Credit Suisse Blow-Ups Give Gottstein a Crash Course in Risk

Credit Suisse Blow-Ups Give Untested CEO a Crash Course in Risk

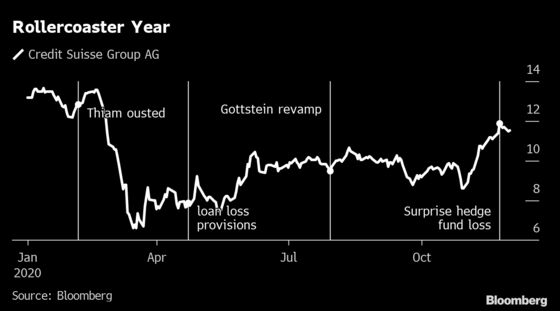

(Bloomberg) -- Two months after Thomas Gottstein took over at Credit Suisse Group AG following a damaging spying scandal, the new chief executive found himself defending losses the bank had incurred in one of Asia’s most spectacular accounting frauds: Luckin Coffee Inc.

It was only the beginning. From questionable deals arranged for SoftBank Group Corp. to a $450 million hit from an investment in hedge fund York Capital, Gottstein has confronted one setback after the next in his short reign atop Switzerland’s second-largest lender. The losses and scandals, many of which he inherited, have compounded the damage inflicted by the global pandemic and now threaten to plunge the bank to a fourth-quarter loss.

Gottstein, who is due to give investors a strategy update on Tuesday, has moved to centralize risk and compliance in Zurich, simplify the organizational setup and scale back lending growth. He’s started a review of the asset management unit after a series of fund implosions. But by and large, the new CEO has shied away from more decisive moves, arguing the missteps aren’t connected and defending Credit Suisse’s appetite for risk as he seeks to win business from the world’s richest clients.

“Credit Suisse has a very solid credit loss track record both in the periods before Covid-19 as well as in 2020 during the economic downturn caused by the pandemic,” a spokesman for the bank said by email. “This also underscores the strength and resilience of our business model, including and especially our strategy to be the leading bank for entrepreneurs.”

Gottstein declined to comment for this story.

Thiam’s Legacy

A two-decade Credit Suisse veteran, he took over in February after revelations that the bank had spied on employees led to the ouster of Tidjane Thiam. He vowed to restore calm while continuing the strategy of his predecessor, who had scaled back volatile trading and tied the investment bank more closely to the needs of the bank’s wealth management clients, offering bespoke deals or loans against their assets.

Almost immediately after Thiam’s departure, the pandemic exposed some of the risks Credit Suisse had been taking, particularly in extending credit to the rich. In the first nine months, Credit Suisse set aside $1.1 billion for loan losses, more than its larger cross-town rival, UBS Group AG, which has a similar strategy. Its shares have declined about 14% this year, compared with a 2.8% gain for UBS.

While some of that reflects different ways of accounting, Credit Suisse is known to be more flexible than some peers when it comes to lending to rich clients, said people familiar with the matter. In a business where banks typically extend credit against diversified investment portfolios, it will occasionally accept single stocks and collateral that’s harder to value, such as ships and aircraft, the people said, asking not to be identified discussing internal information.

Warner’s Rise

“Credit Suisse’s strategy is different from plain vanilla private banking,” said Andreas Venditti, an analyst at Vontobel in Zurich. “You have huge billionaires, you advise them on their companies, provide loans left, right and center to win and retain them. The more interesting these clients are, the higher you go up the risk curve.”

Much of that risk appetite had been shaped over recent years by Lara Warner, a Thiam confidante who was tasked with cleaning up legacy issues and eventually reset risk management under the new strategy. When Thiam was forced out, some in Zurich expected Warner to follow along with other members of his inner circle, but Gottstein instead promoted her to Group Chief Risk and Compliance Officer -- two functions that were previously separate.

Warner has challenged risk managers to stop thinking only about defending the bank’s capital and also look at strategic business priorities, according to the people. The combination of the risk and compliance functions that she now oversees will likely see hundreds of roles eliminated as the bank seeks to remove overlap. At least 20 senior staff -- mostly managing directors -- have already departed in just under two years.

Much of her approach reflects a broader shift in the industry, with banks viewing risk departments less as a control function and increasingly as a tool to help reach strategic goals, the people said. But recent stumbles have raised questions about whether Credit Suisse prioritized revenue growth at the expense of risk and compliance.

Luckin, SoftBank

Luckin Coffee, the onetime challenger to Starbucks, is a case in point. Thiam had praised founder Lu Zhengyao as the “poster child” for his strategy of doing more business with wealthy Asian entrepreneurs. Credit Suisse lent Lu millions of dollars and arranged the company’s lucrative initial public offering in 2019, but was left staring at steep losses, along with other lenders, when the stock imploded in an accounting fraud.

The bank also came under fire for a number of deals it arranged for another key Asian client, Masayoshi Son’s SoftBank. In late 2019, Credit Suisse bankers helped now-defunct Wirecard AG sell 900 million euros of convertible bonds that Softbank had agreed to buy, and then quietly helped Softbank cut its exposure. SoftBank again was at the center of another debacle involving a group of Credit Suisse supply chain finance funds.

Meanwhile, Credit Suisse’s business in the Middle East and Africa was hit by a fraud case when a relationship manager who had lost money for a client used other clients’ money for unauthorized trades to cover up the losses. The matter was particularly damaging because Credit Suisse had been criticized by a regulator two years earlier in a similar case that had raised questions about controls.

As head of compliance, Warner had worked with third-party vendors on new tools to improve controls, including a venture with Silicon Valley’s Palantir Technologies Inc. to catch rogue employees. But by mid-2017, the bank had quietly given up on the project, named Signac. While Credit Suisse continues to work on similar tools, they haven’t been able to prevent the latest fraud.

Fund Headaches

Gottstein has called the Luckin losses “unfortunate” but said it would not change Credit Suisse’s strategy of targeting entrepreneurs in Asia. In the asset management business, the bank has overhauled the supply chain finance funds at the center of the SoftBank scandal, while saying it had confidence in the control structure at the unit.

Still, behind the scenes, he’s slowed lending growth, both compared with previous years and relative to the competition, according to a person familiar with the matter. He also started a strategic review of the asset management business, a unit that’s typically a source of stable income with little risk for the bank, but which suffered a long series of fund implosions this year.

Just last week, the lender announced that two reinsurers that it had backed through the unit would stop underwriting new business after investors decided to pull their money from the funds. The bank has also shuttered a quantitative strategy and took a 24 million franc charge on seed capital in a U.S. real estate vehicle in the third quarter. A joint venture with the Qatar Investment Authority is closing two groups of funds and returning capital to investors.

One of the most painful setbacks came last month, when Credit Suisse announced a $450 million impairment on its stake in York Capital Management. While the investment was made almost a decade ago, and Credit Suisse has since moved away from third-party managers, the charge -- along with a potential legal provision of $380 million for a case dating back to the financial crisis -- risks pushing the bank into the red for the fourth quarter, according to Venditti.

“There is no link between these cases,” Credit Suisse said. “Two of them relate to allegations of external fraud, in which investors and supervisory authorities were misled. They have nothing to do with the legacy RMBS civil law proceedings, which date back over a decade, or impairments taken on a non-controlling stake in a company that the bank has owned since 2010.”

©2020 Bloomberg L.P.