Dire Bond Returns Have 60/40 Managers Juicing Portfolios With FX

Dire Bond Returns Have 60/40 Managers Juicing Portfolios With FX

(Bloomberg) -- It was a dinner conversation with former Federal Reserve Chairman Ben Bernanke in early 2020 that convinced Cesar Perez Ruiz that the golden age of bond investing was over.

The rate on trillions of dollars in debt had sunk below zero, upending one of the pillars of international finance: that borrowers always pay interest. For Bernanke, it was a deflationary signal that could not be ignored. For Ruiz, chief investment officer at Pictet Wealth Management, it was a sign that he eventually may need to get out of bonds -- and instead turn to FX plays, like wagering on the euro or the yen.

Then the coronavirus crisis hit and sent yields on 10-year Treasuries, the asset underpinning much of the global economic system, to within half of a percentage point of 0%. “That was the click for me,” said Ruiz. “We cannot play this. This is a nice trade that has worked since the ‘90s when I started, but not now. It can’t be the solution.”

Since then, Ruiz’s fixed-income managers have ramped up the share of portfolios dedicated to taking advantage of a resurgence of volatility in currencies. At least a fifth of Pictet’s absolute-return funds are now focused on playing FX, up from next to nothing at this time last year. Sell-side fixed-income strategists like HSBC’s Steven Major are also recommending investors diversify away from bonds, as is tail-risk hedge fund LongTail Alpha, and volumes in the $6.6 trillion-a-day currency market have popped higher.

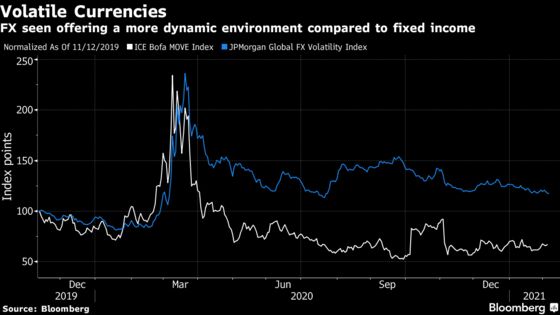

It’s a sign that opportunity is returning to the world’s biggest market, challenging a low-volatility regime that engulfed foreign exchange in the wake of the financial crisis. Price swings are the lifeblood for traders; without them, profits can’t be made and hedge funds have to close shop. As central banks plowed money into financial markets, investors previously had preferred to seek returns riding a three-decade long bull run in bonds or by chasing the record-breaking stock rally, rather than watch the paint dry in currencies.

The new players are now showing up in daily foreign-exchange volumes. In North America, trading soared 22% in October versus April to $933.4 billion a day, the highest since 2018, according to a semi-annual report from the Federal Reserve Bank of New York. Turnover in London, the world’s biggest currency hub, also bounced 7% to more than $2.5 trillion.

The traditional 60/40 portfolio, which refers to a hypothetical mix of 60% equities and 40% bonds, is designed to be almost foolproof in both risk-off and risk-on markets. But it has come under threat of late as losses in the stock market are sometimes met with little more than a shrug in U.S. Treasuries, rather than a rally that protects the entire portfolio.

“Bonds don’t diversify,” Ruiz said. “They don’t do anything.”

Currency trades are also taking a larger share in multi-asset portfolios at Pictet’s wealth management arm, which oversees 233 billion Swiss francs ($260 billion). Bets on the yen last year netted a four-fold return at a time when Japanese bonds oscillated in a narrow range. Pictet, which has hired a specialist currency strategist, positioned for euro appreciation on the back of the European Union recovery fund and played the pound around Brexit.

“We made a fortune,” said Ruiz.

The trend of central bank dominance may have reached a tipping point and it’s now the bond market’s turn to be mired in a low-volatility regime. A phenomenon of monetary policy’s dominance of markets that was once confined to Japan has reached Europe, and trading in government debt is dropping off a cliff. Price swings in both the safest assets, German bonds, and the riskiest -- like Italy’s -- are at their tightest in at least a decade. Lend money to Germany for 10 years and you’ll effectively have to pay around 0.5% for the privilege. The U.S., while further behind, may not be immune forever, either.

By contrast, a gauge of currency swings has climbed against its bond-market counterpart on a relative basis, with the gap between the two hitting the highest since 2008 at the end of last year.

Other long-time stalwarts of the fixed-income market are also rethinking their approach. Throughout much of Steven Major’s 35-year career, he has been known as a bond bull, consistently arguing in favor of more gains in prices in the world’s $60 trillion market. Now, though, even he is being forced to consider other asset classes in an effort to boost diminishing returns for clients.

In a letter entitled “How to spice it up in a dull market” written to clients -- but also, he admits, to his own colleagues -- HSBC’s Major argued that bond investors may have to look elsewhere to secure the returns they had been used to over the past decades. Developed market strategists will have to become more like their emerging market peers and cover both bonds and FX, he added. HSBC has already made that change for its Australia and New Zealand analysts.

‘Into the Mud’

“You shouldn’t look for too much sex, drugs and rock and roll” in bond markets now, Major said in a telephone interview. “U.S. Treasuries have been brought back into the mud. The easy pickings just aren’t there. We have to take more risk on foreign exchange.”

Be it bets on the vaccine rollout, or a simple prediction of which nation’s economy is going to allow its central bank to lift interest rates first, currencies are proving the most-versatile way to express a macro view and hedge risky elements of a portfolio. The traditional 60/40 model is no longer suitable as a bastion against risk events, according to Pictet’s Ruiz.

The sheer size of the FX market also means that it is far less vulnerable to manipulation than equities have been during recent Reddit pile-ons. “Capital markets end up trying to look to express your view in one of the things that’s unmanipulatable -- and that’s FX, ” he said. “This is just the beginning.”

That’s also the thinking of Vineer Bhansali, who spent 16 years at bond giant Pacific Investment Management Co. before founding Newport Beach, California-based LongTail Alpha, a fund that focuses on volatile-market strategies. Hedging FX-market swings has long been used as a key strategy to flip negative-yielding bonds into positive-yielding ones. But the risk is that a sudden move in interest rates could spark a massive repatriation of that cash. Bhansali is using options -- positions predicated on the potential for large swings in currencies -- to prepare.

“The next big move is going to happen in the currency markets,” he said. “Nobody knows exactly when it will happen as nobody knows when the central banks will change course. For now global central banks and fiscal authorities have remained very powerful. But at some point stuff will break.”

©2021 Bloomberg L.P.