Corporate Bond Buyers Seeking Yield Take Treasury Rout in Stride

Corporate Bond Buyers Seeking Yield Take Treasury Rout in Stride

(Bloomberg) -- It’ll take more than this week’s steep sell-off in Treasuries to deter corporate bond investors. The global rout may actually boost demand from yield-hungry buyers.

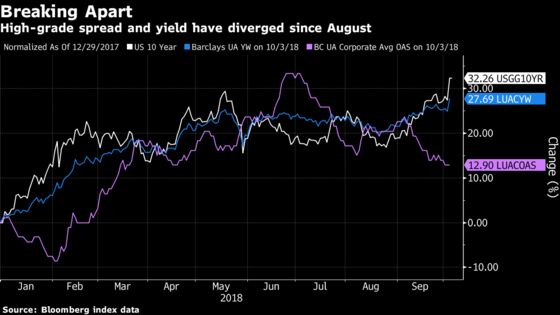

As Treasury yields touched the highest in seven years this week, investment-grade spreads in the U.S. fell to their lowest since April, while junk traded at the tightest since 2007.

The thinking among investors is that the surge in U.S. government yields is due to strong economic data -- the pickup in employment, wages and consumer confidence -- and roaring growth should be a boon to corporate balance sheets.

“Rates have moved up consistent with positive economic numbers -- the backdrop for corporate credit is still favorable,” said Scott Kimball, Miami-based portfolio manager at BMO Global Asset Management, which has about $260 billion in assets.

And what many consider to be a slow march higher in rates may also attract credit investors.

“If we get a slow, controlled rise in rates like I think we really have, that’s very positive for credit,” Timothy Doubek, senior portfolio manager at Columbia Threadneedle Investments in Minneapolis, said by phone Thursday. “What we are seeing is an increase in participation from U.S. investors who are more yield-oriented,” said Doubek, whose firm had about $169 billion of fixed-income assets under management as of June.

Short-End Bias

However, bonds with the longest duration have the greatest sensitivity to changes in interest rates, and investment-grade securities with lower coupons and longer maturities have the longest duration. This risk can be seen in the benchmark $33.7 billion LQD ETF, with an 8.4-year duration, which has hit multiyear lows.

The maturities of newly-issued bonds may shorten amid higher yields, given investors are likely to be asking for greater compensation for longer-duration bonds. As a result, investors will be watching to see if any more deals are postponed or altered, as well as the next-day performance of new issuance.

Volksbank Wien AG on Thursday postponed an about 150 million-euro ($170 million) sale of additional Tier 1 notes, the riskiest form of bank debt, after setting a final coupon. The lender follows electronic payments technology provider Ingenico Group SA and French lender My Money Bank in pulling a deal.

Borrowing Costs

While spreads may be shrinking, actual borrowing costs are still on the rise for corporate issuers, and that may make the weakest more vulnerable. A lot of zombie companies kept afloat through the latest credit rally -- which particularly favored the riskiest end of the market -- may not be able to repay their debts.

“There is no greater input than the cost of money,” Peter Boockvar, chief investment officer at Bleakley Advisory Group, wrote in a note Thursday. “I have no idea when the next economic downturn comes, but I’m very confident that when it does it will be triggered by a rise in rates that at some point hurts.”

It’s not just Treasuries. Costs have increased for leveraged-loan issuers because they are tied to floating rates, and Libor recently touched a 10-year high. But most of the debt isn’t due anytime soon. And if the U.S. economy is indeed set for further growth, then the bull case -- that heavily-leveraged borrowers can grow their way out of debt burdens in a strong economy -- may carry weight.

Never Gentle

There are still risks for bondholders.

The cost of protection on U.S. high-yield bonds rose to the highest since mid-August Thursday, while investment grade also moved up. JPMorgan Chase & Co.’s Global Asset Allocation group recommended a “significant credit underweight” in a note Wednesday, and further acceleration in the bond rout might hurt.

“If people do start getting concerned that growth and inflation are accelerating and rates go up 100 or 200 basis points, then it’s going to be a different story, that’s going to scare people,” said Columbia Threadneedle’s Doubek.

For investors betting against the global credit cycle, shorting leveraged loans via total-return swaps or the ETF market looks cheap since it’s a contrarian trade and an asset class acutely vulnerable in any economic downturn, according to Peter Tchir at Academy Securities.

“Credit goes through long, dull periods, where we grind tighter and tighter, only to explode to higher yields,” Tchir wrote in a note yesterday. “It is never gentle -- it’s just not the nature of the beast.”

--With assistance from Sid Verma.

To contact the reporters on this story: Tom Freke in London at tfreke@bloomberg.net;James Crombie in New York at jcrombie8@bloomberg.net;Natalya Doris in New York at ndoris2@bloomberg.net

To contact the editors responsible for this story: Daniel Hauck at dhauck1@bloomberg.net, Randall Jensen, Brendan Walsh

©2018 Bloomberg L.P.