Dan Fuss Warns on the Real-Income Hit to Boomers as Bonds Slump

Dan Fuss Warns on the Real-Income Hit to Boomers as Bonds Slump

(Bloomberg) -- As a child in the 1940s, Dan Fuss watched helplessly as the price of his favorite ice cream doubled in just one day.

Later, he was vindicated as a bond market “vigilante,” when he and others exhorted U.S. administrations to curtail fiscal deficits and wrest control of the inflationary breakout of the 1980s.

But all that experience doesn’t make the biggest bout of consumer price growth in nearly four decades much easier for the 88-year old vice chairman of Loomis Sayles -- and the generation of pensioners whose investments he helps oversee.

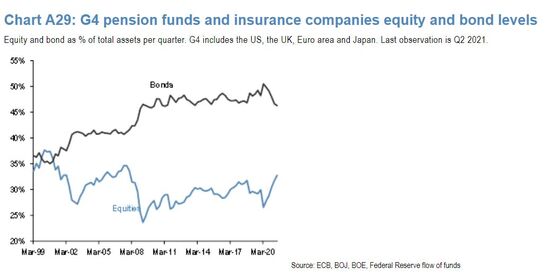

Boomers and the like may have the most to lose from price pressures and rising rates that are punishing bonds, which account for 45% of assets held by pension funds and insurers in the world’s biggest markets, according to JPMorgan Chase & Co. Pensions oversee $30 trillion overall in the U.S., Britain, Europe and Japan, the data shows.

These funds have boosted their bond allocations from 35% two decades ago as easy-money policies encourage governments and companies to borrow at rock-bottom rates.

“People most affected by inflation are those on fixed incomes, especially if their income is not indexed to inflation. Most retirees are in that category,” Fuss said in an interview. “Their income will not catch up with rising prices.”

A preference for fixed income puts the older generation in an uncomfortable position with the Treasury index in line for a second year of losses -- an event last witnessed in 1974 -- as the Federal Reserve pares pandemic stimulus. Already, U.S. government bonds have lost 1.5% in less than two weeks of trading.

While pension funds have enjoyed a multi-year bond rally up until last year, the older crowd are now enduring negative returns on the asset class. By contrast, younger traders appear decidedly more relaxed.

Ben Kumar, a 33-year old fund manager at Seven Investment Management in London, has been buying value stocks tied to a cyclical upswing. He expects the current surge in the cost of living to fade as Covid-related supply disruptions eases, and says inflation-hedging instruments hold little appeal.

Vigilantes Muffled

Treasury Inflation Protected Securities that pay negative real yields could only attract people who are “absolutely petrified about inflation,” he said.

Fuss’s own grandson is a direct beneficiary of inflation when it comes to wages. A specialist in cloud technology, he’s sought-after on the job market and has put away enough money to hike the Appalachian trail for six months.

“His income seems to go up quite nicely,” Fuss said. “I don’t worry about him at all.”

Fuss remains hopeful government bond yields will steady after rising to the highest in two years. At any rate, he’s not expecting anything like the levels of 1982, the last time inflation hit 7%.

Back then, investors weren’t even tempted by Treasuries bearing a 15.75% coupon, boycotting auctions as a way to protest against excessive debt levels. Would-be vigilantes these days have been muffled by the Fed’s massive bond-buying machine suppressing yields.

Fuss is still careful. If yields keep rising much higher from here, he’d prefer to cash out of long-dated debt before it mature -- an approach known as riding the yield curve.

“Once rising prices spill over into wages, my experience is that it could stay in the system longer than some are prepared for,” he said.

©2022 Bloomberg L.P.