downside, according to the people.

While many analysts agree with the muted outlook, market pricing for a cumulative tightening of 20 basis points by March 2020 is “too little,” according to JPMorgan Chase & Co., which is going into the ECB decision with a short position in 30-year bunds.

Bank of America-Merrill Lynch says investors are underestimating the odds of a move as early as the middle of next year, while Credit Agricole SA sees any signal from Draghi on further policy normalization boosting the prospect of euro strength.

The ECB president needs to “sound confident enough in the resilience of the euro-area cycle, and on progress in core inflation by year-end, to avoid getting dragged into any awkward conversations on the wisdom of June’s QE announcements,” according to Bank of America Merrill Lynch strategists including Ruairi Hourihane. “While a hike in the middle of next year is not our baseline, we continue to believe the market is underpricing the possibility.”

Here is a selection of analysts’ market views ahead of the meeting:

Credit Agricole

- Balance of risks for EUR/USD is starting to shift in favor of further upside, according to Valentin Marinov, head of G-10 FX strategy

- ECB’s likely message of gradual policy normalization “could come across as rather constructive given the recent headwinds that have buffeted the euro-zone bond and stock markets”

- Some of these headwinds have started abating, as reflected by the tightening of Italian-German yield spreads and the less intense threat of a trade conflict between the EU and the U.S.

- “This much could add credibility to the ECB’s assessment and boost expectation of upcoming policy normalization”

Barclays

- Strategist Cagdas Aksu expects 30-year French bonds to perform better than 10-year debt in a scenario of rising or falling yields

- Market pricing of rate hikes is shallower than those foreseen by economists

- While pricing “looks very benign, most key ECB speakers have been consistently on the wires over the summer since the June meeting, saying that the market got ECB’s message correct”

- Bund yields to remain low unless core inflation picks up as “ECB’s very dovish short rate guidance in June caps the expectation component of German yields meaningfully”

BofAML

- Strategists expect near-term forecasts for euro-area economic growth and inflation to be lowered, medium-term confidence to be reiterated

- Any rates rally on the back of the ECB meeting would be “an opportunity to instigate tactical shorts in 5y Germany vs the U.S.;” investors will likely have to wait until at least October for any information on reinvestments

- “Very little” is priced in for interest-rate hikes and continue to favor Mar19-Jul19 Eonia steepeners, with the spread currently at around 2 basis points

JPMorgan

- Strategists including Fabio Bassi expect the ECB to hike its deposit rate (currently at minus 0.4 percent) by 15 basis points in September 2019 and 25 basis points in December, and then at a pace of 75 basis points per year

- If core inflation evolves at a slower pace than expected, the ECB may push back its December hike

- In either scenario, market pricing of “a cumulative 20 basis-point of hike at the March 2020 meeting is too little and we continue to keep paying Mar20 ECB OIS at -15 basis points”

- Market attention will be more skewed to the ECB staff forecasts for core inflation, as they are the best indicator to assess inflation forecast over the medium term, once the short-term effect of energy is stripped out

- Bank projects the ECB forecasts at 1.1% in 2018 (unchanged), 1.5% in 2019 (0.1% lower) and 1.9% in 2020 (unchanged)

- “Strategy-wise, we go into the ECB meeting with still a short duration on 30Y Germany, outright and conditional curve steepeners (reds/5Y and schatz/bund weighted, respectively) and paid greens in reds/greens/blues swap fly”

UBS

- “At the upcoming meeting, we do not expect any market moving headlines that could fundamentally alter the market’s assessment of the ECB’s rate path,” analysts write, adding that “ECB’s gradualism is deeply entrenched in market pricing of rate hikes”

- Improvement of underlying inflation dynamics alongside a stabilization in sentiment data will be “driving factors for the market to alter its currently subdued assessment of the ECB’s deposit rate path” yet bar for upside surprises to economic data is low

- Favor outright hedged EONIA steepeners (2y1y vs 4y1y); see potential for gradually higher yields further out the curve and recommend 1y fwd 5s30s EUR steepeners

--With assistance from Stephen Spratt and James Hirai.

To contact the reporter on this story: Carolynn Look in London at clook4@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Anil Varma, Keith Jenkins

©2018 Bloomberg L.P.