At Disney, It’s a Whole New Messy Kingdom

At Disney, It’s a Whole New Messy Kingdom

(Bloomberg Opinion) -- Things are about to get messy at Walt Disney Co.

The conglomerate, which depends on television networks for almost half its operating income, is now looking to partially sidestep cable providers and its arch-nemesis, Netflix Inc., by bringing TV shows and movies directly to consumers through a Disney streaming service to be called Disney+. While the details are still lacking, it’s reasonable to assume that this will lead to a substantial increase in costs for a while and an inevitable hit to revenue and profit (more on that in a moment). Disney’s also nearing the completion of an $85 billion deal for 21st Century Fox Inc. — among the top 10 biggest mergers in history — plus some resulting divestitures that were stipulated by regulators. And because the Fox transaction brings in new faces, it adds even more intrigue to the years-long “Who will succeed CEO Bob Iger?” guessing game.

On Thursday, Disney reported results for the final quarter of its fiscal year that beat estimates and boosted its stock in after-hours trading. Given the company’s new direction, the outlook for 2019 is more relevant than the backward-looking results, though they do spotlight the changing cost picture. Operating income at Disney’s cable networks shrank by $227 million, or 4.2 percent, and capital expenditures of $289 million for the overall media-networks division were the highest since 2011. That’s due in large part to expenses associated with BAMTech, the technology platform Disney has been investing in to power its new ESPN+ app and the soon-to-come Disney+ app. Based on what Netflix spent when its service was still new, Disney may have to shell out $350 million on marketing in its first year, according to Michael Nathanson, an analyst for MoffettNathanson Research.

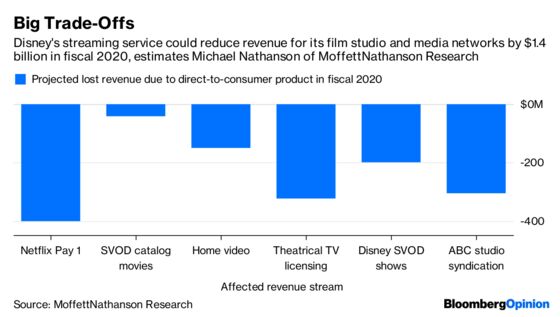

Taken alone, that’s really not an issue for Disney. New products cost money to build, and executives and investors hope they are worth the investment. Where it starts to get messy is when you drill into which content may go on the service and how those decisions affect revenue at Disney’s other legacy divisions. Nathanson projects $1.4 billion of lost revenue and a $1.1 billion hit to earnings before interest and taxes in fiscal 2020. How will Disney determine what to air on traditional networks or show in theaters compared with what it saves for a smaller, less lucrative streaming audience? And when some of its best content does wind up on Disney+, will that create tension with the other businesses? The potential impact on the Disney culture shouldn’t be discounted, especially for a company trying to sort out a succession plan.

There’s also the issue of disjointed messaging. For example, Disney is planning to launch a “Star Wars” TV series exclusive to the streaming service, but subscribers searching there for the “Star Wars” movies may be disappointed because Disney sold those rights to Turner Broadcasting, now owned by AT&T Inc. and has been trying to buy them back. I’ve written that the Achilles’ heel for media companies turning to streaming will be that their array of products is extremely confusing for consumers. There are an increasing number of apps, but the added choice isn’t so meaningful when it requires a research assistant to determine who owns the rights to your favorite series and movies. Subscribers may find that the perfect combination of streaming apps isn’t financially feasible or as appealing as the simplicity of Netflix’s $11-a-month, ad-free offering.

This is all going to make predicting Disney’s future results difficult, potentially calling into question Disney’s stock valuation, which is at the upper end of its peer group. While most of the media giants are trading at discounts to their two- and five-year historical average earnings and Ebitda multiples, Disney is at a premium. The proportion of “buy” ratings among Disney analysts has also held near the lowest since the recession in 2009.

Disney, despite its size and new challenges, has still operated like a well-oiled machine. But it’s entering new territory, and that will come at a price. It’s a good thing Iger is sticking around through 2021 because investors’ faith in the stock has as much to do with their confidence in his ability to navigate these potentially treacherous waters as it does their affinity for the 95-year-old brand.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tara Lachapelle is a Bloomberg Opinion columnist covering deals, Berkshire Hathaway Inc., media and telecommunications. She previously wrote an M&A column for Bloomberg News.

©2018 Bloomberg L.P.