Draghi’s Bond-Market Heroics Face Risk of Lagarde Reality Check

Draghi Dream Trade for Bond Bulls Faces Lagarde Wake-Up Call

(Bloomberg) -- Explore what’s moving the global economy in the new season of the Stephanomics podcast. Subscribe via Pocket Cast or iTunes.

European Central Bank President Mario Draghi has been the bond market’s best friend and investors aren’t expecting the same support from his successor Christine Lagarde.

Since Draghi took the helm of the ECB eight years ago, Europe’s sovereign bonds have surged, with German debt returning 27% and that of Ireland almost 90%, Bloomberg Barclays indexes show. It’s been a dream trade. Draghi cut rates two days after his tenure began and went on to live up to his famous pledge in 2012 to do “whatever it takes” to hold the euro area together. He oversaw trillions in bond buying, the introduction of negative rates and measures to support banks.

Thursday’s gathering of the Governing Council will be Draghi’s last before his time as president ends on Oct. 31. Lagarde arrives just as monetary policy appears to be reaching its limits. The former head of the International Monetary Fund has praised the ECB’s stimulus, but may ask governments for fiscal support to help to energize the euro-area economy. While sweeping increases in public spending are doubtful, the prospect of greater supply that any such measures would bring could threaten the record-breaking rally for the region’s bonds.

“ECB monetary policy is probably reaching the point of diminishing effects,” said Tracy Chen, portfolio manager and head of structured credit at Brandywine Global Investment Management LLC, which oversees $75 billion in assets. “Lagarde prefers the use of fiscal policy more than Draghi did. There is room for a further sell-off in sovereign debt.”

The impact of Draghi’s expansive monetary policy has left an enduring mark on German government bonds, the region’s benchmark securities. The rate on 10-year bunds was around 2% when Draghi took up his role at the ECB, and tumbled to an unprecedented minus 0.74% this year -- as Germany’s entire yield curve turned negative. Italy’s bonds show an even more impressive trajectory, falling from almost 7.5% in 2011 to 0.75% this year. And so Lagarde takes the helm with bond yields near all-time lows, making it hard for any central banker to push them down further.

For euro-area government debt in aggregate, returns under Draghi were about 50%, according to a Bloomberg Barclays index. That compares with gains of 36% during the eight-year term of his predecessor Jean-Claude Trichet.

Regime Change

In the build-up to this week’s rates decision, optimism that the U.S. and China may reach an initial trade deal and diminishing risks of a hard Brexit have helped lift government debt yields globally. Germany’s 10-year rate has risen to minus 0.41%. U.S. benchmark 10-year note yields hover at about 1.74%, up from lows last month of 1.43%.

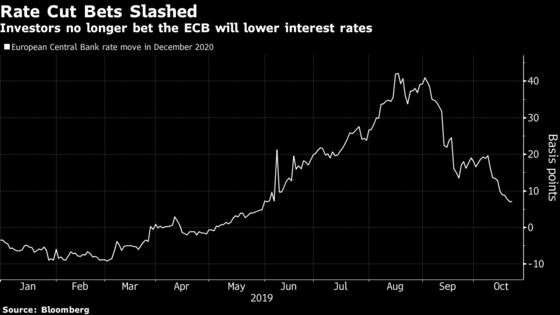

At the ECB’s September gathering the central bank announced the restart of asset purchases, cut its deposit rate to minus 0.5% and eased the terms of its program of long-term bank loans. But the decision also sparked a revolt on the Governing Council, with the resumption of bond purchases seen as excessive by some policy makers. After last month’s fresh dose of ECB monetary easing, strategists expect no further policy changes this week. Futures aren’t pricing in any further ECB rate cuts in the foreseeable future either.

“There might be a degree of reluctance to price further easing, even in light of increasing economic gloom, given the increasing awareness that monetary policy has reached the limits of what it can do and would like to pass on the baton to fiscal policies,” Antoine Bouvet, a senior rates strategist at ING Bank NV, wrote in a note.

Still, large-scale fiscal stimulus from Germany is a remote possibility, even as officials in Chancellor Angela Merkel’s government have some options in the pipeline. Finance Minister Olaf Scholz has argued that the government is ready to act in the event of an economic crisis -- which it doesn’t see as an imminent risk.

Draghi doesn’t get all the credit for the record-breaking rally in euro-area bonds. U.S. Treasury debt has gained about 18% during in the past eight years. Investors’ persistent search for safety has also been a reason for a fall in yields, with rates on around $13 trillion in global debt turning negative.

That has helped the longest-maturity government bonds lead the advance this year. In the Draghi era’s world of ultra-low rates, they offer the highest returns for a safe asset, standing out to yield-hungry investors. And with little inflation to eat into returns and the global economy growing weaker by the day, yield curves have been flattening. That is a sign that the region’s economy could struggle to expand over the long term, leaving it stuck with low interest rates and a lack of inflation, a trend known as Japanification, named for the country that is most associated with the trap.

Unlike the ECB, the Federal Reserve is seen having plenty of monetary policy firepower remaining -- with a third interest-rate cut this year likely when policy makers gather next week. In this context, U.S. Treasuries have outperformed their German counterparts this year.

According to forecasts from Goldman Sachs Group Inc., 10-year German bund yields will by the end of next year have risen to minus 0.2%, The firm’s strategists expect the yield gap in Treasuries over bunds to keep narrowing, given the Fed’s greater bandwidth to ease.

“With Mario Draghi, you really had the feeling at one point that he was master of the universe,” said Markus Allenspach, head of fixed-income research and a member of the investment committee at Zurich-based Julius Baer. “Central bank officials are now kind of moving to the second row, seeing their job as to not kill the expansion but that they alone cannot stimulate the economy. Lagarde enters the field now, with a lot of new ideas.”

To contact the reporters on this story: Liz Capo McCormick in london at emccormick7@bloomberg.net;James Hirai in London at jhirai3@bloomberg.net

To contact the editor responsible for this story: Paul Dobson at pdobson2@bloomberg.net

©2019 Bloomberg L.P.