Curve Inversion May Lead U.S. Banks to Tighten Lending Standards

Curve Inversion May Lead U.S. Banks to Tighten Lending Standards

(Bloomberg) -- For all the questions over the outlook for the U.S. Treasury yield curve, one thing looks clear: If it inverts, banks will tighten lending standards, potentially adding headwinds to economic growth.

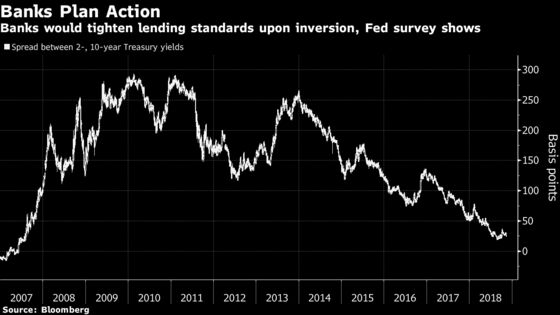

Federal Reserve policy makers and market participants alike have been watching this year as the gap between short- and longer-term rates has narrowed. In August, the curve from 2 to 10 years reached the flattest since 2007, in part as traders priced in Fed policy tightening. Historically, recession has followed inversions, though it’s unclear why that relationship exists.

Banks told the Fed that they would tighten lending standards if short-term rates rise above their long-term counterparts, the central bank said Tuesday in results of an October survey of senior loan officers. Asked how an inversion of the yield curve would impact lending practices, a “major share” of banks in the survey said they’d become less profitable and more risk-averse.

The gap between 2- and 10-year Treasury yields has rebounded to about 25 basis points, after reaching as low as 18.3 basis points in August. It hasn’t been inverted since 2007. Many strategists, including John Herrmann at MUFG Securities Americas Inc., predict the curve will eventually invert in 2019.

Banks saying an inversion would cause them to tighten lending standards would be “like a piling-on effect in terms of a slowdown, as tighter lending standards tend to reinforce any slowdown,” Herrmann said.

Survey respondents also said they’d view inversion as “signaling a less favorable or more uncertain economic outlook and as likely being followed by a deterioration in the quality of their existing loan portfolio.”

The survey comments contrast with the views of some central bankers, including New York Fed President John Williams, who has said policy makers shouldn’t hesitate to allow short-term rates to exceed longer-term rates.

“There are a host of reasons why the curve continues to have this flattening bias, and at some point it brings the inversion into play,” Herrmann said.

To contact the reporters on this story: Liz Capo McCormick in New York at emccormick7@bloomberg.net;Randall Woods in Washington at rwoods13@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, ;Sarah McGregor at smcgregor5@bloomberg.net, Mark Tannenbaum, Randall Woods

©2018 Bloomberg L.P.