Companies in Big Refinance Push While Credit Rally Has Legs

Companies Race to Refinance Bonds While Credit Rally Has Legs

(Bloomberg) -- Fearing a repeat of the 2018 selloff in European credit markets, some companies are opting to swallow relatively higher repayment costs now in order to secure longer term savings.

French retailer Fnac Darty SA will pay 18.7 million euros ($20.8 million) to redeem a bond instead of waiting until September, when a scheduled call price would have been cheaper. Elsewhere, investment firm Wendel SA is utilizing a make-whole provision to retire notes maturing in 2020 and 2021 ahead of schedule.

“The companies are saying who knows how the market is going to be in the second half. Let’s do it now at a low funding cost and be on the safe side,” said Thomas Neuhold, a Vienna-based money manager at Gutmann Kapitalanlage AG, which oversees about 9 billion euros of assets. “They are probably doing the right thing. No matter who is coming, the market is willing to buy at any price at the moment.”

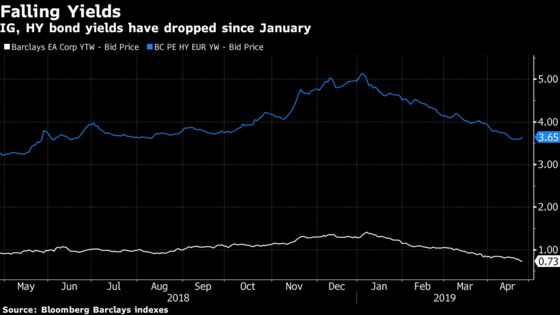

A lack of yield elsewhere and central bankers from Frankfurt to Stockholm turning more dovish this month have continued to boost the appeal of corporate bonds. Euro investment-grade corporate bond yields have tumbled to 0.73 percent, their lowest in 15 months, while those on speculative-grade debt declined to 3.6 percent, near the lowest since June, according to Bloomberg Barclays indexes.

These lows haven’t gone unnoticed. “We decided to do these liability management transactions in the context of a low borrowing cost environment,” Wendel spokeswoman Caroline Decaux said via email. The firm will announce the bonds’ redemption price on May 17.

Confidence Game

Last week Fnac sold two tranches of euro notes to refinance a bond maturing in 2023 rather than waiting for a scheduled call date on Sept. 30 -- under that scenario the company would have paid a redemption price of 101.625 percent, less than the current bid price of 102.522, according to data compiled by Bloomberg.

This decision was based on the retailer’s confidence that current market conditions would allow it to reduce coupons significantly to compensate for the additional premium, according to a person familiar with the transaction. The new euro notes due in five years priced at 1.865 percent while the bond maturing in seven years came at 2.65 percent. The coupon on its existing 2023 is 3.25 percent.

Other high-yield issuers including Rexel SA and Loxam SAS adopted a similar strategy this year, redeeming notes a few months before a step down in call price. Such an approach has seen high-yield borrowers in Europe pay 24 million euros in extra costs so far in 2019, according to estimates by Spread Research, a credit research firm.

The rally in yields has also triggered some unorthodox approaches from financial services borrowers. When Coventry Building Society decided to replace an old contingent convertible bond earlier this month, instead of waiting to do it around the scheduled call date in November, it launched a buyback. The U.K. lender accepted to pay 102.25 percent of face value for the notes that investors sold back.

This year’s additional repayments costs “reflect how careful issuers have been regarding potential spread widening in the second half of the year if the market corrects,” according to Benjamin Sabahi, head of credit research at Spread Research.

“It’s not surprising to see companies acting opportunistically given the market rally this year and how hungry for paper investors are,” he said.

To contact the reporters on this story: Marianna Aragao in London at mduartedeara@bloomberg.net;Tasos Vossos in London at tvossos@bloomberg.net

To contact the editors responsible for this story: Sarah Husband at shusband@bloomberg.net, Charles Daly

©2019 Bloomberg L.P.