Don’t Fear the Bond Doomsday Everybody Sees Coming

Don’t Fear the Bond Doomsday Everybody Sees Coming

(Bloomberg Opinion) -- It seems as if you can’t go anywhere on Wall Street these days without finding someone calling for Armageddon in the U.S. corporate bond market.

Bank of America Corp. strategists wrote a report titled “perfect storm for credit,” while those at Legal & General Investment Management America, with $100 billion in fixed-income assets, say that 2018 — the worst year for corporate debt in a decade — is just the start of its decline. Scott Minerd, global chief investment officer at Guggenheim Partners, made headlines this week by declaring that “the slide and collapse in investment grade credit has begun,” with the sell-off in General Electric Co. just the tip of the iceberg. As my Bloomberg Opinion colleague Robert Burgess noted, other big names in the financial markets have voiced similar concerns, including Marc Lasry of Avenue Capital and Howard Marks of Oaktree Capital.

Markets got the message, with U.S. investment-grade credit spreads widening on Tuesday by the most in nine months. But before you go ahead and sell every corporate bond you own, take a step back and ask: How often is such a large group of investors and strategists correct in divining the path ahead for asset prices? Yes, the corporate-bond market has had a terrible year, but things don’t always move in one direction. One example is Minerd’s view on the direction of Treasury yields in June 2016, as they hurtled toward an unprecedented low. I wrote that he saw 10-year yields hitting 1 percent by the end of that year — and he wasn’t alone in that view. Of course, that didn’t happen.

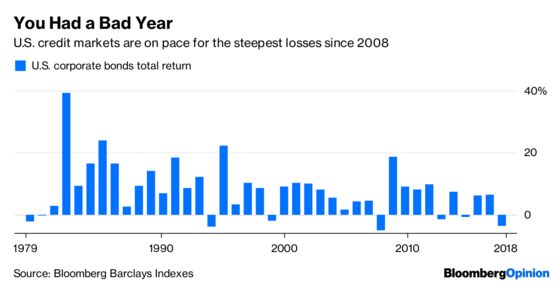

In fact, history suggests that much of the pain may already be over. The Bloomberg Barclays U.S. Corporate Bond Index is down 3.5 percent in 2018, on pace for its third-worst year since 1975. The last time it fell in back-to-back years was in 1979 and 1980. In 2008, when spreads blew out to five times as wide as they are now, the loss was about 5 percent.

Effectively, the main reason corporate bonds are having such a forgettable year is because 10-year U.S. Treasury yields have climbed almost 75 basis points since Jan. 1, rising from what was still an extraordinarily low level. That sort of upward momentum probably won’t last. The median forecast in a Bloomberg survey expects yields to rise only 38 basis points from where they are now by the end of 2019 and then plateau in 2020. If interest rates are still increasing, that most likely means the economy remains strong, which suggests little reason for downgrades and defaults.

Of course, it’s not easy to be level-headed and step in with confidence in the midst of a sell-off. “It just feels like a much more risky proposition than it did a year ago,” Jason Shoup, head of global credit strategy at Legal & General, told Bloomberg News’s Jeremy Hill. There’s no denying that it stings when corporate debt delivers the worst loss in a decade. And it’s unnerving to finally see the Federal Reserve stepping back from its post-crisis stimulus measures. Bond investing isn’t as simple anymore as finding something with a decent yield spread and watching it deliver outsized returns.

That doesn’t necessarily portend a doomsday, though — especially not when it seems as if all of Wall Street is anticipating it. In June, I wrote about the fear that BBB rated borrowers were at a tipping point. Returns have barely budged in the ensuing months. A month ago, Bloomberg News’s Molly Smith and Christopher Cannon wrote a definitive article about companies that have almost $1 trillion of debt and are rated investment grade but have characteristics of high-yield issuers. At this point, investors have lost their right to claim they were blindsided from any of them becoming “fallen angels.”

It’s tempting to look at the decline of GE, which was booted out of the Dow Jones Industrial Average in June after more than a century, as a sign that a change is afoot in U.S. credit markets. But even the Bank of America strategists who talked about the “perfect storm” admitted that GE is small and “sufficiently idiosyncratic.” Investors should always be mindful of potential market dangers. But when everyone’s pointing out the same pitfall, that’s probably not the one you should be worried about.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2018 Bloomberg L.P.