Elite Colleges Join Bond-Market Boom by Seizing on Low Rates

Elite Colleges Join Bond-Market Boom by Seizing on Low Rates

(Bloomberg) -- America’s elite colleges are joining the corporate-debt boom.

Even with the pandemic sowing uncertainty about the coming academic year, some of the richest universities are seizing on a chance to borrow at low interest rates. Investors have plowed into highly rated corporate debt since the Federal Reserve pledged to intervene to keep credit flowing, setting off a rally amid confidence the market will weather the steep economic contraction.

Colleges have sold about $8 billion of bonds since mid-March, a steep increase from a year earlier, according to data compiled by Bloomberg. That has included highly competitive schools such as Brown, Cornell, Duke, St. Louis’s Washington and Harvard universities, all of which are seen as better able to contend with the pandemic’s fallout than smaller colleges without such large endowments or cache.

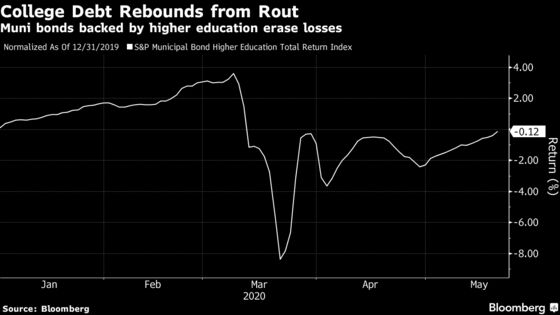

About half of borrowing has been done through the sale of corporate debt, which doesn’t have the municipal-bond market’s restrictions on how the funds can be spent.

“Taxable corporate bonds are appealing as they are experiencing historically low interest rates and the taxable bond market has had less volatility over the last month compared with the tax-exempt market,” said Matt Greaves, the assistant vice president for treasury and finance at Emory University in Atlanta.

The borrowing spree comes as the pandemic casts uncertainty over whether and how universities will resume classes in the fall. That’s expected to increase the financial pressure on some private colleges that were already struggling with enrollment declines as debt-wary students seek less costly alternatives.

Yet even top-flight schools with large endowments and no trouble attracting students haven’t been entirely unscathed. Harvard, the country’s richest college, is forecasting a revenue shortfall of nearly $1.2 billion over two academic years. Northwestern was recently downgraded and is tapping its endowment and furloughing about 250 staff members. Cornell announced a hiring freeze and cut salaries for university leadership.

Even so, Patrick Luby, a municipal-bond strategist at CreditSights Inc., said it’s an “opportune time” for universities to raise money, especially in the taxable debt market where they pose far less risk than companies whose businesses are being battered by the slump.

The Massachusetts Institute of Technology moved up to late April a $350 million debt sale for campus projects that wasn’t slated to occur until as late as 2025, said Glen Shor, its vice president for finance. It paid yields of 2.29% on securities due in 2051.

“Favorable conditions for borrowing drove the Institute to accelerate its timeline,” he said.

Colleges are one of the few types of borrowers that consistently swap between selling debt through the tax-exempt muni market and taxable corporate bond market. The taxable market is usually a quicker, though more expensive, avenue to sell bonds and doesn’t carry the additional federal regulations that come with tax-exempt bonds.

The municipal market was roiled in March by concern about how badly the coronavirus will hammer the finances of governments and others, like hospitals or nursing homes, that have issued bonds. Though it has recovered, the gap has narrowed between the yields on top-rated municipal bonds and corporate debt, according to Bank of America Corp. analysts. That means the premium colleges have to pay to sell taxable is small.

Colleges and universities can also draw from a bigger buyer base when tapping the corporate market, said Nisha Patel, a portfolio manager at Parametric Portfolio Associates.

Corporations have sold more than a $1 trillion of debt so far this year, far more than the $136 billion of long-term municipal bonds that have been issued. Moreover, the tax-exempt debt market is dominated by individual investors who tend to yank out their cash when they see losses pile up.

“Muni investors can be a little skittish about certain sectors,” Patel said. “Corporate buyers will be fine with higher rated institutions relative to the amount of risk in the corporate-bond market.”

©2020 Bloomberg L.P.