Dollar Carry Trade May Be Returning as Global Rates Diverge

Dollar Carry Trade May Be Returning as Global Rates Diverge

(Bloomberg) -- Speculation that euro-area monetary officials will consider more stimulus for banks and expectations for further Federal Reserve tightening are causing spreads between U.S. and European debt yields to widen, adding to the case for euro weakness, according to Nomura Holdings Inc.

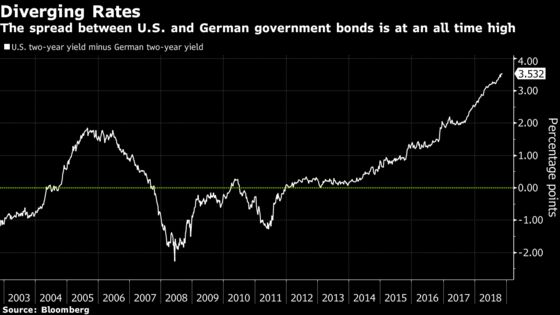

The gap on 2-year Treasury yields over their German counterparts this month surged to about 3.5 percentage points, a record. For Bilal Hafeez, Nomura’s global head of Group-of-10 foreign-exchange strategy, the size of the spread may be enough to spur a carry trade into the dollar.

Europe’s common currency was trading at $1.1242 as of 11:25 a.m. New York time, close to the weakest since June 2017. Hafeez did point to some silver linings for the euro. For one, he sees signals from the financial markets that the risks from Italy’s budget crisis may not spread to the rest of Europe. What’s more, the boost from U.S. fiscal stimulus appears set to wear off next year.

“The yield angle is therefore the most compelling to see further euro weakness,” Hafeez wrote in a note Monday. He added that the euro could settle into a range of $1.10-$1.135, which it stuck to for much of 2015 and 2016.

The outlook for the dollar carry trade, and thus for the euro-dollar rate, is clouded by the potential for a bout of risk aversion that causes the strategy to fall apart, Hafeez wrote. The dollar carry trade against the euro has returned 3.5 percent this quarter, according to data compiled by Bloomberg.

“Equity weakness could lead to such a bout, which complicates the EUR/USD picture,” he wrote.

To contact the reporter on this story: Austin Weinstein in New York at aweinstein18@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Mark Tannenbaum

©2018 Bloomberg L.P.