Credit Markets Flash a Liquidity Warning That Pimco Saw Coming

Credit Markets Flash a Liquidity Warning That Pimco Saw Coming

(Bloomberg) -- Pimco’s fund managers are concerned that liquidity in corporate bonds is drying up when investors need it the most. They’re right.

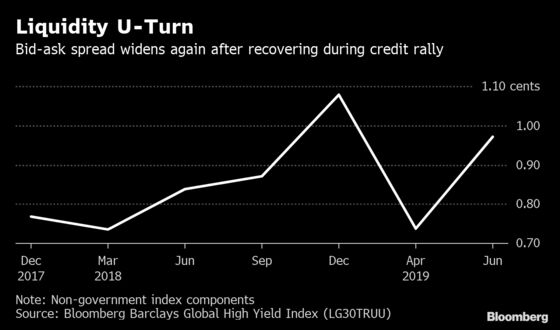

A key gauge of trading conditions in riskier bonds is close to reprising December levels, belying the relative calm in global credit markets, according to data on bid-offer spreads compiled by Bloomberg. It shows the cost to cash out of corporate bonds keeps getting bigger during sell-offs, when funds often face redemptions.

It all helps to explain why Pacific Investment Management Co. said this week that “challenging liquidity conditions’’ aren’t going away anytime soon, according to the latest outlook from the $1.76 trillion asset manager.

A glance at bid-ask spreads of global junk bonds, the difference between prices dealers quote to buy and sell, highlights the quandary. That gap stood at 0.96 cents per dollar on Wednesday, near the highest since the December-January rout, according to Bloomberg data.

Conversely, during the first-quarter melt-up in markets, ample demand for risk assets kept corporate trading well-oiled.

While bid-offer spreads are closely watched, they’re just one of many indicators for credit risk.

The more-widely cited is of course credit spreads, the difference in yields on bonds on company debt with default risk and government debt. Those remain below highs of early January even after widening 76 basis points from mid-April lows of about 400 basis points, according to Bloomberg Barclays indexes tracking global high-yield debt.

Red Flags

Patchy liquidity is a legacy of post-crisis regulation that has thwarted banks’ ability to hold inventory of corporate bonds. With dealers less able to warehouse risk to help investors ride out tough conditions, trading has become “more frictious,’’ according to Pimco portfolio manager Geraldine Sundstrom.

The market is “more prone to bouts of volatility,’’ Sundstrom said at a briefing in London Tuesday.

The firm declined to comment on whether it’s selecting bonds on the basis of liquidity during credit downtrends, but in December group chief investment officer Dan Ivascyn said it’s been relying more on credit derivative indexes than single-name cash bonds.

Others have recently raised red flags on hard-to-trade corporate bonds. In April, strategists at UBS Group AG said that “dizzying’’ moves in the credit market are down to rapidly rising and falling liquidity.

Meanwhile, the downfall of star U.K. fund manager Neil Woodford shows the pitfalls of building a portfolio around illiquid, unlisted stocks.

That’s helped feed demand for more-liquid CDS, especially as a trade war opens on multiple fronts, and political risk in the U.K. and Italy mounts. Trading volume in both U.S. and European credit-default swap indexes jumped last month, with Europe’s investment-grade tracker having its busiest month in 2019, according to Bloomberg data.

To contact the reporter on this story: Tasos Vossos in London at tvossos@bloomberg.net

To contact the editors responsible for this story: Hannah Benjamin at hbenjamin1@bloomberg.net, Cecile Gutscher, Sid Verma

©2019 Bloomberg L.P.