End-of-Cycle Fears Loom Over High-Yield Market After Bumpy 2018

End-of-Cycle Fears Loom Over High-Yield Market After Bumpy 2018

(Bloomberg) -- High-yield bankers and investors alike will be relieved to close the door on 2018 after returns in Europe swung into the red and a choosier buyer-base resulted in at least 18 new deals being pulled or postponed.

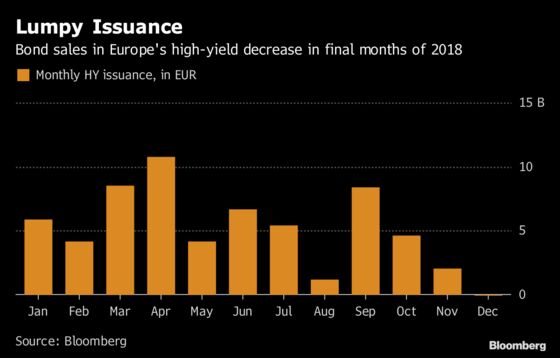

With the European market suffering bouts of volatility for much of 2018, speculative-grade issuance came in some 36 percent down on last year’s record tally of 96.2 billion euros-equivalent ($108 billion), according to data compiled by Bloomberg.

But any comfort may prove short lived as talk of a downturn in the credit cycle gathers pace, potentially damping prospects for issuance over the next 12 months and exacerbating secondary market price moves.

“Putting aside specific things like Brexit, the market will pay particular attention to any bad earnings results from specific companies or sectors and whether that translates into a broader macro downturn,” said Jane Bradshaw, head of high-yield capital markets at Morgan Stanley in London.

Flat Issuance

Next year’s overall supply forecast is broadly in line with volumes seen so far this year, Morgan Stanley strategist Srikanth Sankaran wrote in a Nov. 27 research note. High-yield bond sales have totaled 62.0 billion euros-equivalent year to date, Bloomberg data show.

Issuance in 2019 will be more reliant on M&A activity, according to Kevin Foley, JPMorgan’s EMEA head of loan and high-yield capital markets. But as deal making activity typically suffers when equity markets are volatile, supply volumes could remain at the mercy of wider sentiment.

That volatility could restrict future windows for bond sales as it did in 2018, when there were 12 weeks of zero issuance. Foley is however expecting “busy periods similar to this year where there hasn’t always been strong visibility on the pipeline, but windows have emerged for robust supply.”

Price Pain

This month euro-denominated borrowing costs surpassed 5 percent for the first time since March 2016. This higher price point, combined with an expectation for continued volatility, could hamper prospects for opportunistic refinancing next year.

“The market has priced materially wider and you can’t ignore that when you’re coming to the market with new deals,” Morgan Stanley’s Bradshaw said.

Without a real need for financing, the expectation is that any opportunistic borrowers will remain sidelined, according to Evangeline Lim, a London-based portfolio manager at PineBridge Investments.

“Unless you’re a high-quality issuer with a proven track record you’re going to wait for the right window to launch a new deal,” Lim said.

Besides higher pricing, many refinancings for issuers rated single B were executed in 2017, meaning there isn’t “a single-B maturity wall” to be addressed next year, according to Bradshaw.

| Fundamental Picture |

|---|

| Leverage: Moody’s doesn’t expect average leverage for new deals to increase much further next year. “We are already at record highs and close to the ECB guidelines limit of 6x,” Richard Etheridge said |

| Defaults: Rates for European high-yield bonds and loans will stay low at less than 2%, Fitch Ratings says in report |

| Liquidity: “Speculative-grade liquidity to get worse in 2019” given a more muted economic outlook, Moody’s says in a note; however, moves will be gradual |

| Economy: The ECB is forecasting y/y GDP growth for the eurozone of 1.9% in 2018, moderating to 1.7% in each of 2019 and 2020 |

Fund Outflows

The downbeat sentiment in Europe’s high-yield market saw many investors vote with their feet this year. Junk bond funds denominated in euros have seen $12.0 billion of redemptions so far in 2018, Wells Fargo Securities analysts wrote in a Dec. 13 client note, citing EPFR Global data.

The trend of outflows has been cited as one of the driving factors behind the underperformance of the asset class this year. The Bloomberg Barclays Pan-European HY (ex Fin) Total Return Index has delivered negative returns of 3.28 percent year to date versus 5.5 percent of positive returns in 2017.

“Outflows not only from core high-yield investors but also investment-grade accounts have driven weak technicals,” said Jens Vanbrabant, head of European loans and high yield at Wells Fargo Asset Management.

“The market is combating an end of cycle sentiment with asset allocators continuing to prefer floating rate product such as private debt or syndicated loans,” Vanbrabant said.

Single Name Blowups

Traders next year will likely have to contend with continued swings in single-name bond prices, fueled by earnings disappointments and ongoing sector risks such as those from the construction or retail industries. Over 70 bonds were last month marked at distressed or stressed levels, compared with 32 in 2017, according to data compiled by Bloomberg.

While a poor earnings season may have amplified the debate about where European high yield is placed in the credit cycle, the associated volatility is nevertheless providing an opportunity for some.

“At the margin there’s been an opportunity to rotate out of positions that have held up very well into names that have sold off and now represent better value,” said Thomas Ross, a portfolio manager at Janus Henderson Investors, who manages $2.8 billion of assets.

The market has moved on a stage in the past three to four weeks, Ross said, “with names that we do still consider as decent investments now falling in price too.”

To contact the reporters on this story: Marianna Aragao in London at mduartedeara@bloomberg.net;Laura Benitez in London at lbenitez1@bloomberg.net

To contact the editors responsible for this story: Sarah Husband at shusband@bloomberg.net, Charles Daly

©2018 Bloomberg L.P.