Dogs of the U.S. Corporate Debt Market Are Its Newest Darlings

Dogs of the U.S. Corporate Debt Market Are Its Newest Darlings

(Bloomberg) -- The U.S. corporate debt market’s weakest links are showing new signs of strength.

Bonds rated in the BBB zone -- the worst performing in the investment-grade universe in 2018 and its least creditworthy members -- are the standout performers early in 2019. Corporate bonds with that rating have returned 0.8 percent in January, compared with the 0.5 percent average for the asset class.

The warm reception of new issues in January testifies to a shift in sentiment on U.S. high-grade debt -- particularly the riskiest variety -- and a growing sense that the tail risks that sent shudders through the asset class last year were overstated.

BBBs Favored

Bank of America’s January survey of fixed-income fund managers showed 38 percent expect the lowest tier of investment-grade bonds to provide the highest risk-adjusted excess returns over the next 12 months, up from just one-in-five in November.

“High-grade investors have responded by expanding their overweight to the highest in a year, from the lowest since the financial crisis,’’ write credit strategists led by Hans Mikkelsen. “Cross-credit investors have moved to embrace BBBs in a big way.’’

BofA head of global cross-asset strategy James Barty is also taking a shine to credit for the first time in around 18 months. He added a long position in debt rated BBB to the bank’s recommended trades on the heels of Mikkelsen’s move to raise high-grade U.S. debt to overweight earlier this month.

“We find yields attractive enough to add this as a carry position as we don’t feel that the end of the cycle is close enough just yet,’’ Barty writes.

The fate of BBBs is poised to set the tone for both investment-grade and junk markets in the years to come. With more BBB debt outstanding than all junk bonds and leveraged loans combined, investment-grade problems could get downloaded to high yield in a hurry if there are a slew of downgrades.

“You only need a couple of those large names to move into HY to really cause more of a liquidity trap within high yield,’’ George Rusnak, the Wells Fargo Investment Institute co-head of global fixed-income strategy, said in an interview on Bloomberg TV.

Fallen Angel Risk

But this fallen angel risk that’s top of the mind among credit investors -- the potential for sizable issuers to be downgraded to junk status and then swamp the high-yield market -- looks overstated, according to Barclays.

Many metrics across the BBB universe that shed light on how likely downgrades are -- including the share rated BBB- and relative concentration among large issuers -- linger at historically normal levels, according to global head of credit strategy Bradley Rogoff.

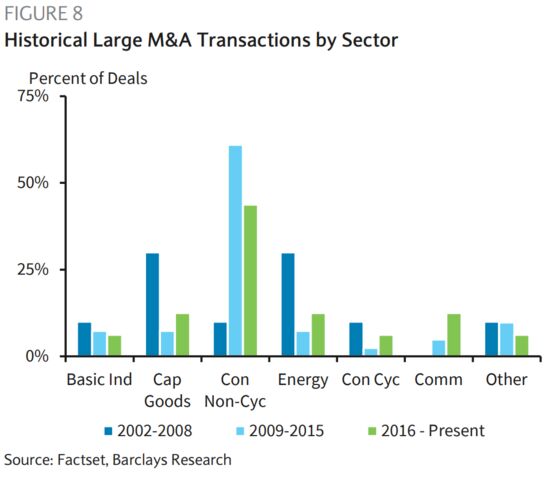

While leverage is elevated, it skews toward companies in defensive sectors that have used debt-funded mergers and acquisitions to grow their businesses and likely have more stable income streams to service obligations amid an economic downturn.

“We see little reason to think that this cycle will be different or worse,’’ he concludes.

Barclays focused in on the potential high-yield archangels: 13 major issuers that would face acute demand challenges if downgraded to junk because their outstanding debt would “overwhelm” the investor base. The most common high-yield benchmark constrains any one issuer to 2 percent of the index by par value.

“A downgrade to high yield for some of the large capital structures could have more drastically negative implication,’’ he writes. “Not only would funding costs increase significantly, but funding a large capital structure -- each of the top 10 BBB would be more than 2 percent of the High Yield Index if downgraded -- in the high-yield market might be downright impossible.’’

To this end, AT&T, Verizon, Anheuser-Busch InBev, CVS Health Corp., Charter, General Electric, General Motors, Ford, AbbVie, Cigna, United Technologies, Kinder Morgan, and Energy Transfer Operating were examined by Barclays fundamental analysts.

“We see a low likelihood of downgrade for all of these names, and even if those chances increase, most have several levers to pull to avoid falling to high yield,’’ Rogoff notes.

Cutting shareholder returns, planned capital expenditures, and in severe cases, asset sales, could often be employed to allow management to meet leverage targets, he concludes.

A previous analysis of potential fallen angel candidates by Wells Fargo showed that firms rated in the BBB universe with a substantial portion of their debt maturing within five years -- in a potentially less-friendly economic environment -- also points to a limited risk of a substantial mismatch between investors’ desires and the characteristics of the downgraded debt in the event of relegation.

To contact the reporter on this story: Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Brendan Walsh, Nikolaj Gammeltoft

©2019 Bloomberg L.P.