CoCos Lose Favor as One of 2019’s Hottest Trades Starts to Cool

CoCos Lose Favor as One of 2019’s Hottest Trades Starts to Cool

(Bloomberg) -- Investors are beginning to get nervous about one of this year’s best performing trades -- risk-laden bank debt.

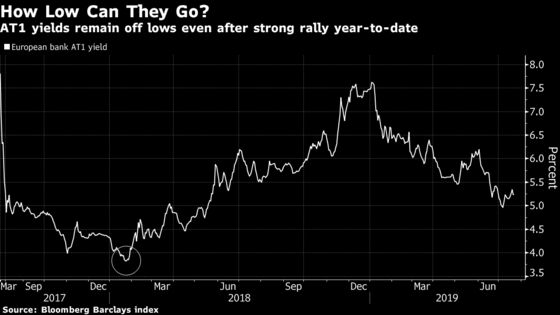

Credit investors have cut holdings of Additional Tier 1 bonds, also known as CoCos, to near multi-year lows, according to a Citigroup Inc. survey, even as they add other notes on the promise of future central-bank easing. The reduction ahead of the summer slowdown comes after mixed-currency European CoCos generated total returns of 13% this year, trouncing other forms of credit, based on Bloomberg Barclays indexes.

“Going into a period of seasonally low liquidity, it makes sense to take some profits,” said Morgan Stanley credit strategist Srikanth Sankaran. “It’s not that valuations are overstretched, but the asset class has come a long way and it has generated significant upside year-to-date.”

Morgan Stanley itself has further reduced AT1 exposure for these reasons, as well as its cautiousness toward Europe’s economy, Sankaran said. Yields on euro-denominated AT1s, the first bank bonds to take losses in a crisis, have also tumbled to 4.3% as investors turn to riskier assets to escape $13 trillion-plus of negative-yielding fixed-income securities.

“AT1 yields shouldn’t be 4%, they should be closer to 6% to reflect the credit risk,” said Stephen Caprio, a credit strategist at UBS Group AG. “We suggest investors lighten up.”

Caprio also cited low liquidity for AT1s, which aren’t in major credit indexes, as well as the risks posed to capital-enhanced banks by weak profitability and non-performing loans.

UBS joined Wall Street lenders in highlighting ongoing pressure on net interest income, even as it reported its best quarterly earnings in a decade. Nordea Bank Abp cited similar concerns last week as it announced a review of financial targets.

Still, AT1s retain an appeal to investors not least because yields are above potential alternatives. Euro high-yield corporate debt pays 3.7%, for example, while euro senior bank bonds yield 0.25%, according to Bloomberg Barclays indexes. Multi-currency AT1 yields are also far above January 2018’s record low of 3.82%, the data show.

Recent new issues have found strong demand including about 2.5 billion euros ($2.8 billion) of bids for a 300 million-euro AT1 sold by Italy-based FinecoBank Banca Fineco SpA earlier this month. Commerzbank AG’s debut AT1, a dollar note, was about 11 times subscribed.

“We continue to have a constructive view on AT1s,” said Sebastian Angerer, senior credit analyst at Western Asset Management, which oversees about $450 billion. “Despite the rally since the start of the year, we continue to find numerous opportunities.”

Still, Western Asset is “highly selective” in the AT1 market, avoiding lenders in high-risk countries or unprofitable banking systems, for example, Angerer said.

More generally, for UBS’s Caprio, the industry’s thin profits, bad loans and lower capital-to-asset ratios are reason enough to be cautious.

“Today’s current subordinated bank spreads and AT1 yields simply trade too tight,” he said in a note with colleagues.

To contact the reporter on this story: Alice Gledhill in London at agledhill@bloomberg.net

To contact the editors responsible for this story: Hannah Benjamin at hbenjamin1@bloomberg.net, Neil Denslow

©2019 Bloomberg L.P.