An Economic Winter Grips the Euro

An Economic Winter Grips the Euro

(Bloomberg) -- Just three weeks into 2019, analysts’ conviction this will be the year of the euro -- and higher bund yields -- is being tested.

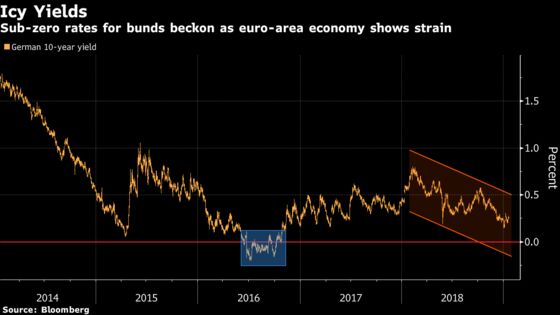

The common currency has declined against each one of its Group-of-10 peers outside Europe as slowing euro-area growth, stalling inflation and lingering political risks hold investors back. Benchmark bund yields, meanwhile, are trapped near the lowest level in two years, setting the stage for “deeply negative” rates within six months, says Citigroup Inc. NatWest Markets contends the recent slide in Japanese yields into negative territory is a precursor for where bunds are headed.

A host of banks had projected that the euro would surge this year, riding on the coattails of higher German yields, on conviction the Federal Reserve would pause its rate increases and the European Central Bank would raise borrowing costs for the first time in eight years. Yet, German factory orders and industrial output have shrunk far more than forecast, data released since the start of the year showed, spurring analysts to peg back their outlook. The skepticism is being reflected in money markets, where investors see the ECB shunning a rate increase altogether this year.

The outlook is so dire that German money manager Wirtgen Invest sees bund yields potentially turning negative before the end of this quarter, with a global recession expected in 2019.

“The likelihood of negative bund yields in the first quarter is high and may even happen relatively fast,” Jörg Rahn, Wirtgen’s Chief Investment Officer, said in an interview. “The current developments are bitter.”

Ten-year bund yields were at 0.25 percent Tuesday, having touched 0.15 percent early this month, the lowest since November 2016. They first went below zero percent in June of that year. Ten-year U.S. and Japanese yields have also touched their lowest levels in around a year. The euro has lost 0.9 percent against the dollar in January to about $1.1360, after sliding 4.5 percent last year.

While the ECB has said it sees rates remaining at record lows “at least through the summer” of this year, current money-market pricing implies investors expect any increase only in the second quarter of 2020. At the central bank’s December meeting, President Mario Draghi had acknowledged that incoming data were “weaker than expected” and that “this may suggest lower growth momentum ahead.” He may reiterate the message this week.

The euro-area economy expanded at an annual pace of 1.6 percent in the third quarter of 2018, the slowest since 2014, according to the most recent data. The economic gloom will weigh on Europe’s shared currency, according to Societe Generale SA.

Short Euro

“If the U.S. economy wasn’t slowing, the euro would already be the other side of $1.10,” wrote Kit Juckes, a strategist at Societe Generale. “We have a bias to be short euros against a trio of other currencies,” referring to the pound, yen and Australian dollar.

Not everyone is convinced though, with other regions also showing signs of economic strain. Goldman Sachs Group Inc. sees the euro rallying to $1.17 over the next three months, with Europe and the U.S. currently engaged in a “race to the bottom,” with the latter currently leading.

“We expect some tactical euro-dollar upside, even though euro-area growth has serially underperformed and the risks to our ECB tightening forecast are skewed toward later and less,” strategist Michael Cahill wrote in a note to clients. “While the euro area has been slowing for the past year, U.S. activity levels are now slowing faster, from a higher level, and in a more reactive setting for policy makers.”

For Citigroup, the recent euro-area slowdown suggests scope for a drop in the manufacturing gauge to 48 in the next four to five months, below the 50 mark that separates growth from contraction. And if that that were to correspond with a slump in inflation to levels last seen in 2016, investors would once again be facing yields of zero percent or lower, according to the bank.

German bonds are among the most widely traded fixed-income assets and have a reputation for being some of the safest money can buy. They have therefore benefited from the escalating trade tensions between the U.S. and China, Italy’s political fragility and the clock ticking down to Brexit without a deal being signed -- all on top of disappointing economic data out of the euro area.

“The euro area and Japan are now in the same space,” NatWest strategists Andrew Roberts and Jim McCormick wrote in a note to clients. “The path of least resistance is lower yields.”

--With assistance from Liz Capo McCormick.

To contact the reporters on this story: John Ainger in London at jainger@bloomberg.net;Dirk Gojny in Frankfurt at dgojny2@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Anil Varma, Neil Chatterjee

©2019 Bloomberg L.P.