Does AT&T Even Need DirecTV?

Does AT&T Even Need DirecTV?

(Bloomberg Opinion) -- With AT&T Inc. shifting its focus to the newly acquired Time Warner businesses, its struggling DirecTV division is looking less essential. Should DirecTV’s headaches persist, it may even get to the point where AT&T is better off without it.

AT&T bought Time Warner (now called WarnerMedia) for $102 billion last year. Before that, it acquired DirecTV for $63 billion in 2015. These back-to-back megadeals have left AT&T with a net debt balance of $175 billion, making it the world’s largest borrower, aside from financial institutions. As DirecTV loses hundreds of thousands of satellite-service customers and suffers declining Ebitda, there’s some concern among shareholders and bondholders that AT&T could be overburdening itself. This raises questions about AT&T’s ability to keep increasing its dividend and making important investments in fiber and its new 5G wireless network, all while maintaining an investment-grade debt rating.

If the company were faced with a choice between dividend growth or shoring up its credit quality, the latter would have to take priority, as I wrote in November. However, any reduction of the dividend would worsen the sell-off in AT&T’s shares, and CEO Randall Stephenson said last month that he has “no intention of changing the dividend philosophy.” That’s why selling DirecTV may be a more feasible option, if one is ever needed. This may sound radical, but hear me out.

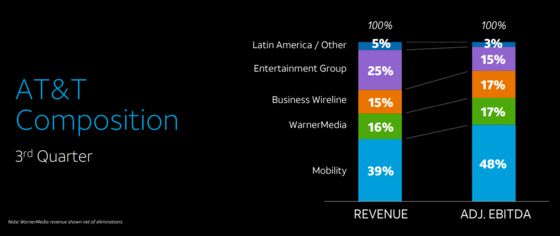

Unlike a dividend cut, letting go of DirecTV would be able to address two issues: AT&T’s creditworthiness and its stock valuation. That’s because DirecTV’s complications are primarily what’s clouding the picture. When AT&T highlighted this chart in its last earnings presentation, what struck me is that even company-provided material can’t hide that the Entertainment Group (the bulk of which is DirecTV) isn’t earning its keep:

Originally, DirecTV seemed to play a key role in Stephenson’s vision for buying the WarnerMedia assets. The pay-TV business was the clearest link between his newfound Hollywood aspirations and AT&T’s core competency of providing connectivity services to customers. Except now, AT&T is on the verge of launching yet another streaming service, this time through the WarnerMedia unit — not the DirecTV/Entertainment Group, where one would think all its pay-TV stuff would be housed.

The new product will offer on-demand viewing of various WarnerMedia content — shows and movies from HBO, Warner Bros. and Turner — across three different package price points. The company has pitched it as being complementary to DirecTV Now, which is for customers who prefer to stream live TV. But it’s not difficult to imagine that a Netflix-like app full of popular on-demand content may instead cannibalize DirecTV Now.

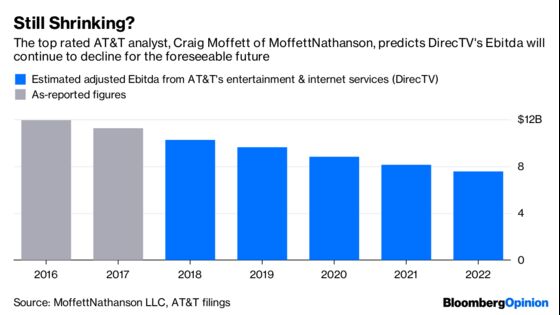

Stephenson predicts that DirecTV’s Ebitda will stabilize this year, and that’s key to AT&T hitting its leverage-reduction goals. His optimism is partly predicated on higher prices for DirecTV services and a shift away from promotions. I’ve wondered whether that approach will backfire by driving more customers to competing products — the forthcoming WarnerMedia app now included.

Still, AT&T shouldn’t necessarily hold onto DirecTV if it continues to weigh on results and the company’s perception in the stock and bonds markets. The business has never been able to thrive within AT&T, and its awkwardness is only becoming more obvious.

Both transaction totals include net debt.

AT&T is also looking to sell other assets, which it says will generate up to $8 billion of cash to help pay down debt.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tara Lachapelle is a Bloomberg Opinion columnist covering deals, Berkshire Hathaway Inc., media and telecommunications. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.