Debt-Limit Deal May Fail to Spur Bill-Supply Surge Market Craves

Debt-Limit Deal May Fail to Spur Bill-Supply Surge Market Craves

(Bloomberg) -- U.S. Senate leaders’ short-term deal to increase the debt ceiling may still fail to deliver the kind of surge in supply that front-end fixed-income investors have been craving all year.

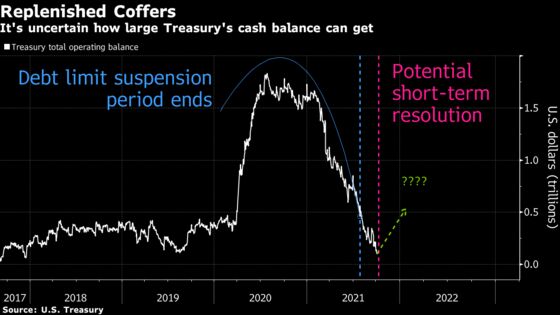

The expected increase in Treasury-bill issuance would hinge on how large the department’s cash pile will be in the coming months. That promises to be a big question mark heading into December, depending on the details of the debt-limit agreement and their implication for the new x-date for avoiding default.

Bank of America Corp. strategists estimate that the added net supply by year-end could be as low as $140 billion -- to cover expected deficits -- or as large as $500 billion if the Treasury General Account can be rebuilt in early December. Such a boost to supply could put upward pressure on rates of bills maturing between now and year-end, but that may be no higher than 5 basis points, the analysts say.

“That’s the key question,” said Priya Misra, head of global rates strategy at TD Securities. “If there is a numerical rise and Treasury can’t raise the cash balance much, then not much normalization in supply. I don’t see high bill rates in November though, so the market probably expects not a ton of supply.”

Treasury bills rallied after Wednesday’s announcement of a potential short-term deal, removing the dislocations in securities maturing in late October and early November. However, most T-bills yield less than 0.05%, which is the offering yield on the Fed’s reverse repo facility.

Investors, particularly money funds, have been flooded with cash that has overwhelmed U.S. dollar funding markets due in part to the Federal Reserve’s asset purchases and drawdowns of the Treasury’s cash account, which is pushing reserves into the system.

As a result, liquidity has been swelling, especially since the department has removed roughly $1.28 trillion of supply from the market this year. That’s also pushed investors to park more cash at the Fed’s reverse repurchase agreement facility, which reached a record $1.6 trillion at the end of September.

In its last round of financing estimates, the Treasury had projected its cash balance would rise to $800 billion by the end of the year. While a short-term resolution would give the department room to boost its cash pile, it may be by a smaller magnitude and shorter time horizon than the market was previously anticipating, which also means less bill supply.

A key point not included in the proposal from Senate Republican leader Mitch McConnell was the extent to which Republicans would allow the Treasury to replenish its cash balance at the Fed and whether the department would be allowed to replenish the government retirement funds that it tapped for extraordinary measures.

“These two points will determine the length of time between reaching the new debt ceiling and the new x-date which could be several months further out,” Bank of America strategists included Ralph Axel and Mark Cabana wrote in a note to clients. “These details matter for the path of Treasury issuance, especially bill supply.”

©2021 Bloomberg L.P.