Liquidity Angst Builds in Bond Market on Surging Risk Indicators

Credit-Risk Concerns Build as Key Market Stress Indicator Surges

(Bloomberg) -- Anxiety about an emerging liquidity crunch is roiling global bond markets.

A key gauge of banking-sector risk, known as the FRA/OIS spread, soared to its highest level in almost two years, while dollar swap spreads widened, suggesting stresses in U.S. markets are becoming increasingly severe. Here are five charts to watch for further angst:

The two-day blow-out in the FRA/OIS spread -- a U.S. money-market benchmark that measures the difference in rates between forward-rate agreements and overnight index swaps -- shows increased perceptions of interbank lending risk or dollar hoarding. The gauge jumped from around 12 basis points at the end of February to over 50 basis points Friday, before paring.

A similar measure for euros widened to a level unseen since September, while futures on Euribor -- the European bank lending rate -- fell. On Thursday, speculative puts were scooped up, hedging for a bigger drop, despite traders pricing in about 9 basis points of rate cuts by the European Central Bank next week.

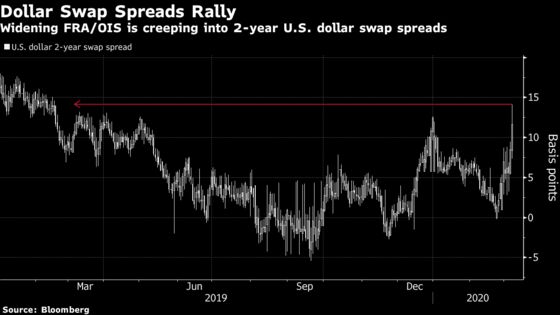

U.S. swap spreads widened, indicating higher risk levels perceived by counterparties in interest-rate swap agreements. The two-year sector rose to its highest level in over a year.

“We are on high alert for any spill-over not just into funding today but credit markets,” NatWest strategists led by John Briggs wrote in a note to clients. “We are concerned that there are skeletons out there in closets we may not be aware of that come out in times like this, particularly leverage from the shadow banking system.”

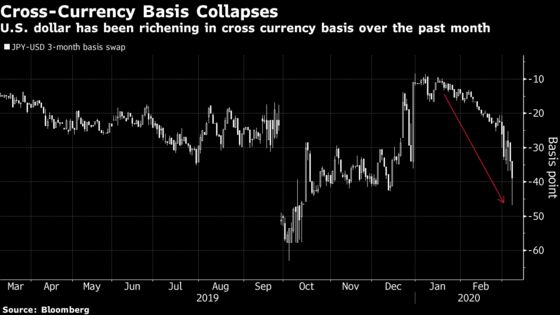

Cross-currency basis swaps -- the rate that international investors pay to switch their local currency for dollars -- also showed a sharp increase in demand for the greenback.

The three-month yen basis touched its widest levels of the year and similar euro and sterling swaps also saw increased volatility.

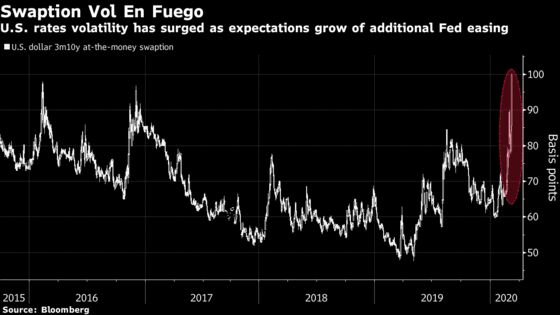

U.S. rates volatility is on fire, with widening swap spreads and convexity triggers on traders’ radars. The at-the-money three-month-10-year swaption hit the highest levels since 2016, fast approaching 100 basis points in annualized volatility on Friday.

Read More: JPM Sees Risk of Higher U.S. Rates Vol After ‘Mini Flash Rally’

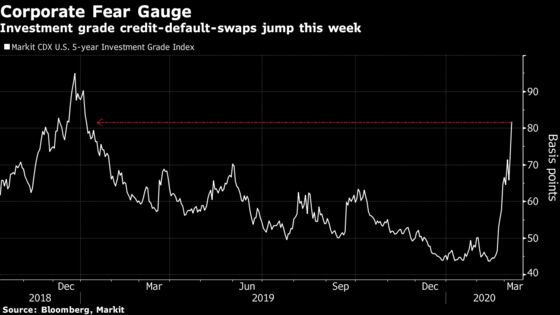

The cost to protect against default on investment-grade credit jumped to the highest in more than a year on Friday, adding to aggressive moves from a day earlier.

Traders are struggling to digest the impact of the coronavirus on the economy and their jobs, spurring an epic rally in global bonds. Equities around the world tanked and bets on further central-bank easing rose, but many now fear that this volatility could hurt liquidity.

“We are staring at the abyss of a credit crunch,” said Kaspar Hense, a portfolio manager at BlueBay Asset Management, noting in particular the widening of dollar FRA/OIS.

To contact the reporters on this story: Edward Bolingbroke in New York at ebolingbrok1@bloomberg.net;Alexandra Harris in New York at aharris48@bloomberg.net;Stephen Spratt in Hong Kong at sspratt3@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Rachel Evans, Debarati Roy

©2020 Bloomberg L.P.