America’s Student-Debt Crisis Was Born in the 1600s

America’s Student-Debt Crisis Was Born in the 1600s

(Bloomberg Opinion) -- Presidential candidates have been busy coming up with ways to deal with the student-loan crisis. And it is a crisis: Recent figures show that nearly 45 million people in the U.S. have more than $1.5 trillion in outstanding student loans, with default rates hitting double digits.

How did borrowing become the dominant way to finance a college education? The answer to that question lies deep in the nation’s history. What began as a well-intentioned, private campaign to help needy college students has metastasized into something that now burdens the very people it was meant to help.

The beginnings of higher education in the U.S. date back to 1636, with the founding of Harvard and several other schools in the Ivy League. Initially, these universities followed European precedent by setting up scholarship funds that gave students outright grants. This model became increasingly popular after the American Revolution: The idea that talented students deserved assistance complemented the egalitarian ethos of the early Republic. But then things changed — quickly.

Two historians of education point toward an unexpected culprit: a Boston-based philanthropy known as the American Education Society. Founded in 1815, the AES was designed to help aspiring ministers attend a handful of colleges and universities: Amherst, Yale and Middlebury.

The Quick Rejection of College Grants

Yet within four years, the directors of the AES concluded that the grants fostered “indolence, idleness, and extravagance.” Loans replaced scholarships as a way to inspire motivation, though recipients only had to pay half the principal amount. Unsatisfied with the results, the terms changed again a few years later: Now students had to repay the loan in full — with interest.

Harvard watched these efforts with apprehension: Aspiring ministers were leaving Boston for — God help them! — Middlebury. This would not do. So Harvard started its own student loan fund, tapping wealthy donors to help underwrite the education of “young men of good character and indigent circumstances.” Eager to get a leg up on the AES, Harvard made their loans interest free. But it also capped them at a quarter of the total bill, encouraging students to avoid overextending themselves.

Other schools, elite or not, quickly copied the model. So, too, did institutions eager to subsidize the education of a particular group. The Daughters of the American Revolution made college loans; so, too, did the Jewish Agricultural and Industrial Aid Society and many other philanthropic organizations.

But all these programs remained pretty modest affairs, given that most people attending college hailed from the ranks of the elite. Moreover, there was still some stigma attached to the idea of students going into debt in order to finance higher education.

In 1934, for example, the Atlantic Monthly published a piece entitled “The Kept Student” arguing students would be corrupted by debt. It singled out graduates of Harvard Business School for opprobrium, as well as ministers, a class it darkly described as having “a rather easy attitude toward debt.”

Seizing College Loans for National Defense

World War II changed this calculus, though few people realized it at the time. In 1944, Congress passed legislation that became known as the GI Bill, which made direct grants — not loans — to returning veterans. It also proved a powerful force for encouraging the masses to aspire to college degrees.

But how would non-veterans pay for them? Loans were an obvious solution, and schools offered them directly to students. But there was a “widespread belief that to borrow money for college is to mortgage the borrower’s future,” as Newsweek noted in 1958. In fact, colleges found that when they offered direct loans, they didn’t get many takers.

In their history of student loans, Joel and Eric Best documented how the popular press changed the college-debt narrative one story at a time. The forerunner to Kiplinger’s Personal Finance touted a now familiar cliché: “College education actually provides the increased income that more than pays for itself.”

There were exceptions, of course: The same article warned that ministers — again! — should borrow only as a “last resort,” and it warned women about the risks of accumulating what the magazine delicately described as a “negative dowry.”

While some states began to create their own student-loan programs, the federal government only got involved after the launch of Sputnik in 1957. That epochal event sparked tremendous fear that the U.S. would fall behind its rival without major changes to the educational system.

The result was the National Defense Education Act of 1958, or NDEA. In short, it was designed to funnel enormous amounts of money into the university system. For every nine dollars from the federal government, the schools had to contribute an additional dollar. These funds then became loans to students in fields deemed critical to national defense: science, engineering, and languages.

The NDEA sparked an unprecedented boom in student loans. But something curious happened along the way: Congress amended the NDEA so that students outside these mission-critical fields could get loans, too. Even students attending business colleges, technical schools, and nursing programs could qualify.

Obliterating the Student Debt Stigma

When President Lyndon B. Johnson signed the Higher Education Act in 1965, the transformation was complete. The rationale for student loans was no longer framed as a matter of national defense. Instead, he predicted: “In the next school year alone, 140,000 young men and women will be enrolled in college who, but for the provisions of this bill, would have never gone past high school.”

More striking still was the change in student loans that this legislation inaugurated. Instead of the federal government putting up most of the money loaned to students, it now guaranteed loans made by private lenders. The result was an explosion in lending for higher education.

This helped consummate a profound shift in ideas about debt and college. One lender interviewed by the New York Times in 1968 declared: “Years ago, people resisted the idea of financing their children’s educations with monthly payments, but when the Government got into the educational loan business it took the stigma away.”

The creation of the Student Loan Marketing Association (Sallie Mae) marked yet another step in this process. Founded in 1972, Sallie Mae was modeled along the same lines as Fannie Mae: Both organizations created a secondary market for loans originated by private lenders. Sallie Mae, in other words, would buy up the student loans originated by banks, bundle them, and market them as long-term investments.

The sum of these interventions was very similar to what happened when the federal government got into the business of promoting home ownership: Borrowing soared, and something that had formerly been the province of a small elite became far more democratic.

But borrowing to pay for college has had other, less welcome effects. For starters, prospective students have become far less discriminating when it came to the cost of education. Just as a family contemplating the purchase of a home can easily be persuaded to “stretch” — take on more debt — in order to purchase their dream house, students who are borrowing tend to weigh the prestige of their dream school far more than the cost.

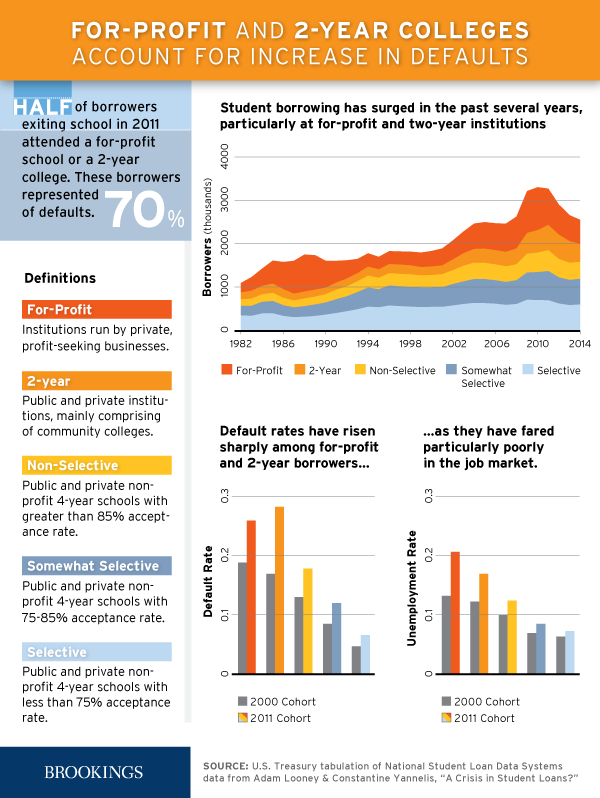

The dramatic expansion of student loans has also led to rising defaults. Some of the students — those with little savings, limited family assistance, and other disadvantages — are effectively “subprime” borrowers, and they’re more likely to default. Moreover, many of these borrowers have enrolled in for-profit institutions that are infamous for leaving students heavily in debt — and jobless.

{kind=link}

There’s no easy answer to these problems. But simplistic solutions — getting rid of tenure, unleashing the free market on higher education — conveniently overlook a deeper problem: The centuries-held belief that higher education should be primarily funded with borrowed money.

To contact the editor responsible for this story: Mike Nizza at mnizza3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Mihm, an associate professor of history at the University of Georgia, is a contributor to Bloomberg Opinion.

©2019 Bloomberg L.P.