The Carry Trade Is Heating Up as Fed and ECB Get More Dovish

The Carry Trade Is Heating Up as Fed and ECB Get More Dovish

(Bloomberg) -- As dovish central banks stoke negative yields throughout developed nations, it’s become more tempting for yield-hungry investors to borrow U.S. dollars and euros to buy riskier emerging-market currencies.

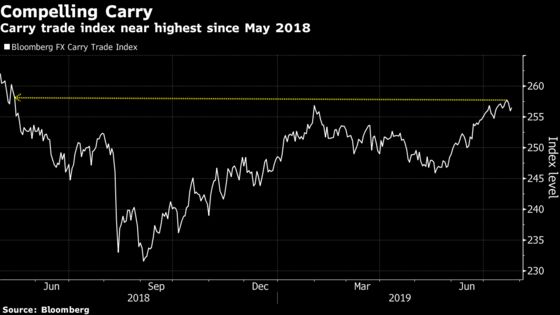

Purchasing such assets with dollars is generating the best returns since May 2018, according to a Bloomberg index that tracks so-called carry-trade returns from eight developing markets funded by greenback short positions. One example of what’s been working: Argentine peso bets using dollars are reaping about a 15% gain this year, and this jumps to 20% with euros.

Expect investors to keep scouring this space. JPMorgan Chase & Co. says central-bank easing in the U.S. and Europe may prompt investors to do even more of these trades. BlueBay Asset Management recommends fueling Mexican peso, Brazilian real and Russian ruble transactions with the U.S. currency. The trend is being stoked by traders irked by the negative yields on $13 trillion of debt, which is pushing them into sometimes-fickle emerging markets in their quest for yield.

“It is an environment which is beneficial for EM credit, carry and spread product,” said David Riley, the chief investment strategist at BlueBay, which oversees $60 billion in fixed-income investments. Demand for carry trades “reflects the fact you’ve got a dovish Fed and the dollar upside is capped.”

In a carry trade, speculators borrow in a currency they expect to depreciate or remain little changed to obtain the lowest borrowing costs. They profit from the yield differentials or appreciation in emerging-market currencies. The trades are usually helped by low volatility.

Clear Signals

Traders anticipate the European Central Bank will take a more dovish stance this Thursday, something that’s likely to worsen yield prospects in Europe. Federal Reserve policy makers are expected to cut interest rates by at least 25 basis points when they meet next week, another boon to carry trades.

The ECB “signaling is pretty clear that they’re going to ease policy,” said Jens Nystedt, a senior portfolio manager at Emso Asset Management Ltd., which has $6 billion in assets under management. “If these central banks deliver on expectations, it’ll keep the demand of carry trades intact.”

Still, risks abound.

JPMorgan says that even though FX carry baskets tend to deliver positive returns in the late stages of an expansion, returns have mostly been negative whenever emerging-market growth falls substantially. On Tuesday, the International Monetary Fund further reduced its global growth outlook. Chase Muller, who oversees $600 million in assets as a money manager at One River Asset Management LLC, said there are challenges in jumping on the carry bandwagon in countries with deteriorating fundamentals.

Musical Chairs

“It’s kind of like you’re playing musical chairs,” Muller said. “How long are you going to keep dancing while the music’s playing? When it stops, it can be pretty painful. But there are still some emerging markets that look pretty good.”

A Bloomberg Intelligence study suggests Brazil, Mexico, Russia and the Philippines offer opportunities for yield hunters because of higher returns and some of the best expected growth rates through 2020.

Read More: Party in Emerging Bonds Is Set to Last So Long as Yield Is King

Goldman Sachs Group Inc. strategists also encouraged caution Wednesday. “For most EM carry trades, an under-delivery from either central bank, or both, would indeed be a risk: rising core yields are historically associated with underperformance of EM FX carry strategies,” Kamakshya Trivedi and others wrote in a note emailed to clients Wednesday.

Goldman recommends investors short the euro against the Mexican peso, noting, however, that the trade could underperform on a hawkish Fed or ECB surprise. If either central bank underdelivers, some Asian high-yielders are more likely to be resilient than other currencies, the strategists wrote.

For now, the approach is working. An investor using dollars to fund Russian rubles and Mexican pesos has gained about 14% and 6.3%, respectively, this year, according to Bloomberg data. A trader going long Brazil’s real and the Philippine peso is up 4.8% and 4.3%, respectively.

“The developed-market central banks are moving towards a dovish pivot,” said Marvin Loh, global macro strategist at State Street Global Markets. “Clearly it’s driving a reach for yield.”

To contact the reporters on this story: Susanne Barton in New York at swalker33@bloomberg.net;Sydney Maki in New York at smaki8@bloomberg.net;Selcuk Gokoluk in London at sgokoluk@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Nick Baker, Mark Tannenbaum

©2019 Bloomberg L.P.