Wall Street Shows Risk Appetite With Small-Cap Profits Near Zero

Earnings Nearly Went to Zero for Small Caps in First Quarter

(Bloomberg) -- For one of the starker examples of how much recovery-obsessed investors are willing to stomach lately, compare this week’s surge in small caps with first-quarter results the companies just finished reporting.

Weighted to service-oriented companies particularly hard hit by stay-at-home orders, the Russell 2000 saw per-share profits fall 90% from a year ago, several times more than members of the S&P 500, according to Goldman Sachs data. Meantime, before a hiccup on Thursday, the Russell 2000 Index had risen on eight of nine days in a rally exceeding 16%.

“With small company stocks, because they carry significant debt and are more fragile businesses as a group, they face a more existential threat. That’s the same reason they tend to lead the way out of most recessions,” said Peter Mallouk, president and chief executive officer of Creative Planning. It’s not just that their earnings outlook improves, but the “existential risk of complete failure gets taken off the table,” he said.

The divergence shows what a powerful force hope has been in guiding investors lately. It’s also a laboratory for observing the impact of Federal Reserve actions in equities. Strength in small caps is by definition strength in companies with the weakest credit profiles, and their fortunes turned almost simultaneously with Jerome Powell’s campaign to shore up bond and lending markets.

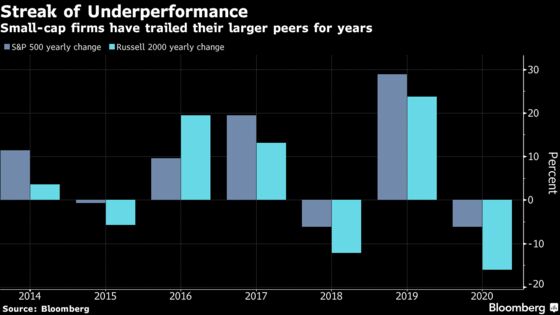

Investors have shown themselves willing to pivot away from lockdown winners including tech and health care and move into shakier corners of the market. But the damage to earnings for smaller companies in the quarter just passed was deep and those stocks are still playing catch-up. Down about 16% this year, the Russell 2000 has lagged behind the S&P 500 by about 10 percentage points. That’s the most on record this far into the year.

Goldman’s data is based on the total of how much each Russell 2000 company made in the first quarter and compared it with results from a year ago, showing EPS of $32.53 last year versus $3.23 this year.

Rather than looking at per-share results, Vincent Deluard, global macro strategist at INTL FCStone, plotted the total amount of money made by each company that has released results. Based on a 90% reporting rate, the index’s components posted a loss of about $37 billion in the first quarter, his model showed.

The group was already on weak footing coming into the crisis. More than a third of U.S. small caps had losses before the outbreak, while 40% don’t have sufficient cash to cover two months of operating expenses, according to a recent report from Deluard.

“In such desperate times, only balance sheet strength, and especially cash positions, matter,” he said.

Looking ahead, about 47% of Russell 2000 companies are projected to report a loss in the second quarter. That compares with 16% for large ones, according to data compiled by Bloomberg. And at 1 times sales, the Russell 2000 is trading near a multiple that’s one quarter of what investors are willing to pay for stocks in the Nasdaq 100. That’s the biggest discount since the dot-com era, data compiled by Bloomberg show.

Some researchers, however, see potential for small-cap outperformance once a recovery begins, signs of which were prevalent this week. Coming out of recessions, small caps have beaten large nine out of the last 10 times and also tend to beat coming out of bear markets, according to Jefferies’s Steven DeSanctis and Eric Lockenvitz.

“You’ve seen both value and small-caps do better because of the anticipation of a better economic cycle in the upcoming year,” said Wayne Wicker, chief investment officer of Vantagepoint Investment Advisers. “With that hope by investors, I think you’ve seen a shift to those more pro-cyclical plays.”

To Barry James, portfolio manager at James Investment Research, the trend also makes sense. Investors already took advantage of the run-up in tech firms -- now, they’re looking for new deals.

“We view the market as a battlefield and the generals have been leading and now maybe the privates are coming into battle,” he said. “Folks realize that is where the opportunities are.”

©2020 Bloomberg L.P.