Corporate Bonds Are on Fire After the Fed’s Dovish Signal

Corporate Bonds Are on Fire After the Fed’s Dovish Signal

(Bloomberg) -- Fear is turning into exuberance in credit markets.

Demand for U.S. corporate bonds has surged after the Federal Reserve signaled that it’s done raising interest rates for now and eased investor concerns that rate hikes will choke off economic growth and crimp profits. High-yield bonds gained 4.9 percent this year through Thursday, the best start to a year since 2009, and saw the biggest fund inflows this week since July 2016.

High-grade bonds on Thursday reached their highest levels since late 2017, according to Bloomberg Barclays index data. For new offerings, investors this week put in six or eight times as many orders as there are securities for sale, about two or three times the usual levels of oversubscription. Strategists at JPMorgan Chase & Co. and Bank of America Corp. think there’s a lower chance of a recession now, and have been growing more bullish on corporate debt, at least for the near term.

“There was a dovish surprise,” said Gene Tannuzzo, deputy global head of fixed income for Columbia Threadneedle Investments, which manages $485 billion. There are still risks for credit, including slowing global growth. But the Fed’s shift “should be positive for credit, and that’s what we’ve seen: demand is coming back into high yield and investment grade.”

Read More in the Credit Brief: Pain in Weak Covenants and Unsold Loan Deals

The riskiest of assets have been rallying the most. Bonds rated in the CCC tier, at least seven levels below investment-grade, have gained 5.7 percent so far this year through Thursday, according to Bloomberg Barclays index data. Clear Channel Outdoor Holdings Inc., a billboard company, sold $2.24 billion of notes rated CCC+ as it gets ready to separate from iHeartMedia Inc., the bankrupt radio broadcaster that owns it, which was the largest offering at this rating level since September.

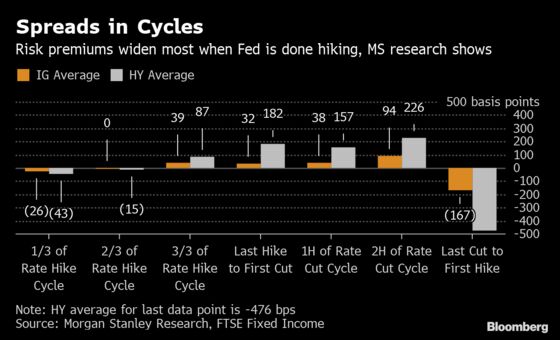

It’s not clear how long the party will last. The easy money has already been made in the securities, wrote Morgan Stanley strategists led by Adam Richmond in a note dated Jan. 25. Risk premiums, or spreads, often start widening toward the end of the rate hike cycle as economic growth slows. They continue deteriorating as the Fed switches over to cutting rates, the strategists said.

“For the long-term investor, you still have to think about what your bonds are worth in different environments like a weaker economy or a much more hawkish Fed,” said Bill Zox, chief investment officer of fixed income at Diamond Hill Capital Management, which oversees about $21 billion.

Leveraged lending is the most hazardous part of banks’ syndicated loan portfolios, because so much debt has been piled on weaker companies, banking regulators cautioned last month. Lending agreements are giving less protections to investors, which means that when loans go bad investors might end up recovering just 50 cents on the dollar, down from historical levels closer to 80 cents, UBS credit strategist Matthew Mish said at the end of January.

And there are early signs that economic growth may be deteriorating. Global exports shrank in January for the second consecutive month, and countries from China to Germany are reporting weakness in manufacturing activity. Anxiety about trade weighed on U.S. stocks this week, leaving equities on track for their first weekly loss of the year. U.S. consumer confidence fell in January to the lowest level since mid-2017 amid the government shutdown.

Good Signs

But there are other signs that everything is fine. U.S. manufacturing was unexpectedly strong in January, and employer hiring last month jumped by the most in almost a year. Any signs of slowing growth could keep the Fed at bay even as earnings stay relatively strong, in a replay of the post-crisis, bad-news-is-good-news investing strategy. Dovish central banks mean that the first half of 2019 will likely be similar to 2016, wrote strategists with BNP Paribas in a note dated Jan. 31.

That’s giving comfort to corporate bond investors. The cost to protect high-grade debt against default has dropped to around its lowest level since mid-November. Micron Technology Inc. on Monday sold $1.8 billion of notes with investment-grade ratings from two firms and junk grades from S&P Global Ratings. The securities had almost six times as many orders as there were notes for sale.

Amid the demand, supply has been light. U.S. investment-grade bond sales for the year are at their lowest levels since 2015, according to data compiled by Bloomberg.

“The Fed is saying risk is OK, the party is going to play on for a while,” said Mark Spindel, chief executive officer of Potomac River Capital in Washington. “Speculative assets have a lot of runway to keep going, if the Fed keeps interest rates low and lets markets run a little bit hotter.”

--With assistance from Gowri Gurumurthy and Sally Bakewell.

To contact the reporters on this story: Molly Smith in New York at msmith604@bloomberg.net;Rebecca Choong Wilkins in New York at rchoongwilki@bloomberg.net;Janine Wolf in New York at jwolf71@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Dan Wilchins

©2019 Bloomberg L.P.